Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInfrastructure trusts have been a saviour to investors

Amid all the gloom and falling markets as a result of the coronavirus pandemic, at least one area of investment seems to be holding up relatively well.

Mostly seeing smaller declines than the market year-to-date and maintaining their dividends, renewable energy infrastructure investment trusts will have been useful supports in a diversified portfolio.

According to analysis from the Association of Investment Companies, in the six weeks to 13 March share prices of renewable energy infrastructure trusts fell by just 3.2%, compared to a 27% fall in the FTSE 100 and a 13% fall in the S&P 500.

While that may change in the next few months depending on the length and severity of the crisis, most renewable trusts appear to be uncorrelated to stock or bond markets.

SECTOR RESILIENCE

There are several reasons why the sector is resilient, according to Gresham House chief executive Tony Dalwood.

‘Firstly, renewable assets are typically private with relatively stable revenue, and therefore they tend to see less price volatility,’ he explains.

‘Second, and a related point, is that the income yield and the relative security of that is also attractive relative to equities and other financial assets.’

Many renewable energy infrastructure trusts typically get around half of their revenues from government subsidies like renewables obligation certificates (ROCs), which are issued by regulator Ofgem to accredited renewable energy generators. These subsidies are locked in for a period of 20 years.

The other half of their revenue comes from the sale of electricity. This is an area of concern for trusts in the sector generally, given wholesale electricity prices have been low for some time because of an oversupply of cheap gas and lower demand from a mild winter.

REASON TO WORRY?

Electricity prices have since slumped to 10-year lows as social distancing rules resulting from the coronavirus outbreak put the brakes on the economy and dampen demand further. The closure of factories, pubs, restaurants, gyms, shops and cinemas led to a 10% decrease in electricity demand in the last week of March.

However, Winterflood analyst Kieran Drake still thinks the sector is in a ‘relatively strong position’ at the moment, and points out that most funds have at least some fixed price contracts for selling electricity – called power purchase agreements (PPAs) – and so in the short-term have some protection against lower prices.

‘Revenues, and hence dividends, in the short-term look reasonably robust compared with other areas of the market,’ he adds.

For example, Foresight Solar (FSFL) makes around 53% of its revenue from UK Government subsidies, mainly through ROCs, with another 17% fixed through PPAs. Around 30% of its revenues have exposure to the power price.

Its share price has taken a bit of a hit in the year to date, falling around 13%, but manager Ricardo Piñeiro says the fund is ‘well protected’ compared to other sectors and asset classes.

He says: ‘The share price doesn’t necessarily reflect the resilience in the sector. More generally [the market sell-off] is a liquidity point, and renewables haven’t been excluded from that.’

IS THE OIL PRICE SLUMP A CONCERN FOR RENEWABLE ENERGY?

While renewable energy infrastructure trusts haven’t seen their revenue dry up unlike some other companies, exposure to the power price could still potentially dent their income if oil prices remain low for a long time.

Oil has collapsed to multi-decade lows thanks to plummeting demand and a price war between Saudi Arabia and Russia, two of the largest producers in the world, resulting in a huge oversupply in the market and a lack of sufficient takers for all that oil.

Some in the sector insist the oil price has no impact on wholesale electricity prices as it is the price of gas, not oil, which determines wholesale electricity prices, however others say there is an impact as gas pricing is affected by the price of oil.

According to Ofgem, the reason gas is used to determine wholesale electricity prices is because gas-fired power stations are often what’s called the ‘marginal source of generation’.

When electricity demand is low, it is met by cheap sources of power. This has traditionally included coal-fired and nuclear plants, but when demand increases gas-fired generation (which is more expensive) is added to the mix as the marginal source of generation and therefore sets the wholesale power price.

Dalwood explains: ‘The low oil price is affecting power prices in general and it is affecting gas pricing. Some renewables generation is affected and this will continue to be the case if the pricing of oil and the wider energy market remains low for a prolonged period.’

However, Piñeiro says the correlation between the oil and gas price has been decreasing in the past few years with other sources of gas becoming more readily available.

