Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFour stocks priced for perfection and likely to disappoint investors

Controversial Brexiteer hedge fund manager Crispin Odey is fond of saying that cycles never die, or what goes up inevitably comes back down. What this means is that investors can sometimes mistake structural growth for cyclical growth.

This can be applied to a company’s valuation too, which expands and contracts in ‘cycles’ depending how a company’s earnings are progressing compared to expectations.

When the up-cycle inevitably rolls over a stock’s price-to-earnings (PE) ratio can fall dramatically, taking the share price down.

We’ve used data from Stockopedia to screen for stocks which are priced for perfection. We identified the most expensive stocks in the market and where analysts have downgrades their earnings expectations more aggressively than the market.

WHAT DRIVES THE UPGRADE/DOWNGRADE CYCLE?

One of the factors that drive the PE higher is related to a behavioural trait whereby analysts are slow to publish an upgrade to earnings, but fast to downgrade on the first signs of trouble. In other words, good news travels slowly, while bad news travels fast.

The former effect creates a self-fulfilling upgrade cycle as analysts play catch-up with the fundamentals. It also means that upgrades tend to lead to more upgrades in the future.

HIGHER REVISION STOCKS TEND TO OUTPERFORM THE MARKET

Academic evidence from Philip McKnight and Steve Todd has shown that stocks with the best upward revisions tend to outperform, so investors chase those stocks higher. But even greater future upward revisions are needed to give investors comfort.

At some point analysts get ahead of the curve and realise they need to start downgrading their expectations. If this happens when a stock is trading at an elevated PE, trouble lies ahead.

We have chosen four stocks from our screen. Each of them have the potential to disappoint and miss future profit expectations and are therefore at risk of seeing their PE de-rated.

AstraZeneca

Pharmaceutical giant AstraZeneca (AZN) has seen its fortunes turn around over the last three years and can now boast one of the strongest cancer drug pipelines in the industry.

The impressive turnaround has seen the company’s PE increase from around 13 times in 2014 to the current rating of 22.5-times. This represents a 56% premium to the PE of rival GlaxoSmithKline (GSK) which is also in the process of revamping its drug pipeline. Over the past five years shares in AstraZeneca have risen by 60% compared with 22% for GlaxoSmithKline.

However over the past few months earnings expectations for GlaxoSmithKline have risen by around 8% while analysts have actually downgraded AstraZeneca’s earnings estimates. Despite the 20% expected growth rate in earnings next year, investors in AstraZeneca need to see continued upgrades to justify such an elevated PE ratio.

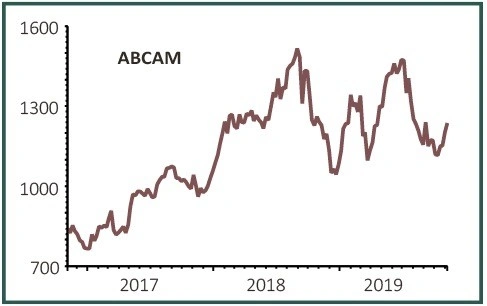

Abcam

Life sciences group Abcam (ABC) has seen its shares go up over 10 times in the past decade, driven by strong growth in earnings.

But in the past couple of years the growth profile has started to falter, leading the company to make significant investment in the business to ‘kick-start’ growth.

In September the company announced a long-term plan to achieve revenue of £450m to £500m by 2024, putting the company back onto a 12% to 13% revenue growth path at a cost of £175m to £225m of investment.

The PE has risen from 25 five years ago to the current rating of 39 times earnings per share. Meanwhile analysts have reduced their earnings expectations by 16% since January, a worrying sign for a business that is priced in the most expensive 5% of the market.

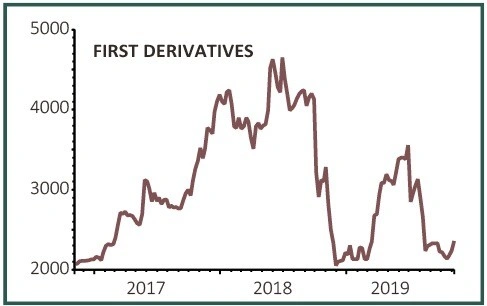

First Derivatives

Computer and software services firm First Derivatives (FDP:AIM) has been a notable growth story over the past five years, increasing sales from £70m in the 12 months to February 2014 to £217m five years later.

According to the analyst consensus forecast, this growth should continue with sales seen reaching almost £300m in February 2022. Meanwhile the cost of sales is seen holding steady so the firm’s gross profit margin is seen climbing from around 27% to nearer 45% in the next few years.

Investors have chased the stock up to a PE of 44 based on current year earnings estimates. That’s essentially pricing in a lot of the expected future gains today. So if the firm doesn’t deliver, that rating could fall very quickly.

ASOS

Online fast fashion retailer ASOS (ASC:AIM) has delivered a number of profit warnings over the past 10 months which has seen its shares fall by two thirds from the highs of £76 in the spring of last year.

In October the company delivered a 68% slump in full year pre-tax profit despite sales rising 15% to £2.7bn. While most retailers would envy reporting such sales growth, it pales compared to the 20%-plus that the business has historically achieved.

Trading on a PE of 52 and with analysts still downgrading their earnings expectations, which have fallen 30% since January, the company has a lot to prove to justify its rating.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.