Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Microsoft could thrive despite coronavirus crisis

There are unlikely to be many stock market winners from the fallout of the coronavirus pandemic, but one of them could well be a company which was right in front of us all along.

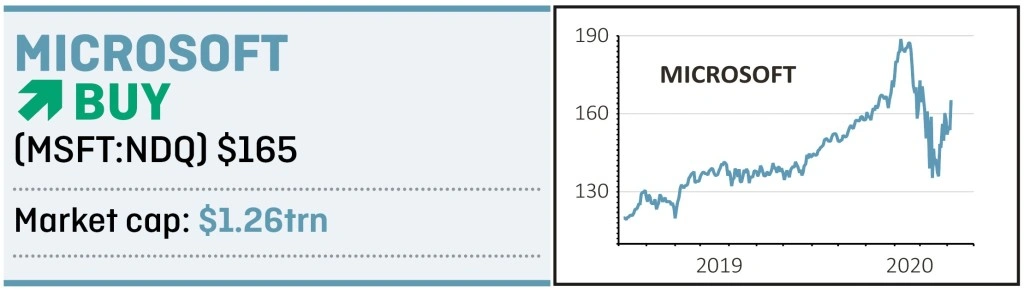

The biggest and possibly most well-known technology company in the world, Microsoft seems as well-placed as any business out there to carry on growing when others are being hit by a global economy in hibernation.

The company’s sources of income can be split into as many as nine categories, with roughly three overarching segments, Productivity and Business Processes (Microsoft Office, Dynamics, LinkedIn), Personal Computing (Windows, Xbox) and Intelligent Cloud (Azure, SQL).

Some of these divisions could be affected by big increases in unemployment, which are already becoming visible particularly in the US, with potentially lower Microsoft Office subscriptions (which have been growing strongly), less PC sales and reduced advertising spend on LinkedIn for example.

But several of the world’s largest companies have increasingly ordered their office staff to work from home, with institutions like the Chartered Management Institute saying it may ‘change the workplace forever’. Significant increases in major companies telling staff to work from home will require equally significant investment in exactly the solutions that Microsoft provides.

FORTRESS-LIKE BALANCE SHEET

This seems to be reflected in the company’s stock price, up 3% year-to-date, and is certainly the view of credit ratings agency Fitch, which gives Microsoft’s short-term credit score at ‘F1+’, the highest rating possible, and long-term score at ‘AA+’, the second highest long-term rating.

Microsoft does have $70bn in debt, but Fitch points out this is easily manageable thanks to its $134bn in readily available cash and annual free cash flow of $25bn.

While going forward the ratings agency highlights cloud computing, its fastest growing and second biggest profit contributor at $16.1bn of its $49.3bn total operating profit in 2019, as the area of most promise for Microsoft.

The coronavirus pandemic looks set to leave forecasts for cloud computing unchanged, as a postponement of key IT projects from some business companies is expected to be offset by other businesses ramping up cloud computing and other IT solutions as they accelerate their ‘digital transformation’.

According to a paper by Verified Market Research, global cloud computing was valued at $258.4bn in 2018 and is projected to reach $930.6bn by 2026, a compound annual growth rate of 17.28%.

The company’s shares are still trading at a price-to-earnings multiple of 26 times, which means its share price will take a hit if the company falls below the market’s expectations.

But the company has a robust balance sheet, resilient near-term cash flows and a long-term growth trajectory that remains more or less unchanged.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Investment Trusts

Money Matters

News

- Scottish Investment Trust denies ‘style drift’

- £1.6bn fundraising frenzy: companies tap markets to ensure their survival

- UK industrials ‘unlikely’ to breach debt covenants

- Trading platforms see surge in demand amid market volatility

- Market’s attention turns to exit strategy

- UK Treasury reported to be considering strategic companies bailout

- Times are hard for value fund managers

- Lindsell Train’s Japanese fund soars ahead