Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to tell if oil’s rally can continue

Almost unnoticed, oil is trading near four-month highs at $67 a barrel for Europe’s Brent Crude benchmark and $59 for America’s West Texas Intermediate. According to OPEC’s latest monthly report, demand is holding firm at between 97m and 98m barrels of oil a day.

This suggests that any tightness in the market is the result of supply, a view which seems logical enough in view of (limited) American sanctions on Iran, a sharp drop in output in Venezuela (thanks to economic and political chaos) and apparent Saudi determination to stick to the production cuts outlined by Riyadh at last December’s

Vienna OPEC summit.

Besides these geopolitical and economic issues, four further, more tangible and easily measured, factors are at work: global oil rig

activity, inventories, US shale output and positioning in the financial markets.

Thankfully, they are all a little easier to judge and measure than the affairs of state in Caracas or the workings of US President Donald Trump’s foreign policy.

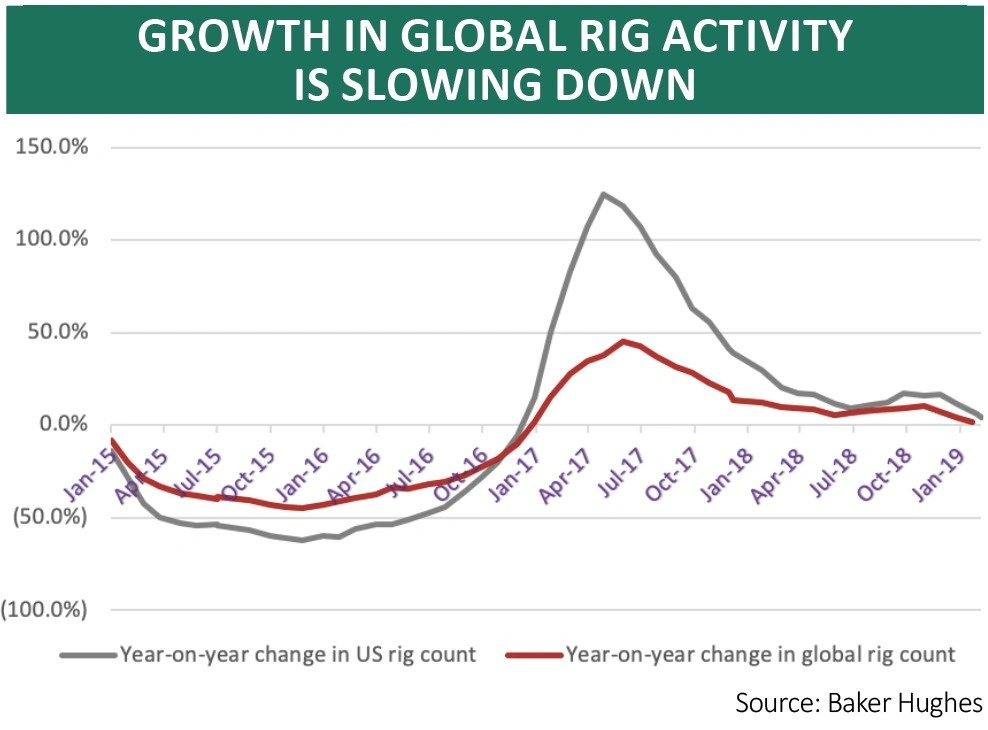

RIG WORKS ROLLS OVER

A slowdown in growth in American and global oil rig activity would point to a better balance between supply and demand and one suited to the plan formulated by Saudi Arabia and Russia late last year to support the price of crude. Growth in active US rigs looks to be slowing while the global rig count is now up by just 2% year-on-year.

American oil inventories may have also stopped growing, at least if a recent unexpected drop is any guide, with stockpiles are now just 4% higher than they were a year ago.

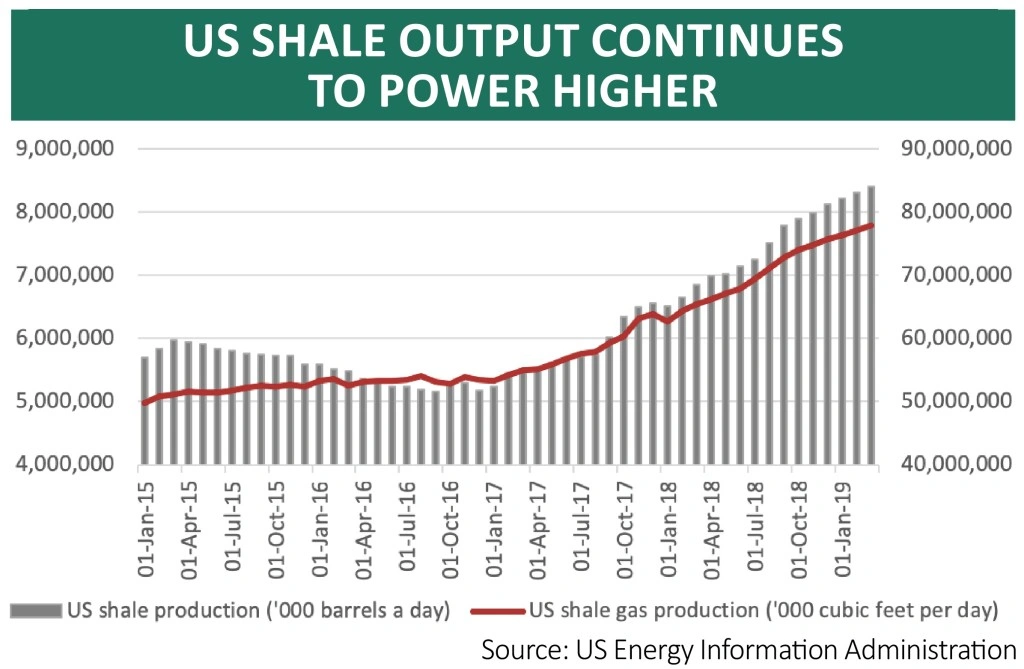

SHALE SURPRISE

This could be seen as reasonably bullish for oil but seasoned commodity watchers will know it is never that simple.