‘There’s a lot more shale gas in the US for example being distributed around the world, and this has helped create a lower level of correlation between gas prices and oil,’ he adds.

DIVERGENT BEHAVIOUR

Despite their resilience not all trusts in the sector have performed the same. Some of the wind and solar trusts, like the aforementioned Foresight Solar, have lagged a little compared to energy storage trusts and those with a mix of wind, solar and other renewable energy assets.

One of the most resilient areas has been energy storage, which has no exposure to the power price.

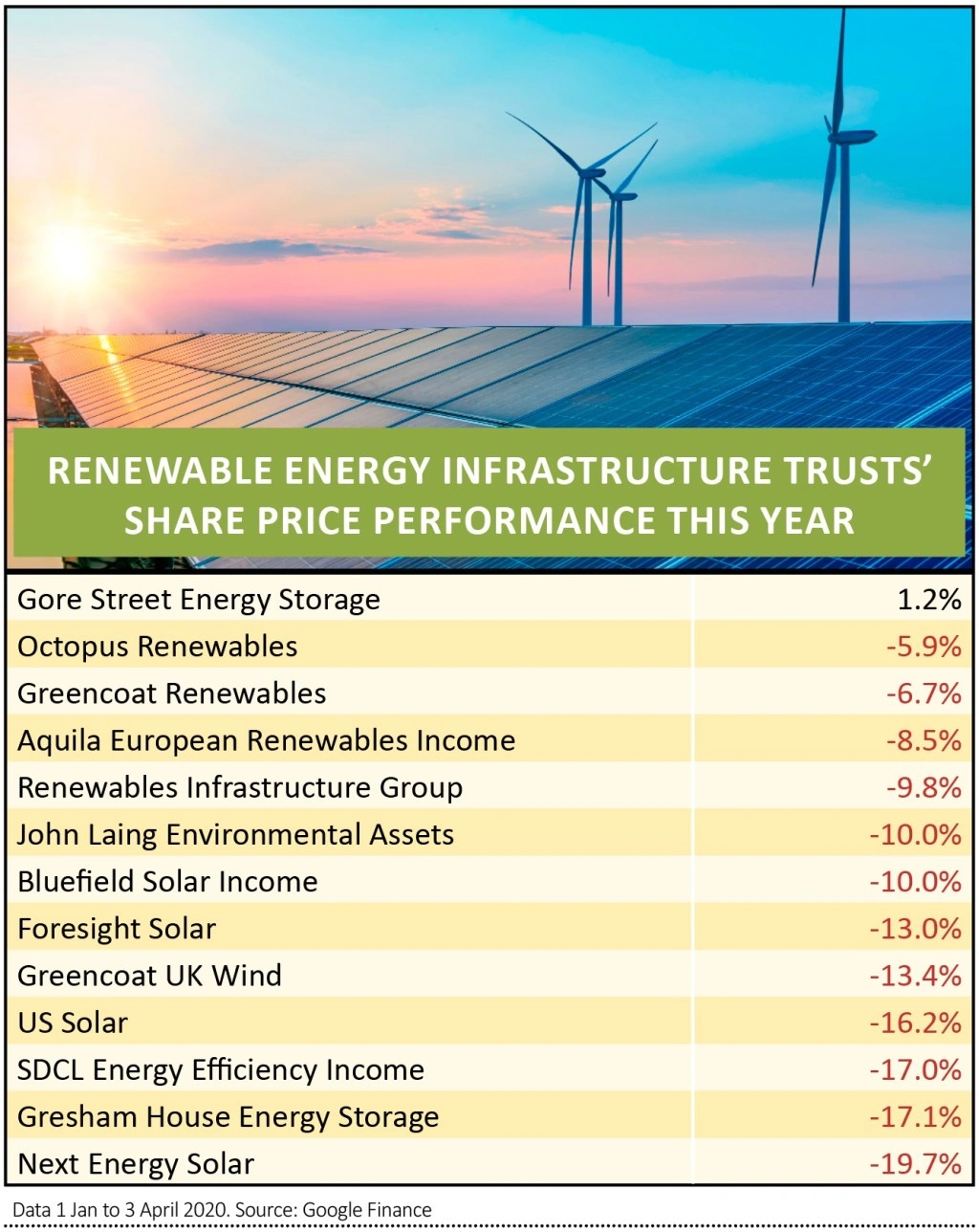

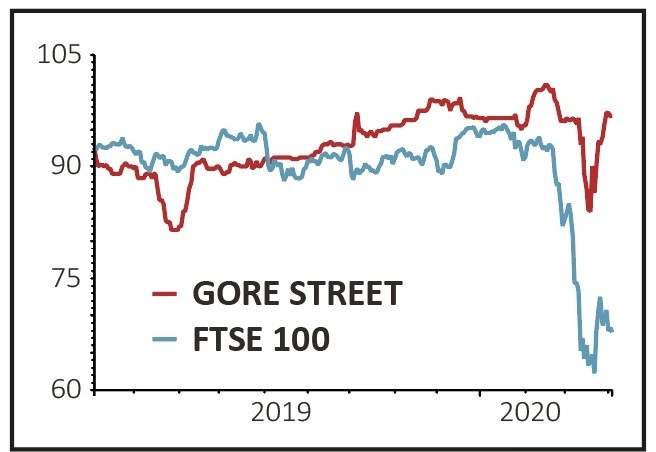

As at 2 April, Gore Street Energy Storage (GSF) has been the best performer, in share price terms, in the AIC’s renewable energy infrastructure sector over the past year, and is currently trading marginally higher year-to-date.

The trust has lithum-ion battery assets in the UK and Ireland, which store energy to be used by the grid when there is an imbalance between the energy being put into the grid and the energy being consumed.

The amount of electricity fed into the grid must always be equal to the amount of electricity consumed, otherwise there’s a black-out.

Alex O’Cinneide, CEO of Gore Street Capital, says that while the trust is not counter-cyclical, ‘we are neutral to events at the moment’.

Its main customers are FTSE 100 utility giant National Grid (NG.) in the UK and state-owned power transmission operator EirGrid in Ireland.

O’Cinneide explains: ‘We provide a service to a very well-capitalised firm. If the grid goes out of balance, they call on our assets to either consume electricity or generate electricity to keep it in check. Energy storage is another form of resilience.’

Not all good news from Infrastructure trusts

