Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUse investment trusts to cash in on historic low valuations and high yields

For decades UK stocks were prized by global asset managers but in the last two to three years they have been roundly shunned due to uncertainty over Brexit.

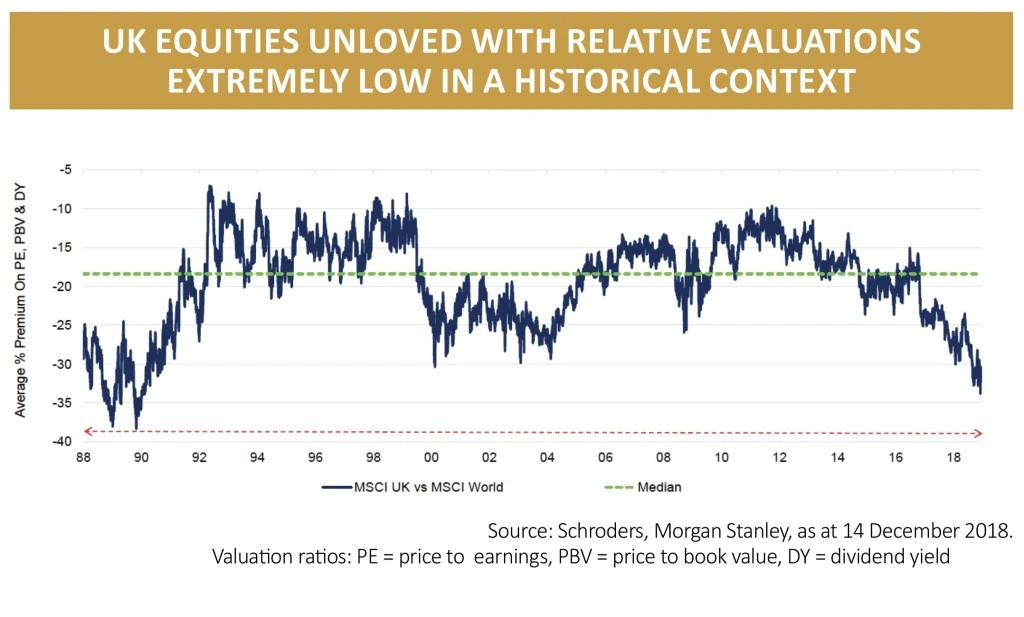

The result is that on some measures the UK stock market is now the cheapest it has been for nearly 30 years.

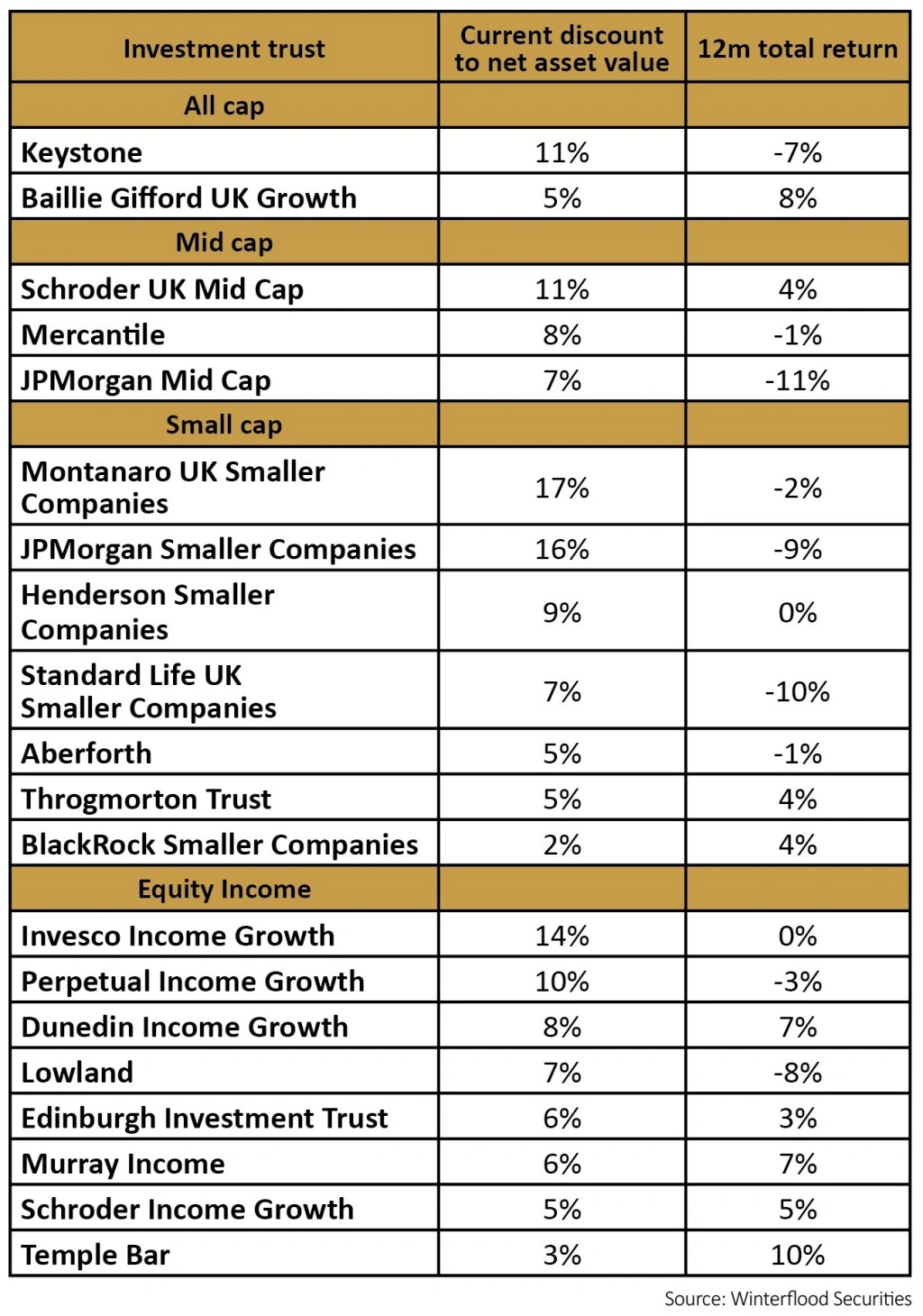

With valuations so low, investment trusts are a great way to get broad exposure to the UK market and some well-known trusts are also trading at a discount to net asset value (NAV) meaning that canny buyers can get a double discount.

