Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBargain UK stocks: the experts say ‘buy now’

The broader UK stock market is very cheap on multiple metrics as a result of investors worrying how Brexit will impact the UK economy and domestic earners.

The fear has spread so that many investors are nervous about UK equities in general, even though a lot of the companies generate their earnings overseas. This situation presents an opportunity to buy some real bargains.

Many fund managers and investment experts say the time to buy is now rather than waiting for more certainty over the direction of Brexit.

In this article we look at UK equities in the context of other markets and reveal five stocks currently exciting fund managers.

WHY THE EXPERTS ARE BULLISH

‘It might be counterintuitive to think that the UK market could be among the top performers globally in the year that we leave the EU (if indeed we do). But markets have a way of confounding expectations and surprising the consensus,’ says Alex Wright, fund manager of investment trust Fidelity Special Values (FSV).

He is confident that clarification in the relationship between the UK and EU would act as a catalyst for investors to revisit the UK equity market.

Sterling began to rise last week on talk that the EU would wave through the draft Brexit deal, and indeed that was confirmed on 25 November. However, the deal is not yet set in stone.

Getting parliamentary approval is the big hurdle still to clear and success would be the real, material catalyst for investors to take another look at the UK market.

There is no guarantee that MPs will vote in favour of Theresa May’s Brexit plan and failure could cause another stock market wobble. Investors must therefore consider the near-term risk to any UK-related investments they make in the run-up to the parliamentary vote, confirmed to happen on 11 December.

The price you would pay from waiting is the loss of potential gains from the market rebounding upon a smooth Brexit agreement.

WHY BUY NOW?

‘One thing I have learned from investing in unloved companies is that you shouldn’t necessarily wait for good news to become obvious before investing. By investing when all the bad news is “in the price” and no good news is expected at all, you put the odds in your favour. I think this is a situation we are in in the UK at the moment,’ says Wright.

Paul Mumford, a fund manager at Cavendish Asset Management, believes there is a good chance for UK domestic earners to bounce on the stock market in 2019.

He is little surprised that ‘Red October’, the big sell-off in equities last month, took as long to materialise as it did. His view is that the uncertainties created by long-winded and complex Brexit negotiations, plus the drop in sterling, could have triggered something similar earlier in the year.

The plus side of October’s market adjustment is that it has created a host of good opportunities on UK equity markets. ‘There’s great value out there,’ he says, particularly among companies with strong UK domestic earnings if the pound strengthens through 2019.

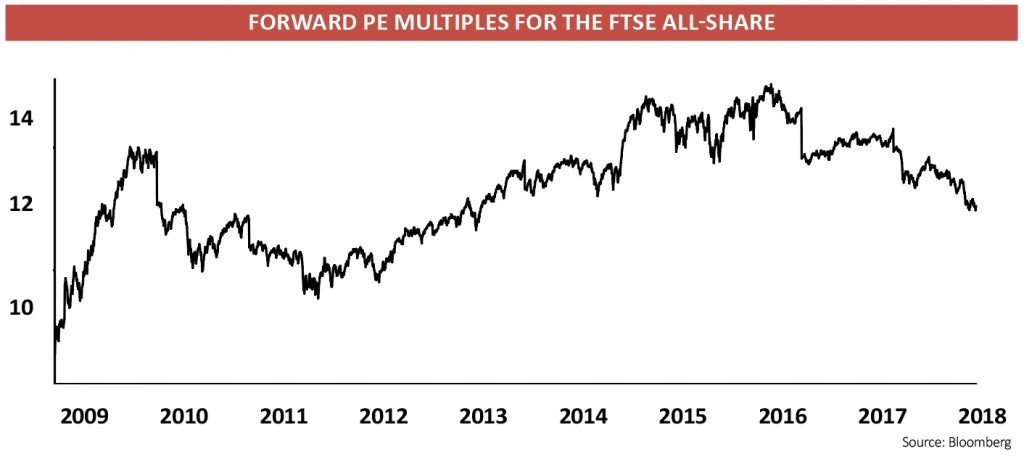

HOW CHEAP IS THE UK MARKET?

At the start of the year we were paying almost 16 times forward earnings for the broad UK equity market (as dictated by the FTSE All-Share index), now we’re paying less than 13-times, equivalent to a 20% discount. The same percentage gap is noted on the FTSE 100 and FTSE 250 indices.

Approximately half of the FTSE 250’s constituents generate their earnings from the UK and about one quarter of the FTSE 100 is considered to be UK domestic.

UK CREDIT RATINGS

Until 2013 the UK had an AAA sovereign bond rating, the highest possible level of credit rating.

The big three credit agencies, Fitch, Moody’s and S&P, have subsequently cut their ratings due to austerity, high levels of indebtedness and most recently fears that Brexit will damage the economy.

S&P still rates the UK as AA but its outlook is negative which means there is more than a one third chance of a downgrade in the next two years.

To put that in context, Italy is rated BBB by S&P which is six ‘notches’ or levels below the UK’s rating while Greece and Turkey are rated B+ which is 10 notches below the UK.