Winterflood discusses some important points about three investment trusts:

‘HICL Infrastructure (HICL) looks to be more exposed in the current environment, with 22% of the portfolio invested in demand-based assets where revenues are correlated to GDP.

‘Demand/usage has fallen markedly at the fund’s largest three assets (toll roads and HS1 rail), which together make up 20% of the portfolio.

‘Sequoia Economic Infrastructure Income (SEQI) has seen the largest share price decline of the infrastructure funds so far this year and its rating has moved from a 10% premium to a 10% discount.

‘In an investor call on 16 March the manager highlighted that the economic infrastructure debt in which the fund invests is often supported by physical assets, long-term concessions or licenses to operate infrastructure assets and the companies frequently operate within a regulated framework.

‘However, unlike social infrastructure, economic infrastructure sectors generate revenues from demand, usage or volume.

‘3i Infrastructure (3IN) has also seen a significant de-rating, although it is still currently trading on a premium. The fund invests in the equity of operating economic infrastructure companies and so offers a higher risk potentially higher return than other funds in the sector.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Investment Trusts

Money Matters

News

- Scottish Investment Trust denies ‘style drift’

- £1.6bn fundraising frenzy: companies tap markets to ensure their survival

- UK industrials ‘unlikely’ to breach debt covenants

- Trading platforms see surge in demand amid market volatility

- Market’s attention turns to exit strategy

- UK Treasury reported to be considering strategic companies bailout

- Times are hard for value fund managers

- Lindsell Train’s Japanese fund soars ahead