Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat is regular investing and will it help me?

Regular investing can help to smooth out your returns. It is a great way to get into the savings habit and can give you good discipline, but will it generate the highest returns?

Rather than saving up your money and then putting a chunk of it into the market when you’ve reached a certain amount, regular investing involves putting a set amount into your investments each month.

Many investment platforms will allow you to start as little as £25 or £50 a month, which means you don’t have to start with a king’s ransom. You could seek to increase contributions as your disposable income grows.

A big advantage is that you don’t have to remember to invest your cash each month as it is done automatically. Everyone has a ‘life admin’ list as long as their arm, and often it can be easy to plan to invest money but forget to do so.

This means that rather than your money sitting in cash for three months before you remember to invest it, with regular investing automatically buying specific funds or shares you’re getting constant access to investment markets.

IMPOSING DISCIPLINE

On top of regular investing making you more organised, it also means you have a rigid investment process that you stick to. This is important as often emotions can get in the way of investing, and if markets fall investors can panic and decide to sell.

Many investors think they can time the market, and will be able to decide when is exactly the right point to buy into a fund or share. Getting it right is harder that you think.

Even professional investors fail to time markets accurately every time, so your chances of being able to predict when the market will hit its peak or trough are pretty slim. And it could mean you end up buying at the wrong point, or just leaving your money in cash for months while you wait for the right time.

Having the discipline imposed on you to invest regularly is particularly useful for first-time investors, as if you’ve not experienced markets falling before it can be very easy to get spooked and sell, or avoid buying.

SMOOTHER RETURNS

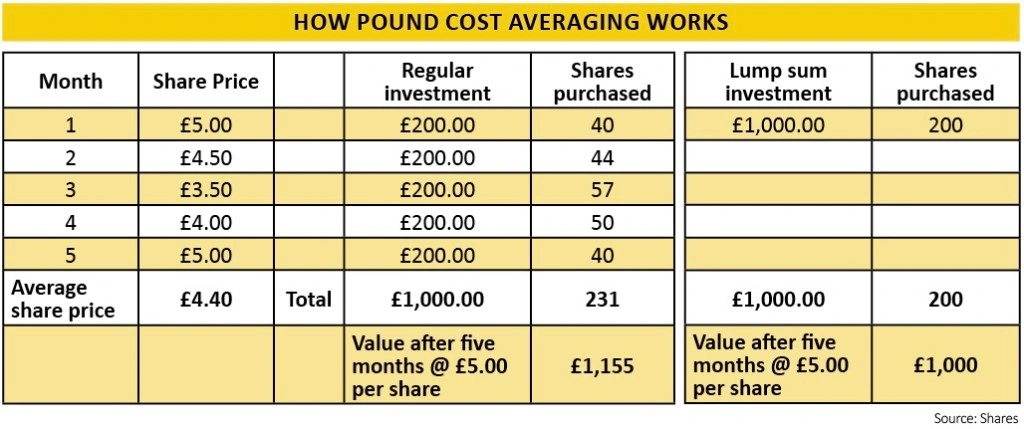

Regular investors benefit from smoother returns, thanks to something called ‘pound cost averaging’. Because you’re putting a regular amount in the market, regardless of market movements, you’ll help to smooth out any volatility.

So-called pound-cost averaging means that when markets rise you are buying fewer shares or units in a fund and when they fall you’re buying more when they are cheaper. The table shows how this could work in a hypothetical example.

So how much could you save from a small amount each month? If you put away £50 a month over 10 years, assuming investment returns of 5% after fees, you’d build up a pot of £6,910, while over 20 years you’d end up with £19,175, showing how a small amount each month can really add up over time.

Let’s look at some real-life examples. If you invested £100 a month over the past 10 years you would have invested a total of £12,000 excluding charges. If you had invested it in the FTSE 100 you’d be sitting on £16,899 today, while if you’d put it in the MSCI World index you’d have £21,675 today.

However, assuming you have all the money available at the start of the year, you’d have been slightly better off investing it in a lump sum at the start of January.

If you’d taken that same £1,200 annual investment and invested at the start of the year, after 10 years you’d have £17,185 if you’d put it in the FTSE 100 and £22,364 if you’d invested in the MSCI World.

This is partly because your money has more time in the market – if you invest at the start of the year that £1,200 is invested in the markets for the entire 12 months, whereas with monthly investing only £100 is invested for the full 12 months, with your final £100 monthly instalment only in the markets for one month before the year end.

However, this depends greatly on how markets perform when you put that lump sum in. If you invested £1,200 and then the market immediately fell, you’d likely have been better off with monthly investing.

WATCH OUT FOR CHARGES

Charges is one area you need to consider. If you’re only investing £25 a month you need to make sure you’re not investing in lots of different funds, as it will cost you a dealing fee each time. However, you will save money in fees with lots of investment platforms if you opt for regular investing.

On AJ Bell YouInvest, for example, you would usually pay £9.95 when you buy or sell shares, but this is reduced to £1.50 if you’re doing so through regular investing. Assuming you buy two shares a month, regular investing could save you £200 a year, compared to making the same two share purchases a month on an ad-hoc basis.

Each platform will have a different day that they carry out the deal. For AJ Bell Youinvest it’s the 10th of the month, or the next working day if that falls on a weekend or bank holiday. However, you can make any changes to the regular investment until midnight the day before the deal.

The other thing you need to watch out for is that you have enough cash in your account to make the regular investment. If you don’t then the deal won’t be done. However, you can set up a direct debit from your bank account to your investment account each month to avoid falling short.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.