Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat does a rapid build-up of debt mean for economic growth?

According to the International Monetary Fund (IMF) the total cumulative amount of global liquidity injections, in the form of government spending packages and central bank stimulus measures, adds up to a whopping $14trn.

This represents around 17% of the value of global gross domestic product (GDP), a common measure of the value of all goods and services produced within an economy.

Whichever way you look at the present economic response to the pandemic, the amount of public and private debts are mounting up and could eventually be bigger than at any other time, outside of the two world wars.

The IMF has said it seems likely that the current crisis will be several times more costly than the global financial crisis of 2008 and have far longer effects.

Whether higher debts affect the potential future growth rate of the UK economy, or possibly stir inflationary pressures, are questions being asked by many investors and economists, and here we attempt to lay out some of the issues.

WHAT ACTIONS HAVE BEEN TAKEN SO FAR?

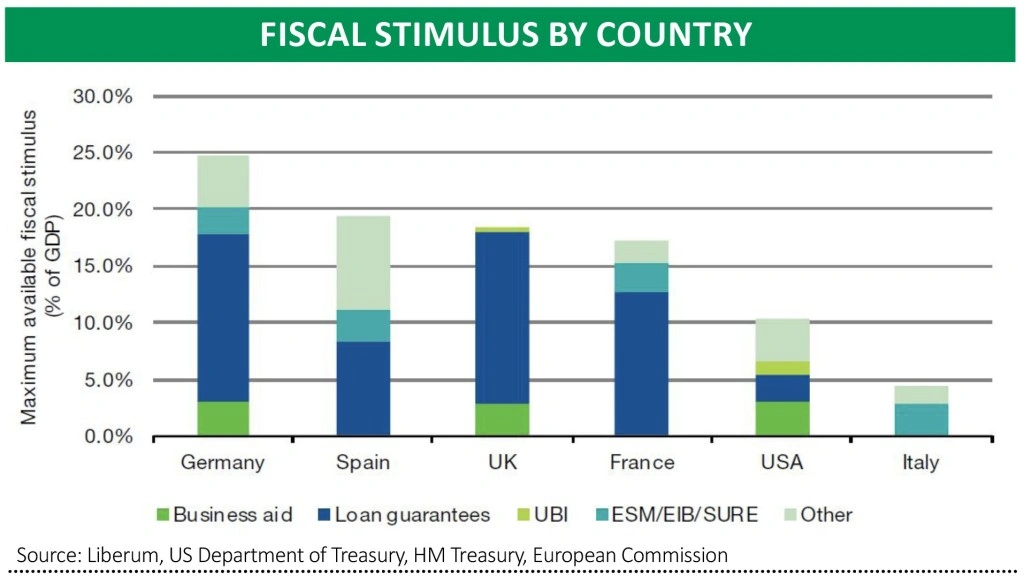

In contrast to the uniformity of action across the major countries, there has been a varied response in terms of the types of support provided.

For example, the US government has preferred to go down the direct bailout route with only $540bn of the total $2trn package containing business loans that will ultimately need to be repaid. The remainder are direct payments that will immediately add to state debts.

This is a different to the route taken during the global financial crisis, when the US launched the Troubled Assets Relief Programme (TARP), which amounted to $700bn or 4.7% of GDP. By the end of 2010 half the money lent had been paid back and five years later 99.7% had been repaid.

The US approach this time contrasts with the UK where £330bn of the £400bn of support is in the form of business loans that need to be repaid. Similarly in Germany €580bn of the €830bn spent so far could be recouped when the economy recovers, when the loans get repaid.

These different routes might have important effects on the national debt of each country in the future. According to projections made by the IMF and OECD, the UK’s debt to GDP ratio by 2030 is expected to be around 88% compared with 84.2% before the pandemic.

This assumes that companies will pay back their emergency loans quickly as happened with the US TARP experience. In the US, debt to GDP is projected to rise to 135% of GDP compared with 125.5% today.

HIGHER DEBTS SLOW ECONOMIC GROWTH POTENTIAL

Data from a study conducted by the Bank for International Settlements (BIS) in 2017 showed a strong link between low interest rates and bank lending practices. As interest rates approached zero, banks lent less and that behaviour remained in place even after the global economy started to grow strongly.

The reason is related to the way banks make money which relies on interest rates in the future being higher than they are today. Banks use short-term customers’ deposits, and lend that money for longer periods to corporates at higher interest rates, earning an interest rate spread.

Central bank action has had the effect of reducing interest rates right across the maturity spectrum, and effectively removed the profit margin for the banks, making them more reluctant to lend.

In the parlance of economists, a major ‘transfer mechanism’ has been broken by the quantitative easing polices pursued by central banks since the global financial crisis.

A 2019 study of 118 international banks showed that as interest rates declined banks shifted their business away from traditional interest bearing activities into fee-based business. In other words, lowering interest rates had the unintended consequence of reduced bank lending, starving the economy of liquidity and lowering growth.

CROWDING-OUT EFFECT

One effect of rising debt levels is well understood due to the pioneering work of two economists, Ken Rogoff and Carmen Reinhart. Their work showed debt-to-GDP levels above 90% reduced growth rates significantly.

A more recent study by Mehmet Caner showed that if combined public and private debt reached a threshold of 137% of GDP, every subsequent 10% increase would reduce real, inflation-adjusted GDP growth by 0.25% over the following five years.

The main reason is the crowding-out effect, which essentially means that private borrowers have to pay higher rates of interest in order to attract investors, increasing borrowing costs and lowering the amount of investment that otherwise would have been made.

The UK and US are already above the threshold rates which will lead to a significant drag on economic growth over the next five years according to investment bank Liberum.

A STOCK FOR A LOW GROWTH ENVIRONMENT

In a low growth and persistently low interest rate world, earnings growth of any kind will probably trade at a premium, while defensive earnings unrelated to the growth in the economy will also be sought.

Around 90% of Go-Ahead’s (GOG) revenues are derived from contracts where there is no direct revenue risk from changes in underlying travel demand. The transport company was recently awarded a new contract to keep running the Southeastern rail franchise which runs to October 2021.

The Government has removed exposure to changes in passenger demand and costs because of the pandemic, making the new Southeastern arrangement a management contract rather than the old one which saw the franchise operator’s revenue primarily generated through passenger fares.

The company has been cutting costs and has suspended the dividend. It has £110m of cash and £134m of unutilised facilities, with net debt of £306m.

The Government has provided £167m of funding to bus operators for at least 12 weeks. When the lockdown ends and business eventually goes back to relative normality, Go-Ahead will be in a good position to reinstate dividends, which have grown around 4% a year over the last five years and provided an average yield of 5%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Exit charge lowered on Lifetime ISA as a temporary measure

- Companies will need to start quantifying Covid-19 impact

- Investors need to be prepared for terrible second quarter results

- Why these stocks have just hit all-time highs

- Orbis seeing ‘most exceptional discounts’ since the credit crunch

- Could we see a return of M&A due to the crisis?

- Berkshire Hathaway builds cash to record levels, sell airline stocks