Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePat on the head for Pets at Home

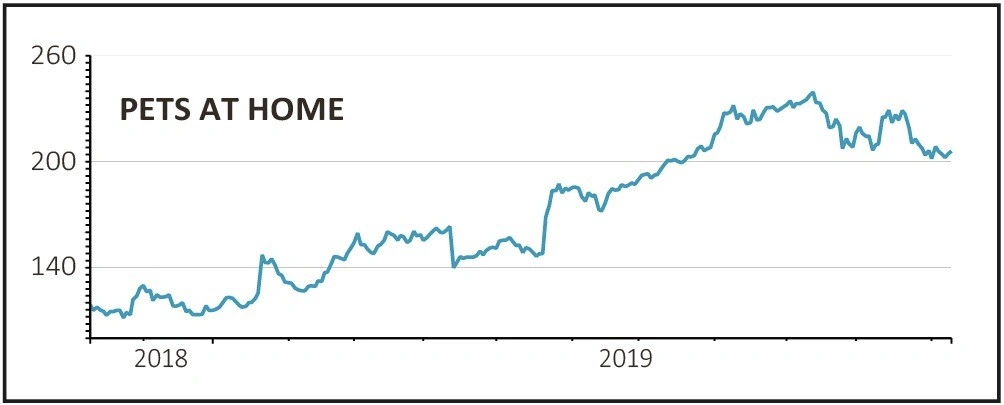

PETS AT HOME (PETS) 205.4p

Loss to date: 3.6%

Original entry point: Buy at 213p, 5 September 2019

While our recent call on specialist retailer Pets at Home (PETS) has still to produce a positive return, we note that Liberum Capital has issued a ‘buy’ recommendation on the UK’s leading pet care business for the first time in three years, validating our investment thesis.

The broker says Pets at Home’s decisive actions, including own-brand price cuts, are delivering results, giving it greater confidence that the retailer’s pre-tax profit will start to grow again soon.

Liberum also thinks first-half results on 26 November should reassure that momentum is continuing. It believes retail like-for-like growth of 6%-to-7% is ‘probable’ and sees share price upside as the market gains more confidence in Pets at Home’s earnings and free cash flow improvement potential.

The broker says this is ‘shaping up to be one of the most impressive turnarounds in the sector of recent times’.

SHARES SAYS: Pet retailing is a resilient niche and we’re sticking with the turnaround underway at Pets at Home. Keep buying at 205.4p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.