Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow worried should you be about China?

A 2 January warning from Apple that sales and earnings for the three months to December were hurt by weak Chinese demand sent a shockwave through world markets, so does this mean we should be worried about China?

According to chief executive Tim Cook, Apple was wrong-footed by ‘the magnitude of the economic deceleration in Greater China’, blaming it for ‘most of our revenue shortfall to our guidance and over 100% of our year-over-year worldwide revenue decline’.

Analysts and journalists have suggested that Apple’s selling prices are too high, especially for the iPhone, but could falling handset sales be a sign that Chinese consumers no longer feel like spending?

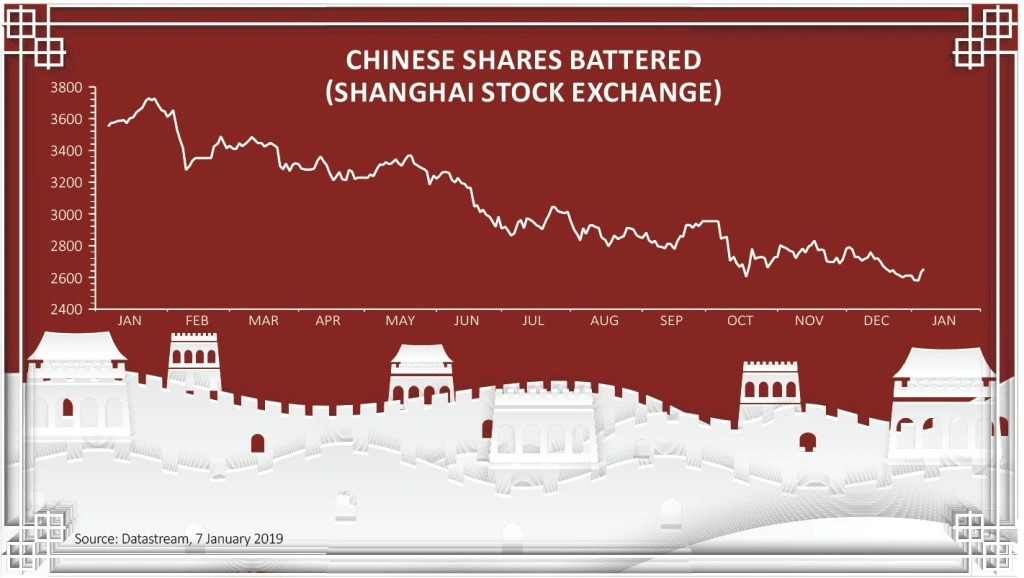

MANUFACTURING SURVEYS SUGGEST ECONOMY IS SLOWING

Last week the privately-sponsored Caixin manufacturing purchasing managers index (PMI) surprisingly fell below the key 50 level for the first time since May 2017.

A reading above 50 signals expansion while a number below 50 usually signals contraction.

This was just days after the official government-sponsored PMI fell to its lowest level since February 2016.

Moreover in the quarter to the end of September, Chinese GDP growth was 6.5% which was below estimates and the lowest level since the financial crisis.

Sensing a slowdown, commodity investors have been piling out of copper, where China is the world’s largest consumer, and into gold and silver.

As a result copper prices are now at 18-month lows while gold prices are at six-month highs.

ARE TRADE TARIFFS TO BLAME?

It is hard to gauge the extent to which a slowdown in Chinese demand is due to trade tariffs.

The 25% tariffs slapped on Chinese steel imported into the US from March last year have effectively stopped exports dead in their tracks. That has meant a surplus of steel on world markets which has depressed prices.

However Chinese exports overall have grown this year with November’s trade surplus hitting nearly $45bn, the largest level since December 2017 and well above the market forecast of $34bn.

China’s trade surplus with the US, its largest export market, hit a record high of $35.5bn in October as exports outpaced imports suggesting that Trump’s tariffs may actually be hurting US firms more than Chinese firms.

US manufacturers are hardly dancing in the streets, with the much-followed Institute of Supply Management’s PMI index of factory activity suffering its biggest drop last month since October 2008, sending tremors through US stocks.

Trump’s reaction has been to call a 90-day truce in the tariff war, while US and Chinese trade negotiators are due to meet in Beijing this week in a bid to avert further trade tensions.

IS THE DOMESTIC ECONOMY SLOWING?

Consumption accounts for a steadily growing share of the Chinese economy but in a worrying sign retail sales growth hit its lowest level in 15 years last month.

Car sales have actually gone into reverse falling 18% in November, the sixth consecutive month of declines.

The total number of vehicles sold last year will be down on 2017, the first annual fall since the early 1990s. China is the world’s largest passenger-car market.

Part of the reason for lower sales is a government crackdown on non-bank lending such as peer-to-peer platforms, which is part of a wider policy of reining in easy credit.

Another part is that Chinese consumers have tended to rely on the stock market and property prices to generate surplus income.

Last year however the stock market lost 25% of value meaning that $2tn of ‘wealth’ has disappeared from investors’ pockets.

Also property values, which have been rising for many years, have levelled out with new home prices in Beijing and Shanghai more or less flat over the last year.

The government is doing what it can to stimulate the economy, reducing business taxes and cutting its reserve requirement so that the banks can keep lending, but investors seem unconvinced.

WHICH STOCKS COULD BE AFFECTED?

Plenty of UK stocks have exposure to China but miners and luxury stocks look to be the most exposed in terms of sales and profits.

On the day that Apple warned, mining stocks were instantly marked down with BHP Group (BHP) losing 2%, Antofagasta (ANTO) losing 4% and Glencore (GLEN) losing 4%.

Meanwhile clothing firm Burberry (BRBY) dropped 6% and in Paris shares in luxury conglomerates LVMH and Kering lost 4% and 5% respectively.

Aston Martin Lagonda (AML) saw its shares fall 3% as most of its growth this year has come from China.

In terms of smaller-ticket consumer spending, drinks makers Diageo (DGE) and Remy Cointreau generate significant sales in China and consumer health giant Reckitt Benckiser (RB.) has large exposure through its infant formula business.

In the investment trust world Edinburgh Dragon Trust (EFM) is a pure play on China and therefore worth monitoring.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.