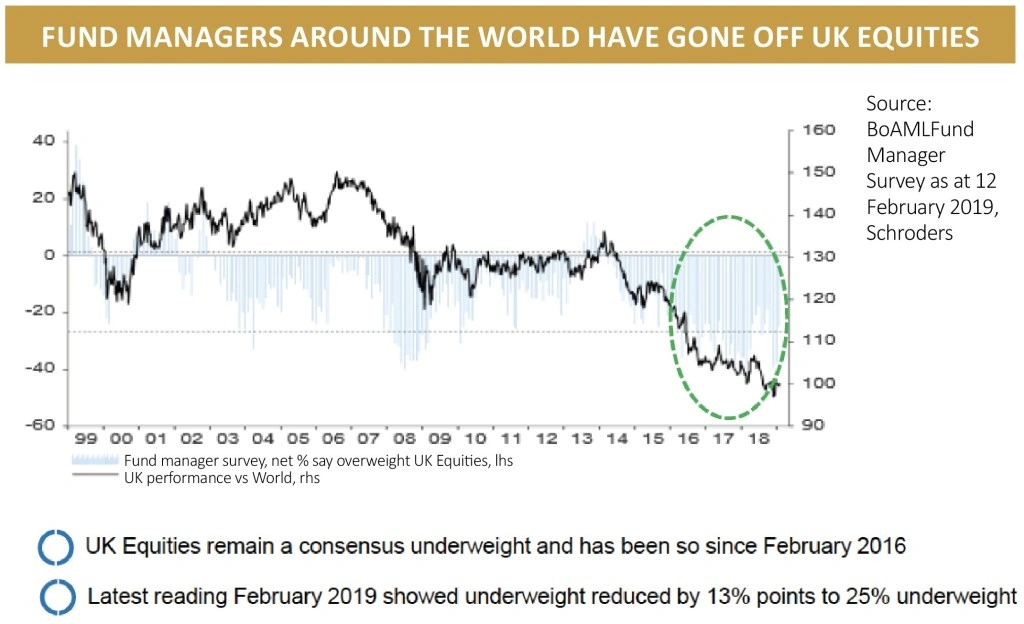

BEST OF BRITISH

Historically many global investors had a large weighting to UK stocks in their portfolios based on the quality of their earnings, their professional management teams, the business-friendly regulatory regime, high levels of corporate governance and reliable dividend streams.

Also buying a basket of FTSE 100 stocks meant diversification as more than 70% of the index’s sales and earnings are generated overseas meaning investors can tap into global growth, often at a discount.

However the last two to three years have seen international investors desert the market in their droves and the overall asset allocation to UK equities has tumbled to decade lows according to research by Bank of America Merrill Lynch.

As the right-hand side of the first chart shows, fund managers are as underweight UK stocks today as they were at the height of the global financial crisis, if not more so (blue bars).

At the same time the UK stock market has underperformed global equity markets sharply over the last two to three years.

Looked at another way, UK stocks are at their lowest valuation in almost 30 years on a combination of price-to-earnings, price-to-book and dividend yield.

Over 30 years the average discount between global markets and the UK has been in the region of 18% although that figure is somewhat skewed by the last five years: excluding the most recent past the average discount would likely be between 15% and 18%.

Today the discount is almost 35%, roughly double the average, taking it back to the levels of the early 1990s. Yet one could argue that UK companies today are in far better shape than they were in the early 1990s so buyers now are getting better management and a higher-quality earnings stream.

Investors looking for income are really being spoilt at the moment with UK dividend yields at a level which has only been seen twice before in the last three decades – during the tech bubble and before that in the 1991 recession.

A RICH HUNTING GROUND FOR INCOME

Schroder Income Growth (SCF) fund manager Sue Noffke says for dividend payouts would have to be cut by a quarter for yields to ‘normalise’ from the current 4.7% to the 30-year average of 3.5%.

Even during the global crisis, the peak-to-trough fall in dividend yields was only 15% so a 25% fall looks unrealistic.

Alex Wright, manager of Fidelity Special Values (FSV), says he is ‘struck by the sheer number of stocks across different sectors whose valuations suggest significant asymmetry of risk and reward over the next two to three years’.

Among the sectors where he is finding opportunities is financials. ‘The assets held by UK life insurers are significantly higher quality and more internationally diversified than the market is discounting,’ he adds.

Alastair Mundy, manager of Temple Bar Investment Trust (TMPL), is also finding opportunities in UK financials.

He says: ‘The UK banks have become something of a pariah sector but we have seen significant changes and improvements over the past decade and yet they remain on undemanding valuations.’

New management, strengthened balance sheets, closer regulation and the winding down of provisions for past misconduct mean

banks are much more profitable than they were.

Mundy is also finding opportunities among retailers and housebuilders and he expects the builders’ merchants to be big beneficiaries once housing transactions pick up again.

Schroders’ Noffke agrees that ‘some of the most attractive opportunities are among companies whose businesses are most exposed to the domestic consumer, such as housebuilders and hotel and leisure companies’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.