American shale output remains a major wildcard. Rig activity may not be rising but output per rig is and shale production in the US continues to advance as a result. It now stands at 8.4m barrels of oil a day, up by 1.6m barrels a day when compared to March 2018, a surge that offsets much if not all of the loss of Iranian, Venezuelan, Saudi and Russian production.

There is no sign of shale output slackening any time soon and this is a potential cap on the price of crude, at least on the other side of the pond.

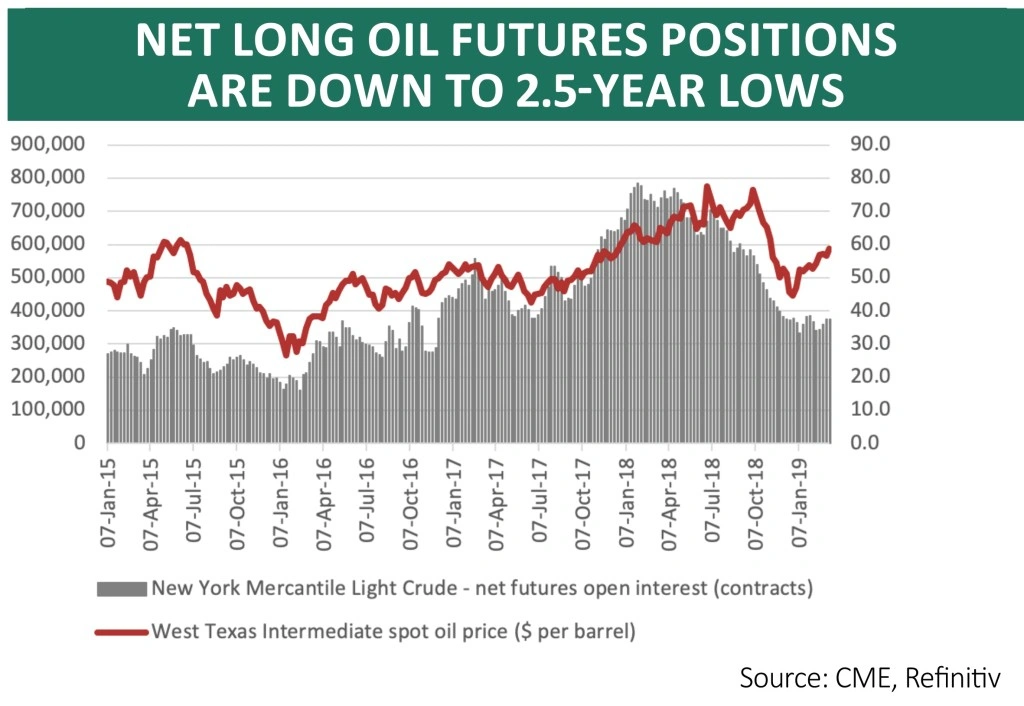

Intriguingly the fourth and final factor is the one whose influence is most frequently underestimated – how financial speculators are positioned via the futures market, where each contract is worth 1,000 barrels of oil.

According to data from the CME the number of long futures contracts in early July 2018, where traders were betting on oil price increases, was 771,350 against just 68,994 that were short and betting on oil price declines.

That made for a net long exposure of 702,356 contracts – so, surprise, surprise, oil promptly plunged from nearly $80 to barely $40. When it looks like everyone is already bullish it can be hard for an asset to do well, at least in the near term.

The picture is now a lot less clear cut. Long positions have been cut to 473,621 contracts but shorts are still rare at just 99,757 for a net bullish position of 373,864.

On balance that is still toward the top of the historic range for net ‘longs’ but the message seems to be that even the professionals who constantly look at oil do not necessarily have a strong view right now.

PUMP UP THE DIVIDENDS

Taking a punt on oil via a handful of oil producers or explorers through an industry-related exchange traded fund (ETF) or a tracker fund that follows the stock market of an oil-related region or country, such as the Middle East, Saudi Arabia or Russia, therefore looks risky.

But perhaps investors in UK equities can draw some degree of comfort from oil’s latest ascent. After all, BP (BP.) and Royal Dutch Shell (RDSB) between them represent 15%, 18% and 19% of the FTSE’s market cap, forecast profits and forecast dividends respectively for 2019.

And the more firmly the oil price is underpinned, the better their dividend cover and by implication the 4.7% dividend yield currently on offer from the FTSE 100, according to analysts’ consensus forecasts.

So whatever you think of Brexit, at least investors are being paid to sit patiently as they wait for the negotiations to conclude, helped by oil’s latest rally.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.