Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSix ways to get paid in retirement

Generating a steady income from the markets in retirement isn’t as hard as you might think. Doing some basic research and understanding the risks involved with certain investment products are good starting points. In this article we’ll discuss these topics and more in order to help you find that prized stream of cash.

Anyone deciding to stay in the markets instead of generating a fixed income through an annuity needs to think about where their money is invested. The goal is to earn a continuous stream of money through dividends as well as avoiding capital losses.

Investment funds can be a better route to take than individual shares as you should get instant diversification.

Actively-managed funds let you benefit from someone else doing all the hard work of picking stocks or other asset classes. Passive products such as exchange-traded funds typically come with lower fees and let you track the performance of a wide range of markets, sectors or themes.

DON’T JUST PICK THE HIGHEST YIELD

There are plenty of options in the market but not all are good paths to follow. For example, some actively-managed funds may offer high yields because they are high risk products. You need to understand exactly what they are investing in.

Some passive products work off rules that track the highest yielding stocks. That sounds interesting but it is important to consider that many of the yields from the underlying portfolio are optically high because the market doesn’t believe the earnings forecasts for the relevant companies and this has ultimately weakened their share price. A dividend cut could be just around the corner.

The key message is that knowing what to avoid is equally as important as knowing what to buy when it comes to investing.

ARE YOU BEING COMPENSATED ENOUGH FOR THE RISKS TAKEN?

The general rule in investing is that higher yields equate to higher risk. The yield is a way of compensating you for taking on extra risks.

Sources of higher yields include debt-related funds such as Honeycomb (HONY) which yields 7.1% and asset-backed investment trusts which include TwentyFour Income Fund (TFIF), yielding 6.3%.

One of the highest yielding investment trusts is CATCo Reinsurance Opportunities (CAT) at 14.3%. On paper the yield is extremely attractive versus the typical sub-2% rates you would get on cash savings in the bank. However, look closer and you may think twice about wanting to get involved.

CATCo’s strategy is to invest in insurance products linked to catastrophe reinsurance. The shares have lost three quarters of their value over the past 12 months as the managers got their risk models wrong and underestimated losses from US hurricanes and wildfires.

WHAT ABOUT INCOME FROM BONDS?

Bonds are often considered to be lower-risk products, particularly ones issued by governments or high-quality companies. The potential rewards are therefore lower because they are widely considered to be safer options when it comes to collecting the regular income they offer (known as coupons) and getting your capital back at the end of the bond term.

Someone in retirement may find the rates on bond funds are too low for their income needs. For example, iShares Global Government Bond ETF (SGLO) yields a mere 1.2%.

However, bond funds can still play an important role in a diversified portfolio, particularly if equity markets go through a rocky patch and you need to have at least some portion of your portfolio which isn’t falling in value.

You can still make capital losses from bonds and there is no guarantee you will get your money back at the end so don’t think of them as completely risk-free.

Going for equity income funds should get you a better rate of income but the returns are not always significantly better than cash or bonds. For example, Neptune Global Income (B91RFZ2) yields 2.29% compared to SmartSave which is paying 2% on a one-year fixed rate savings account.

You have to ask yourself whether such an equity income fund is worth the extra risk for a mere 0.29% additional income rate in this example.

ARE INFRASTRUCTURE FUNDS A GOOD OPTION?

Infrastructure funds have been popular among investors – both those accumulating wealth and those already in retirement – because many offer good yields, typically in the range of 4% to 6%. For example, HICL Infrastructure (HICL) yields 4.9% and Foresight Solar Fund (FSFL) yields 5.7%.

Infrastructure can be a good source of income because you get exposure to assets which generally have predictable cash flows and are often in highly regulated markets. However, infrastructure projects can encounter unforeseen delays, something which was the case with Foresight Solar in 2018.

