Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTypically impressive GB Group balancing underlying and acquisitions growth

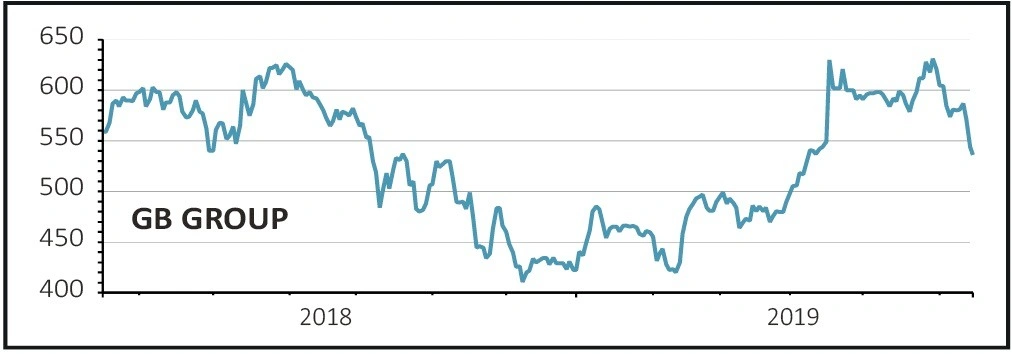

GB GROUP (GBG:AIM) 540p

Gain to date: 27.8%

Original entry point: Buy at 422.5p, 20 December 2018

A pause for breath was to be expected after such a strong start to the year for identity data intelligence expert GB Group (GBG:AIM). That the stock, one of our top picks for 2019, remains up by more than a quarter year-to-date even after two months of relative drift illustrates the point.

GB believes it holds a technology edge over competitors and we agree. Knock-out full year results on 5 June suggests that customers both new and old increasingly share that view. Revenue up 20% to £144m encompasses very decent 12% organic growth while expanding margins at 22.3% fired a 21.7% jump in operating profit to £32m.

Some working capital wobbles saw operating cash flow decline 12% to £27.8m and cash conversion dip to 81%, but we believe this to be a short-term effect that will iron itself out down the line.

Otherwise it is business as usual with international expansion and cross/up-selling very much the focus, supported by integration of Vix Verify and IDology, opening new and ‘significant’ opportunities in Australasia and the US respectively.

Updated market expectations call for £195m of revenue and £46m of earnings before interest, tax depreciation and amortisation, implying rough 35% growth on both measures.

SHARES SAYS: Typically impressive, GB remains a stand-out UK technology growth story.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.