Even in a worst-case ‘no-deal’ Brexit scenario it is unlikely that the UK’s rating will approach those of Italy, Greece or Turkey.

The biggest companies in the FTSE 100 are global businesses and as such they tend to have the highest credit ratings.

For example Royal Dutch Shell (RDSB) sports an AA- rating (just one notch below the UK government) and GlaxoSmithKline (GSK) sports an A+ rating (two notches below).

More UK-focused companies will have lower ratings; for example, Lloyds (LLOY) has a BBB+ rating. This may not look great alongside GlaxoSmithKline but it’s still one notch higher than Italy’s rating. (IC)

In addition to Brexit investors have been spooked by rising interest rates (particularly in the US) and US bond yields exceeding 3%. ‘Rising bond yields tend to depress the multiple we are willing to prescribe to earnings, which causes an equity de-rating. They also place pressure on stretched balanced sheets,’ comments Henry Dixon, a fund manager at Man GLG.

He says investors should consider the current state of affairs with regards to earnings expectations, as they are a ‘crucial part of the investment game’, namely the fact that upgrades or downgrades are major share price catalysts.

The accompanying tables show the earnings expectations at the start of certain years and then how the market performed over the respective 12-month period.

The first table shows the years where the market was most optimistic – occasionally resulting in a negative return. The second table shows years where the market was most pessimistic in terms of earnings expectations and, low and behold, most of the periods had a strong positive return.

‘The market is looking for 5% to 6% earnings growth in 2019 from UK equities which is the lowest data point we’ve had over the past 30 years,’ says Dixon. As you can see from the historical examples below, low expectations could lead to decent returns assuming Brexit doesn’t get messy.

LOWER VALUATIONS VERSUS FOREIGN PEERS

Another way of measuring the level of cheapness in the UK market is to compare big London-listed stocks with their overseas counterparts. Here are some examples:

Construction group CRH (CRH) is trading on 11.4 times 2019 forecast earnings versus New York-listed Vulcan Materials which is on 21-times.

Aerospace engineer Meggitt (MGGT) is trading on 13.9 times 2019 forecast earnings versus New York-listed United Technologies which is on 16.2-times.

Banking group Lloyds (LLOY) is trading on 7.2 times 2019 forecast earnings versus Euronext-listed KBC which is on 10.6-times.

Insurance and asset management group Aviva (AV.) is trading on 6.9 times 2019 forecast earnings versus Xetra-listed Allianz which is on 9.8-times.

‘The FTSE All-Share PE (price-to-earnings ratio) is trading at an approximate 15% discount to the FTSE World index PE. That is cheaper than during the financial crisis a decade ago, and you would have to go back to the late 1980s and then to the mid-1970s to find similar situations,’ says Dixon.

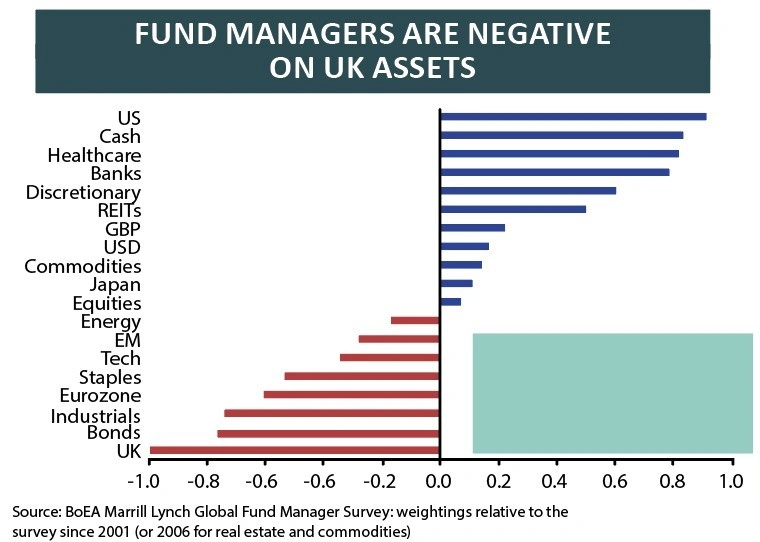

LOW APPETITE FOR UK STOCKS

Bank of America Merrill Lynch asks fund managers around the world every month how they are positioning their portfolios and UK stocks have been consistently out of favour for a long time.

The latest survey finds that 27% of fund managers are underweight UK assets as the approaching Brexit deadline ‘stokes renewed uncertainty’. Underweight means holding a smaller amount of certain assets compared to their weighting in a benchmark index.

HOUSEBUILDERS IN NEGATIVE TERRITORY

London-listed housebuilders are almost exclusively focused on the UK and their share prices are heavily tied to what happens with the Brexit process.

The relief offered by a successful deal with the EU would not fully solve the issues they face, even if that could provide a sentiment-driven boost to housebuilding stocks.