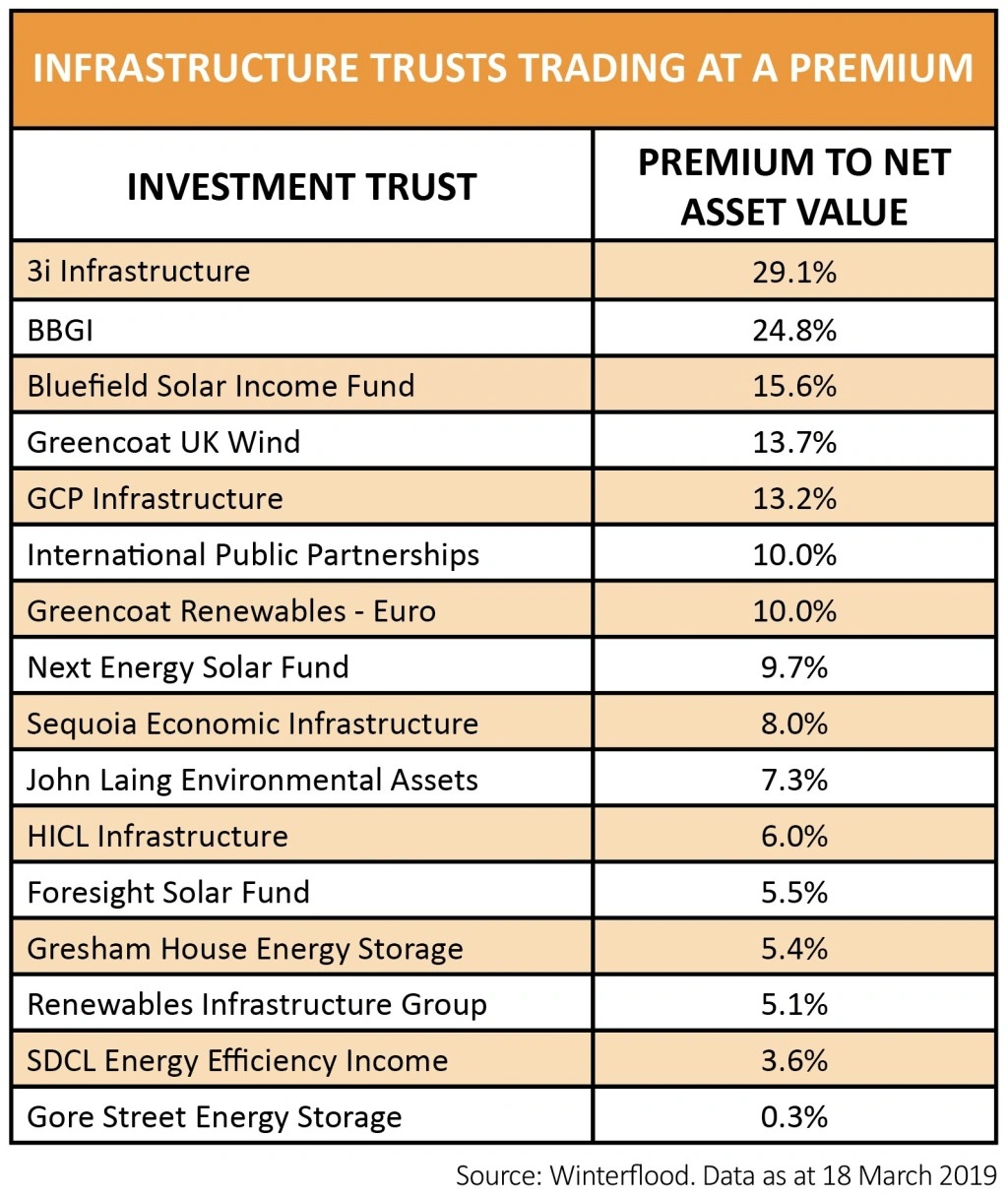

Many infrastructure investment trusts trade at significant premiums to net asset value (often 10% or more) so you are paying much more than the value of the assets are worth. There is a risk the market goes off this sector and the shares de-rate back towards fair value. In this scenario you could be hit with a capital loss.

