Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan you make money from investing in pub companies?

Britain is a nation that loves a pint of beer or a glass of wine, yet younger generations aren’t as enamoured with alcohol.

More under-65s were not drinking at all in 2017 compared to 2005 according to the Office for National Statistics.

While this trend may be welcomed by the overburdened NHS, pub operators may understandably feel differently as a reduction in demand for alcoholic drinks could weigh on their earnings and growth.

Should investors go teetotal with their portfolios and ditch pubs entirely? We think that’s a bit extreme as pubs have historically been decent investments and they remain an important part of everyday life, despite some shifting trends.

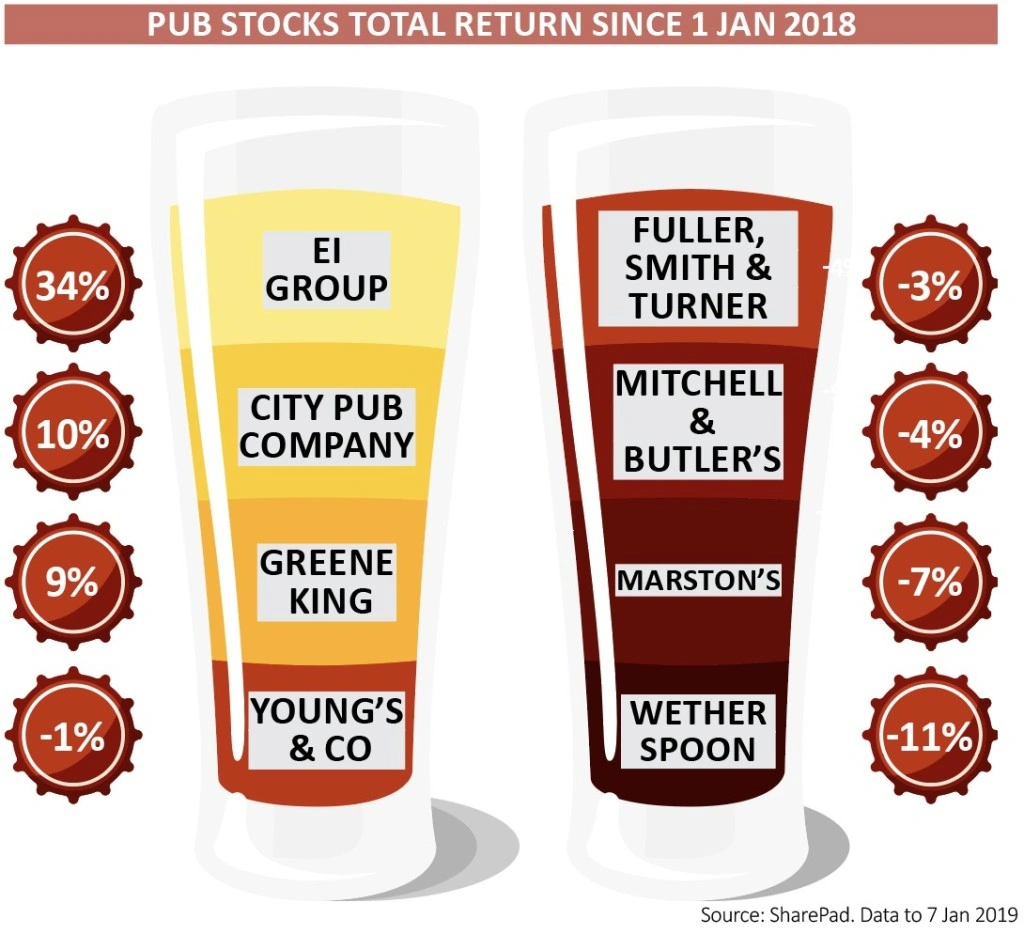

In a year where most stock markets fell around the world, three UK-listed pub companies would have delivered shareholders with a positive total return (share price gains and dividends) since the start of 2018. These are City Pub Group (CPC:AIM), EI Group (EIG) and Greene King (GNK).

Yes, the sector is battling various cost pressures and a mixed appetite from consumers towards casual spending, in addition to reduced alcohol interest among younger adults. But in the long term we still think there may be opportunities for select companies in the sector.

We like EI Group as management seem focused on the operations once again, having previously been distracted by years of non-stop questions about the group’s large debts. Net debt has been reduced to £2bn which equates to a 56% loan-to-value.

Investors should expect returns to come from a rising share price with EI as it is not expected to pay dividends in the near-term.

We like Young’s & Co (YNGA:AIM) for its premium estate and a proven dividend growth track record, although we recognise the shares aren’t cheap. They are trading on 18.6 times forecast earnings for the year to March 2020. Although the prospective yield is only 1.6%, this is a great stock for reinvesting a growing stream of dividends so as to enjoy compounding benefits.

