Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFTSE 100 needs more momentum to make further gains

We are six months into the year and the FTSE 100 is up nearly 9%, with the prospect of a decent dividend on top. Given everything that is going on in the world right now, it seems fair to assume that many investors would have taken that return for 2019 as a whole, had they been offered it on 31 December last year.

The index’s advance is at least partly the result of its valuation, since a forward price-to-earnings ratio of 13.1-times and a dividend yield of 4.7% look attractive, in absolute terms and also relative both to the benchmark’s history and to other geographic options available to investors.

Bulls of UK stocks may therefore be drawing comfort from how aggregate profit forecasts for the FTSE 100 are holding up, despite the prevailing uncertainty over issues such as global trade and tariffs, central bank monetary policy and the growth trajectory of the Chinese and US economies, let alone Brexit.

Equally, bears can point to a lack of upgrades in earnings (at least of any magnitude) and downgrades to dividends to back up their cautious outlook.

Profit progress

The good news is that analysts are, in aggregate, expecting the FTSE 100 to generate an all-time high pre-tax profit of £225.5bn in 2019. That is a meaty 16% increase on 2018 and finally takes the index past the £202bn peak of 2011, when over £100bn in pre-tax profit came from the then-buoyant mining and oil sectors.

In 2019, oils and miners are forecast to churn out £74bn in profit, so the base of the FTSE 100’s earnings power seems more broadly based than it was eight years ago.

On balance, this should be a good thing, especially as the aggregate profit contribution from oils and miners is expected to drop by some £1.6bn in 2019 thanks to soggy commodity prices.

Financials and industrial stocks are seen by analysts as taking up this slack. The rebound in industrials stems mainly from Rolls-Royce (RR.) and Melrose (MRO), as the former sorts out its engine problems and cost base and the latter gets to work on 2018’s acquisition of GKN.

Whether investors feel comfortable relying on the banks is another matter. While the banks are already heavily provisioned for a final surge in claims, the PPI deadline probably cannot come quick enough for them.

Meanwhile, challenger and digital rivals continue to nip at their heels and central banks’ U-turn in interest rate policy, with the next movement now likely to be down rather than up, will only hurt net interest margins at a time when they are already thin.

Lack of momentum

The unhelpful contribution from miners and oils may not be a surprise given the lack of clarity on the global economic backdrop but the index is relying on banks and industrials – which are also cyclical and sensitive to the economy to varying degrees – for this year’s earnings growth.

That may be a concern for some and bears may continue to growl unless we see some genuine upgrades to profit (and dividend) forecasts for 2019 and 2020, so that some positive momentum can carry the FTSE 100 to, and then beyond, May 2018’s all-time high of 7,877.

The news here is mixed. We are not seeing any downgrades but we are not seeing upgrades of any note when it comes to earnings.

In aggregate, analysts’ earnings forecasts for the FTSE 100’s members have dropped by 7% so far this year, to £226bn from £242bn at the end of last year. The only good news is that the rot stopped in the second quarter, when earnings forecasts ticked up from £224bn in March.

The absence of profit upgrades or downgrades suggests that neither FTSE 100 boards nor analysts know much more than investors, as analysts will tend to use guidance from management teams as the basis for their forecasts.

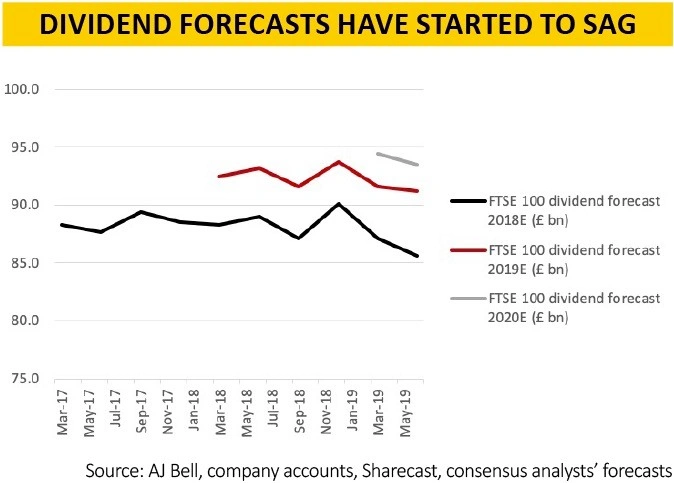

Aggregate dividend payments are expected to grow by 7% (excluding special dividends) but momentum is negative. Thanks to cuts from Vodafone (VOD) and Marks & Spencer (MKS) dividend payment forecasts have fallen for the second quarter in a row and, at £91.2bn in total, now stand 3% below where they began in 2019.

The battle lines therefore remain drawn. Bulls like UK equities because they have underperformed their global peers for more than three years, look cheap on both an earnings and a yield basis as a result, and it will just need a bit of positive forecast earnings momentum to stoke fresh interest.

Bears will counter that the FTSE 100 is cheap because it deserves to be, given concerns over the quality of profits, the quantity of dividends and how any downgrades in the event of a global slowdown could leave the index bereft of a positive catalyst.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.