You may be better off looking at open-ended funds (unit trusts and Oeics) for exposure to infrastructure where you wouldn’t pay a premium to net asset value. We’ve picked one later in this article.

Read on to discover its identity and five other funds which we believe to be good investment ideas for someone in retirement who is happy to take on some element of proportionate risk.

We suggest you consider most or all of them to act as a blended source of income. All the yield information refers to dividends paid in the past 12 months and none of the income payments are guaranteed. Any reference to the term ‘OCF’ stands for ongoing charges figure.

TWO NEW AJ BELL INCOME FUNDS BOTH TARGET 4% YIELD

AJ Bell has launched two new income funds which may suit someone who wants to obtain a better income than cash in a bank or building society account. They both aim to pay 4% yield although this is not a guaranteed return. The ongoing charges figure is capped at 1%.

The funds blend a mixture of passive products and actively-managed funds. AJ Bell Income Fund (BH3W755) is a multi-asset fund with investments in equities, bonds and property. AJ Bell Income and Growth Fund (BH3W799) is similar with the addition of alternative investments like infrastructure but no exposure to bonds.

‘Our starting point is finding decent income for decent cost. For example, you can get passive infrastructure funds yielding 2% and costing 0.65%, yet there are also actively-managed funds yielding 4% for not much more cost,’ says Matt Brennan, head of passive portfolios at AJ Bell.

He explains that some of the funds’ income will be generated by passive products which follow specific rules to find dividend-paying assets.

‘You can get ETFs that rank FTSE 350 stocks by yield. We don’t like these products because you are chasing income at any cost. The ones we’ve selected have a quality income tilt. For example, one range we use is iShares Quality Dividend products which only includes companies which have strong fundamentals as well as a higher yield. This ensures the yield is not just high, but more importantly sustainable.’

The AJ Bell Income Fund may appeal to someone in the latter stages of retirement because the product has been designed to keep the capital fairly flat over time, although that isn’t guaranteed to happen.

The AJ Bell Income and Growth Fund could suit someone either in the early stages of retirement who want their investments to keep growing, or even someone younger who likes the benefits of income or wants to enjoy compounding benefits by reinvesting all dividends.

SIX OF OUR FAVOURITE INCOME FUNDS FOR INDIVIDUALS IN RETIREMENT

1. TB EVENLODE INCOME (BD0B7D5)

YIELD: 3.30% – OCF: 0.90%

This should be a core holding for income investors wanting exposure to high quality companies. The fund managers look for companies with high returns on capital and strong free cash flow. They believe these attributes can help identify companies capable of sustainable dividend growth above the rate of inflation.

You’ll get exposure to names like consumer goods giant Unilever (ULVR), drinks group Pepsico and comparison website Moneysupermarket (MONY).

A 3.3% yield is decent in the current environment and you should also expect some level of capital gains. Over the past five years it has delivered 9.7% annualised returns versus 4.1% from the FTSE All-Share total return index.

What’s really interesting is the lack of exposure in the top holdings to some obvious names which crop up in many income funds such as Royal Dutch Shell (RDSB) and Vodafone (VOD). That’s because Evenlode prefers to put money into companies that don’t need to spend a lot of money to keep their business ticking over and it also prefers to avoid firms with high debt levels.

It is worth noting that Evenlode’s website displays a message saying the fund is soft closed. This means it has put up restrictions such as a 5% initial charge to put off new investors as it doesn’t want its fund to get too big in size. Some investment platforms such as AJ Bell Youinvest can still accept new investment into this fund without the 5% initial charge.

MAN GLG UK INCOME (B0117D3)

YIELD: 4.29% – OCF: 0.90%

Man GLG UK Income has minimal overlap with the aforementioned product from Evenlode as fund manager Henry Dixon takes a value rather than quality approach. He buys stocks that are much cheaper than you’d typically find in Evenlode’s fund and the yield is greater at 4.29%.