Panmure Gordon analyst Matthew Webb argues that Young’s premium rating is warranted thanks to its ‘far superior estate, exceptional like-for-like record and conservative balance sheet’.

Greene King’s shares are considerably cheaper than Young’s, trading on 8.6 times forecast earnings for the year to April 2020. There is a good reason why its rating is low: earnings are forecast to stay flat until at least the 2021 financial year. Analysts have pushed through numerous earnings downgrades over the past few years and the business seems to have lost its way.

Chief executive Rooney Anand is seen as an old-school operator with traditional values. He leaves the company later this year and investors may hope that a more modern-thinking replacement breathes new life into the business.

WHY DID SOME PUBS STRUGGLE IN 2018?

Investors may not be surprised by the list of headwinds dragging on the sector as pub operators have struggled with the weather-related impacts, higher labour costs and more competition for dining out.

The depressed high street environment is another factor, but some observers believe the pubs are faring a good deal better than their counterparts in the retail sector.

Canaccord Genuity’s leisure analyst team says: ‘In contrast to the retail sector which had an abysmal end to 2018, circumstances appear more upbeat for the eating and drinking out sector.

‘Christmas Day continues to grow in importance to the pub companies as families increasingly prefer the treat of a pub event to the effort of cooking a feast at home. Greene King reported that Christmas bookings were well ahead of last year at its interims.’

Over the scorching summer, there was also a short-term boost as people flocked to pubs to enjoy the World Cup. Perhaps surprisingly given the societal decline in drinking, wet-led pubs performed better through 2018, while pubs with more exposure to food sales struggled as customers were spoilt for choice thanks to an over-saturated casual dining market.

EI TAKES THE CROWN

The UK’s largest pub operator EI delivered the best returns for shareholders in 2018, driven by progress on rebuilding its business following years of being weighed down by significant debt. It was also in the right part of the market with its drinks-led proposition – food was less of a driver for the sector compared to previous years.

Investors may be also have been bidding up the shares ahead of a potential catalyst as EI plans to sell its portfolio of commercial properties to shore up its balance sheet and possibly reward shareholders with a special dividend.

Canaccord Genuity analyst Nigel Parson says the bids are estimated to be valued at between £320m to £350m, but the final price could be up to £400m.

EXPANSION STRATEGY PAYING OFF

City Pub Group is newest company among the UK-listed pub stocks, growing from a start-up in 2011 to an estate of 42 pubs, which are mainly drinks-led.

In the six months to 1 July, nine new pubs have been opened. City Pub Group is ambitious in its growth strategy as it wants to double in size by 2021.

With modern bars and restaurants in affluent areas in England and Wales, including a contemporary pub near Brighton’s i360 tower, City Pub arguably has more unique assets than its rivals.

It also has the financial firepower to hit its acquisition target of between eight and 10 new pubs, and even pursue further openings.

Liberum analyst Anna Barnfather argues Brexit uncertainty and revised business rates may work in the company’s favour as it faces less competition for sites at potentially cheaper market prices.

PREMIUM BENEFITS

Shares in Young’s failed to take off despite a robust performance at its pubs, which boast strong interior design, many riverside locations and fresh food made with local ingredients. We don’t think there is anything to worry about, as Young’s has a good track record of delivering earnings growth which is the ultimate driver for the share price.

Over the summer, its pub gardens attracted thirsty drinkers with Young’s posting double-digit growth in drink sales in the 26 weeks to 1 October.

Sales and profitability have been on the rise thanks to investment in its premium estate. Young’s is generous with its dividend policy, delivering its 22nd consecutive year-on-year interim dividend hike, leaving the payout at 9.9p per share.

WHO ARE THE SECTOR LAGGARDS?

Investors would have lost money in 2018 investing in Marston’s (MARS), Mitchells & Butlers (MAB), Fuller, Smith & Turner (FSTA) among others.

With a 14.4% share price decline over the last year, Marston’s has been struggling with falling food sales at its pubs.

Many investors are drawn to Marston’s (and Greene King) for generous dividends, yet the former failed to lift its dividend at the latest full-year results, reported in November.

The company is taking a cautious view of life in 2019 and will reduce its normal capital expenditure plans by £30m including a reduction in the number of new pub, bars and lodgings.

The company is also hoping to reduce debt and slash pension contributions to improve cash flow and its balance sheet.

SPENDING MONEY TO MAKE MONEY

Adjusted pre-tax profit fell by 1% in Fuller’s latest half-year results to £23.6m. Chief executive Simon Emeny said the business had decided to ‘front-load’ its investment programme, buying new pubs and investing in its brewing and IT operations.

Peel Hunt analyst Douglas Jack is confident Fuller’s is making the right decisions even if it is impacting profitability, flagging further expansions and refurbishments are in the pipeline.

As we enter 2019, there are little signs that the pressures facing the pub sector will let up so Fuller’s attempt to get is estate in the best possible shape looks a prudent strategy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.