Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvestors pile into gold just before price slumps

Reports that the US and China are making progress to resolve their trade dispute has been welcomed by many investors. But for those who invest in gold, and the mining companies that dig the precious metal out of the ground, the news has been less well-received.

Gold is considered a safe haven asset – it does well in times of market stress, such as when investors are worried about the global economy. It goes out of favour when investors regain confidence.

Like other safe haven assets, such as Swiss, German and Japanese government bonds and shares in non-cyclical companies, it appears that gold’s momentum may have hit a wall.

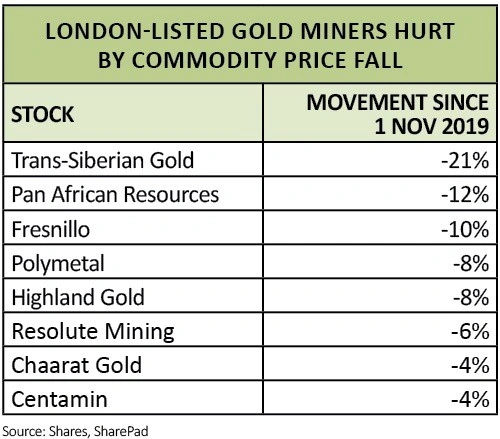

Gold has fallen from $1,511 per ounce on 1 November to $1,452 on 11 November, a drop of nearly 4%.

It comes after major stock markets worldwide – like the S&P 500 in the US and the CAC 40 in France – hit all-time or multi-decade highs as China’s Commerce Ministry said on 7 November that a deal would include tariff rollbacks. However, US president Donald Trump subsequently said this hadn’t been agreed.

The drop in the gold price wasn’t good news for gold exchange-traded fund (ETF) investors, particularly those who had recently put money into the asset class. The World Gold Council says the third of quarter of 2019 saw the largest inflow into gold-backed ETFs since the first quarter of 2016.

According to strategists at US research firm Bespoke Investment, the pullback in the gold price is not surprising as the market begins to move away from ‘recessionary pricing’, as pockets of optimism over the global economy lead the price of shares to go up and the price of gold and government bonds to go down.

If big macroeconomic issues heighten in the coming months, such as relations deteriorating once again between the US and China, Brexit not going well and German manufacturing output getting worse, then gold could be back in favour.

Not everyone thinks the gold rally is over. Hardman & Co equity analyst Paul Mylchreest points to the inverted yield curve seen in US government bonds earlier this year as a positive for gold.

This is because every time there has been an inverted yield curve, except in 1995, a recession has followed within two years and that could shift investors back towards gold.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.