Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineKnow your fund: Invesco Income and High Income

Invesco fund manager Mark Barnett has come under increasing pressure following the downgrade of his income funds, Invesco Income (BJ04HW5) and Invesco High Income (BJ04HP8), by fund researcher Morningstar.

The latter has highlighted concerns about the funds’ increased exposure to small and mid-cap companies at the expense of larger, more liquid names. In response Barnett said that his funds are ‘appropriately positioned, well diversified and able to generate liquidity should investors wish to buy or sell’.

Liquidity has become a sensitive issue for investors following the demise of Neil Woodford’s income fund which was full of illiquid holdings, namely investments that couldn’t be sold quickly.

WOOFORD COMPARISON

Barnett has found himself fighting off criticism that he has made similar mistakes to Woodford, a former colleague at Invesco. The Morningstar report has somewhat exacerbated the situation.

We think it is worth looking at the evidence before jumping to conclusions as Barnett’s current situation is not the same as Woodford’s.

Ryan Hughes, head of active portfolios at AJ Bell, comments: ‘People need to be careful in drawing parallels between what happened at Woodford and Mark Barnett’s funds. Yes, Mark was Neil’s protégé to a degree and their investment approaches have some similarities but it is important to note that Woodford had gone down a very different road with his equity income fund by the time it suspended.

‘Investors should therefore be evaluating Mark’s investment approach and the portfolios within his funds in their own right.’

BARNETT’S INVESTMENT POLICY

Both the Invesco Income and High Income funds aim to deliver a mixture of income and growth via investing in UK equities. Barnett looks for undervalued businesses where the share price can appreciate and the income stream can grow.

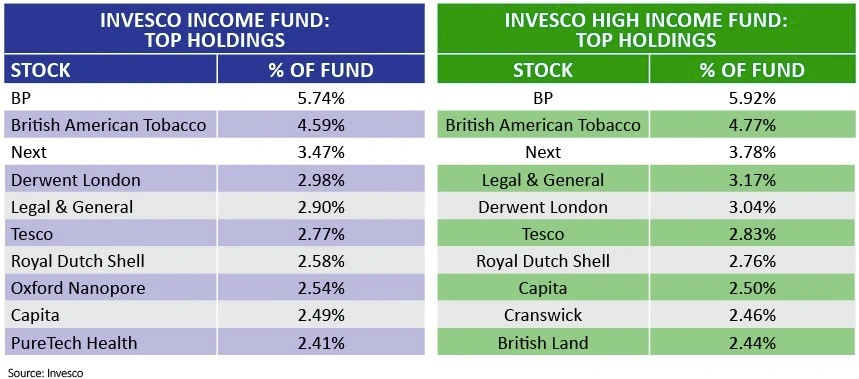

The inclusion of growth in the investment style explains why his portfolios include non-dividend paying companies such as outsourcer Capita (CPI) and healthcare provider PureTech Health (PRTU).

Both funds invest at least 80% of their assets in shares domiciled or carrying out their main activities in the UK. The funds can invest in unquoted and private companies and can use derivatives to manage risk.

The benchmark used to compare performance is the Investment Association UK All Companies sector. The manager is not constrained by any benchmark and is free to construct portfolios that differ widely from the FTSE All-Share index.

THE INVESTMENT PROCESS

Barnett employs a long-term fundamental approach that combines a high-level macroeconomic view which informs active stock picking across the entire market cap spectrum.

The funds’ starting point is to highlight areas of the market which are unloved or where a macro headwind has been mispriced. Barnett will look to get exposure to these areas of the market by populating the portfolios with individual stocks.

Barnett and his team use a variety of traditional metrics such as price-to-earnings ratios and price-to-book value to screen for mispriced stocks. He conducts fundamental research using his own stock knowledge as well as input from Invesco’s broad UK equities team.

He builds the portfolios without regard to the benchmark, basing his decisions on fundamental conviction levels while considering the downside risk and liquidity. He adopts a 6% limit on individual stocks, but has no constraints on sector weights.