He avoids value traps by focusing on cash, cash flow and assets. Value investing ultimately means buying something when it is cheap and selling when it becomes fair value. As such, the Man GLG fund can have high levels of turnover and so transaction costs can be elevated.

Dixon’s track record is good: the fund has delivered 8% annualised return over five years, twice that of the market. Miner BHP (BHP), housebuilder Bellway (BWY) and banking group Lloyds (LLOY) currently feature in the portfolio of approximately 70 stocks. Dixon also invests in some corporate debt and convertible bonds.

MONTANARO UK INCOME (BYSRYZ3)

YIELD: 3.67% – OCF: 0.86%

This fund is more suited to someone in the very early stages of retirement who wants to obtain some capital growth from their portfolio as well as income.

While you may think it is odd suggesting a small cap fund as a source of income in retirement, there is a slight twist to this product in that you won’t find lots of high-risk AIM stocks in its portfolio. Instead you get exposure to more established businesses, some of which are really mid-caps in size.

The companies in its portfolio are cash generative, well-managed businesses, often with founding management still owning large stakes. Example names include self-storage group Big Yellow (BYG), piping manufacturer Polypipe (PLP) and leisure group Cineworld (CINE).

The fund had a tough year in 2018 with 14% loss versus 24% positive return in the previous year. That was predominantly down to 2018 being a tough year for smaller companies including the worst fourth quarter since the global financial crisis.

Don’t let that put you off. Montanaro has a big research team and is very good at finding opportunities in the small and mid-cap space.

HENDERSON INTERNATIONAL INCOME (HINT)

YIELD: 3.50% – OCF: 0.83%

Henderson International Income will give you access to global markets excluding the UK. The latest factsheet shows exposure to a wide range of geographies including the US, Switzerland, France, Netherlands, China and Sweden.

The investment trust’s objective is to provide a high and rising level of dividends as well as capital appreciation over the long-term.

The current portfolio includes some really big names in the world of business including Microsoft and Coca-Cola. It tends to hold between 60 and 80 positions and has a strong value focus. It holds stocks until a cheap valuation re-rates to a fair valuation.

Henderson says most of the companies in its portfolio increased or maintained their dividends in its financial year to 31 August 2018. It also says dividend growth in this period was driven by both earnings growth and an increase in the proportion of earnings paid out as dividends.

JUPITER ASIAN INCOME (BZ2YMT7)

YIELD: 3.88% – OCF: 0.98%

This fund has a fairly concentrated portfolio of 40 to 50 stocks and follows a strict investment criteria. It invests in companies listed or located in Asia Pacific, including Australia and New Zealand, but not Japan.

Fund manager Jason Pidcock will only consider a company that is well-managed and well-positioned in its own industry. Companies need to have a scalable business model and must be committed to paying dividends. The shares also have to be good value for money rather than paying any price for quality names.

The portfolio includes stakes in investment bank Macquarie, Samsung Electronics and Ping An Insurance.

LEGG MASON IF RARE GLOBAL INFRASTRUCTURE INCOME (BZ01WT0)

YIELD: 5.17% – OCF: 0.93%

Earlier in this article we talked about the risks of paying a premium if you accessed infrastructure through investment trusts. The Legg Mason product avoids this situation because it is an open-ended fund.

Investors in the income fund are benefiting from the expertise of a true specialist in the field of infrastructure, namely Rare Infrastructure which was founded in 2006 and acquired by Legg Mason in 2015.

The fund’s model is to invest in a range of different companies involved in gas, electricity and water utilities, toll roads, airports, rail and communication infrastructure.

This is the sort of fund you want to hold for at least five years and you shouldn’t expect capital gains every year.

DISCLAIMER:

AJ Bell is the owner and publisher of Shares. This article is not a recommendation to buy AJ Bell’s new income funds referenced in the feature – it is for information only.

The author owns shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.