Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to measure the earnings power of corporate America

A sour trading update from Apple leaves those investors who have exposure to US equities – and technology stocks in particular – with a few questions to answer.

Although disappointing demand in China grabbed most of the headlines, Apple’s chief executive officer, Tim Cook, also blamed weaker growth across emerging markets more generally, a stronger dollar and a slower-than-expected product upgrade cycle in the West – all issues which could affect not just Apple but any US-based multi-national.

This is why the forthcoming quarterly reporting season in America will be a particularly important one, as investors try to get a read on whether the second-half sell-off suffered across US equities in 2018 was merited or not.

VALUE CASE

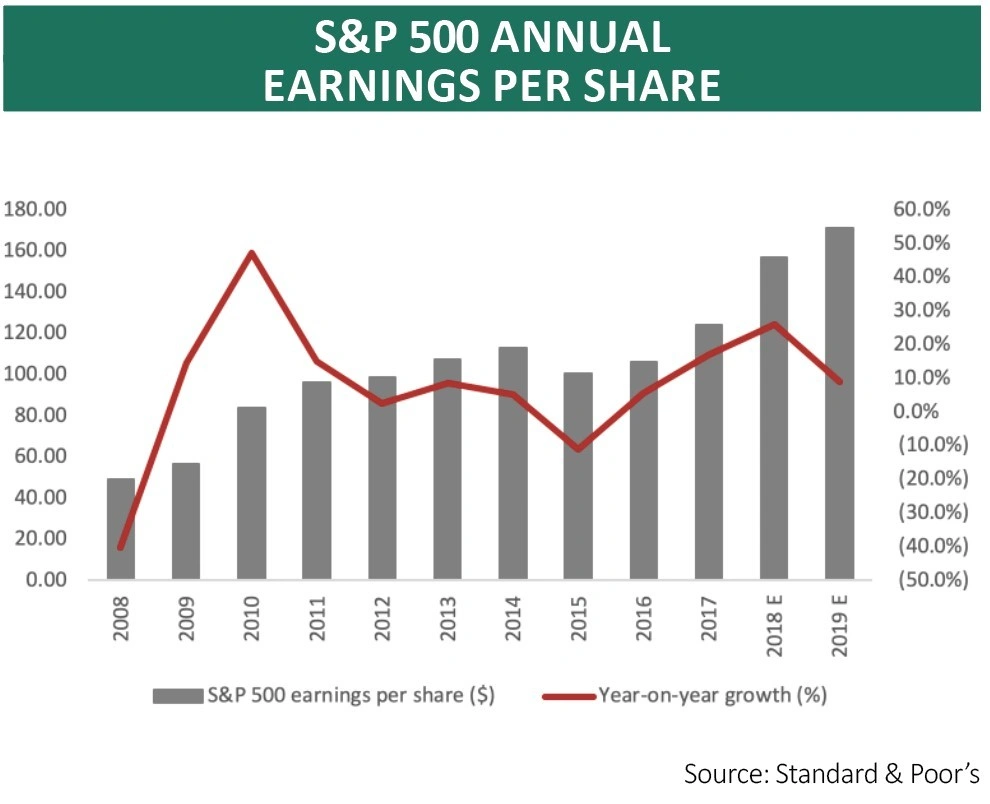

According to research from Standard & Poor’s the pull-back leaves the US stock market on 14.3 times forward earnings per share estimates of $171 for the S&P 500 in aggregate for 2019.

Bulls will argue that a 9% increase is perfectly achievable, especially with the US economy primed to rack up GDP growth of 2.5% to 3.5% for 2019. Throw in that 9% earnings increase, some multiple expansion from that 14.3 times level if confidence returns – and a dividend yield of around 2.1% - and you can see how forecasts of double-digit returns from US equities for 2019 may easily add up.

Bears will challenge that 9% growth estimate by pointing out that the forecast 2018 earnings per share figure for the S&P 500 of $157 already represents a record high. With corporate profit margins of 12.1% in Q3 2018 also a record high, it seems legitimate to ask how US corporate earnings can keep on growing, as the benefits of the Trump tax cuts fade and higher wages, higher interest bills (thanks to the Federal Reserve’s four interest rate increases last year) and the stronger dollar make their presence felt.

EARLY TEST

Hopes for a trade settlement between America and China, a softer approach from the US Federal Reserve and the announcement of both fiscal and monetary stimulus by Beijing’s President Xi Jinping have given markets a boost but the imminent fourth-quarter results season will be good early test for the US equity market – especially as Apple, silicon chip maker Micron (which gave out a profit warning just before Christmas) and Delta Airlines have got it off to a bad start.

Around 30 of the S&P 500 index’s members report quarterly results in the coming week. Most of them are financial stocks, including megabanks Citigroup, JPMorgan Chase, Wells Fargo, Bank of America, Goldman Sachs and Morgan Stanley.

Investors will be looking for strong numbers here as the banks sector was a terrible stock market performer the world over in 2018 – and if there is one sector that all portfolio-builders would like to know is healthy some ten years after the Great Financial Crisis then surely it is the banks.

Overall, Standard & Poor’s is looking for 26% earnings per share growth, helped by the Trump tax cuts for the final time – the beneficial comparative effect will drop out from the first-quarter results that will be released in April and May.

MARGIN FOR ERROR

The second-half retreat in US equities to around the 2,500 mark on the S&P 500 at the time of writing leaves the headline index some 14% below its September all-time high. And the fact that US stocks are now 14% cheaper than they were makes them more interesting.

However, tempting as that 14.3-times forward multiple may be, there may be still little room for disappointment when it comes to the quarterly reporting season.

The 10% hammering handed out to Apple on the day of its warning suggests as much, as does the work of Professor Robert Shiller.

His cyclically-adjusted price/earnings ratio (CAPE) calculation, which is based on inflation-adjusted historic earnings on a ten-year rolling basis, still argues that US stocks may be overvalued, at 29 times forward earnings.

The S&P 500 reached a CAPE rating of around 30 times on two prior occasions, in 1929 and 1998-2000, and both of those episodes ultimately ended badly.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.