For example at the end of September 2019 the High Income fund had a 42% weighting in financials compared with 21% for the benchmark.

Historically he has had a clear focus on strong and sustainable cash flows because they were considered a good indication of a company’s ability to grow dividends.

FUND POSITIONING

Barnett believes that the most compelling opportunities in the current climate lie outside the ‘the dominant top tier’ of the FTSE All-Share Index, in cash generative companies – ‘many of which are UK-orientated which been overlooked by the market, in a climate of political uncertainty’.

It should be remembered that the investment policy states that in a changing global environment investors’ interests are ‘best served by employing a well-tested investment process, which is based on fundamental company analysis and a prudent approach to valuation’.

The issue isn’t that Barnett has strayed from his tried and tested investment process, but that the process has logically resulted in shifting the funds’ focus towards smaller, domestically-focused stocks, at the expense of large liquid internationally-exposed companies.

One criticism levelled at Barnett by Morningstar is that ‘an increasing number of stock-specific issues, notably among smaller, less proven businesses, have raised concern over the depth of fundamental analysis and focus on risk.’

Morningstar points out that while Barnett has support from seven other fund managers and analysts they have their own strategies to manage which leaves Barnett with a ‘considerable workload’.

Barnett himself commented recently that ‘over the last few years, the performance of the funds has been disappointing in capital appreciation terms and I regret some of the stock- specific challenges’.

One example is specialist card retailer Card Factory (CARD) which has issued a number of profit warnings over the past two years. However in a recent trading statement the company reported positive like-for-like sales growth. That said the stock is trading at half the peak levels achieved in 2015.

THE LIQUIDITY FACTOR

In response to Morningstar’s concerns on liquidity, Barnett points out that more than two-thirds of the funds are invested in companies worth more than £1bn. In addition he has reduced exposure to unquoted investments from £944m to £493m since taking over management of the funds in 2014 and less than 1% is invested in companies worth less than £100m.

Although Barnett believes that the funds can generate enough liquidity to meet redemptions, it is clear that running a large portfolio with exposure to small and mid-cap companies is more challenging from a portfolio construction perspective than investing in large caps. The risk is that the funds, being so large in size themselves, will end up owning bigger chunks of smaller firms.

PERFORMANCE HAS LAGGED

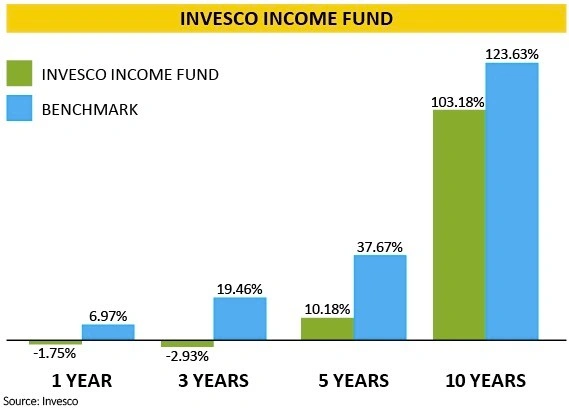

The Invesco Income fund has delivered 1.96% annualised returns over the past five years compared 6.6% for its benchmark, according to the asset manager’s latest factsheet.

While this is disappointing for holders, past performance isn’t always a good guide to future performance. The contrarian nature of Barnett’s approach means that ‘suffering’ poor short-term performance is the price paid for delivering superior longer-term performance.

Barnett has endured an unusually long period of underperformance, but one thing in the funds’ favour is that market trends are prone to reversing without warning.

As the manager has highlighted, global equity markets have reached such an extreme level that £1 of revenue sourced in the UK is now worth less than a third of $1 of revenue sourced in the US.

In other words pessimism towards the UK has driven a fundamental mispricing which will benefit the fund if and when that condition normalises.

We’ve recently written about how there are signs value investing is coming back into favour. If that trend continues then Barnett could be in a strong position to benefit.

DISCLAIMER: Invesco is a shareholder in AJ Bell, owner of Shares. The author and editor Daniel Coatsworth own shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.