Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

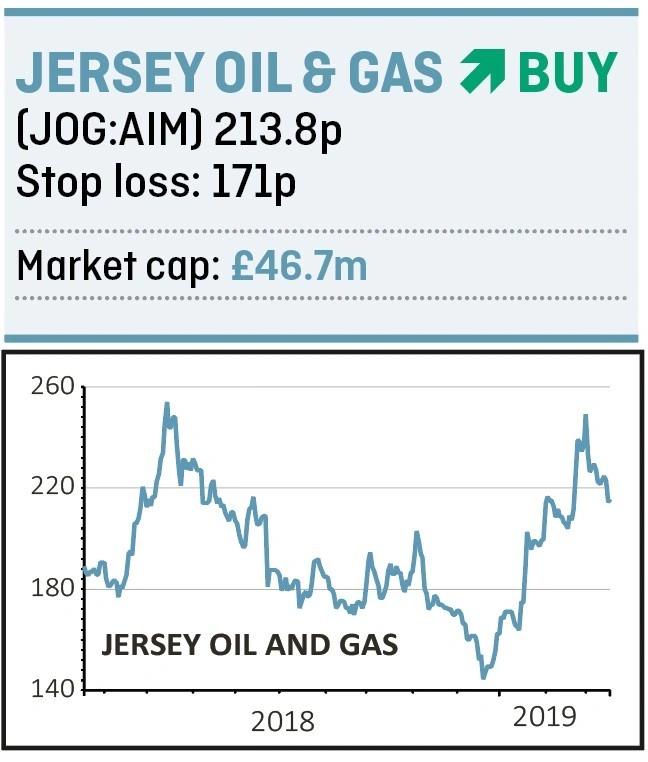

magazineJersey Oil & Gas is about to quantify its North Sea oil discovery

Oil exploration is a notoriously risky enterprise. It is often seen as an activity with a binary outcome for listed companies – either they find oil and the share price gushes higher, or they don’t and the shares crash.

However, we’ve spotted a small cap oil play which is drilling a well that could provide a significant catalyst for the stock but with the potential for much more limited downside if the news disappoints.

AIM-quoted Jersey Oil & Gas (JOG:AIM) two years ago made a large discovery in the North Sea. Verbier is located on the P2170 licence in which Jersey has an 18% stake and is partnered by Norway multinational Equinor and a subsidiary of Japanese conglomerate Itochu Corporation in CIECO UK.

The partners are currently drilling an appraisal well to determine just how much oil it has found. The results are expected by the middle of the second quarter this year.

Current estimates put the size of the discovery at between 25m and 130m barrels of oil equivalent. And, according to analysis from broker FinnCap, the shares are currently pricing in something towards the lower end of that spectrum.

Proving up the mean estimate of resources at 69m barrels of oil equivalent could be worth 500p per share and the upper end would have a value of £10 per share, multiples of the current share price.

This is one of at least three prospective drivers for the shares in 2019. 3D seismic is currently being shot over P2170 and this could be a precursor to firming up a drilling plan for the Cortina prospect, possibly in 2020.

The other catalyst is the results of its participation in a North Sea licensing round. This encompasses acreage around Verbier which Canadian bank BMO believes could contain an undeveloped resource of up to 300m barrels of oil equivalent. News on this front is expected at some point in the second half of the year.

With more than £20m worth of cash on the balance sheet at the last count and zero debt, the company is well funded for its 2019 capex requirements of between £7m and £10m.

The company is also on the hunt for acquisition opportunities in the North Sea to add some producing assets to its portfolio. This would offer cash flow to help fund future activity and would also take advantage of the tax losses Jersey has racked up by investing in exploration as these can be offset against production revenue.

However, it is being picky having assessed and rejected somewhere around 50 deals. We find this patience reassuring.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.