The industry faces an unhelpful combination of flat or falling house prices, partly driven by economic uncertainty but also a consequence of the regulatory impact on the buy-to-let space.

Furthermore, rising costs are weighing on the sector including labour as the availability of workers is likely to be affected by whatever form the UK’s exit from the EU takes.

Some housebuilders are trading on double-digit dividend yields which is typically a sign that the market doesn’t believe the dividend or earnings forecasts.

However, some experts believe now is a good time to reappraise the sector following significant share price declines this year.

For example, the managers of Standard Life Investments UK Equity Unconstrained (B79X967) and Mercantile Investment Trust (MRC) both highlight Bellway (BWY) as an undervalued opportunity. Wesley McCoy from Standard Life describes it ‘one of the best operators in the market’. (TS)

‘Investors know that UK-focused stocks are cheap (many on single-digit PEs) and they are underweight. With growth elsewhere slowing down and GBP stabilising they are looking to reduce that underweight slowly,’ says Steve Davies, fund manager at investment trust Jupiter UK Growth (JUKG)

WHAT COULD HAPPEN NEXT?

It seems fair to suggest that Theresa May’s Brexit plan may not be approved first time by parliament, thus requiring revisions. Such news could cause a stock market wobble but we don’t believe it would cause long-lasting pain for investors.

No-one knows for sure at the moment so investors must take on board the risk that buying UK stocks could result in a loss before a gain.

Investors must also consider a far worse outcome. ‘I don’t think a hard Brexit outcome is an impossibility,’ says Oliver Brown, fund manager at MFM UK Primary Opportunities (B8HGN52). ‘The ramifications are unknown for the UK in terms of trading agreements, so a hard Brexit could cause a sharp de-rating in UK stocks. As such, it feels a roll of the dice with some equities at present.’

A Brexit deal approved without a major hitch may trigger a rally in the pound which would be negative for the FTSE 100’s large number of overseas earners as their share prices are sterling-denominated.

You must also consider that the Brexit deal could lead to a rise in inflation if the terms result in it being more expensive to buy goods from abroad. That could prompt the Bank of England to raise interest rates which theoretically would be negative for equities.

There are so many variables that investors should not consider buying UK equities today to be an easy win. Our view is that you should embrace the current state of fear to buy decent businesses as long-term holdings. There may be bumps along the way, but that always comes with the territory of investing.

WHY HAVE UK BANKING SHARES STRUGGLED THIS YEAR?

One of the big mysteries of the UK market this year has been the poor performance of the banks despite higher interest rates.

While the Bank of England has raised interest rates twice in the last 12 months, the FTSE 350 banking index is down 19% against a 10% fall for the FTSE 100.

Normally higher rates mean higher revenues as banks jack up borrowing costs and hold off on raising savings rates. With 3.5m mortgage borrowers on variable or ‘tracker’ rates the banks ought to be raking it in.

The problem is more savers are locking in fixed-rate deals to avoid higher charges. In the case of banking group CYBG (CYBG), 78% of its £25bn mortgage book is fixed-rate and in the past year 96% of all new mortgages were fixed.

At the same time companies are awash with cash and are sticking it on deposit. Almost all of the increase in CYBG’s current accounts was due to businesses stashing away cash.

The net result of these trends is that interest costs are rising while interest income from lending is falling, which is bad news for banks. Add in uncertainty over Brexit and no wonder investors are shunning the sector.

Auto Trader (AUTO) 434.5p

Auto Trader’s share price was hit in October when rival business Motors.co.uk was bought by Ebay and investors worried the latter would become a much stronger player in the car market. Fortunately Auto Trader’s half year results on 8 November helped to win back investor interest with strong numbers including pre-tax profit up 9% to £114.5m.

We continue to rate the business highly and so does Mercantile (MRC) fund manager Guy Anderson who sees the firm as ‘a long-term compounder’ for his investment trust portfolio.

He says Auto Trader is ‘clearly a category killer and a market leader by a significant margin’.

Providing an online market place for car retailing, Auto Trader is ‘focused on used car transactions, has excellent pricing power, very high operating margins and generates a lot of cash it can return to shareholders,’ adds Anderson.

Investors need to keep a close eye on its average revenue per retailer and whether this metric comes under pressure in the wake of the more competitive environment.

Close Brothers (CBG) £15.29

Merchant bank Close Brothers is often perceived as a good barometer of the health of the UK economy thanks to its lending to small businesses. Something of an all-rounder, the company has operations across lending, deposit taking, wealth management and securities trading.

Wesley McCoy, fund manager of Standard Life Investments UK Equity Unconstrained (B79X967) flags the company as a good one among UK shares.

He says: ‘The business specialises in taking the right risk at the right time. It sailed through the last crisis and has already shrunk lending in the hottest unsecure areas. This leaves it poised to perform strongly when others give up. Exactly the kind of long-term positioning that can stand the test of a rockier political and economic climate. The market thinks short term, Close thinks longer.’

The shares trade on 11.1 times forecast earnings for the year to July 2019.

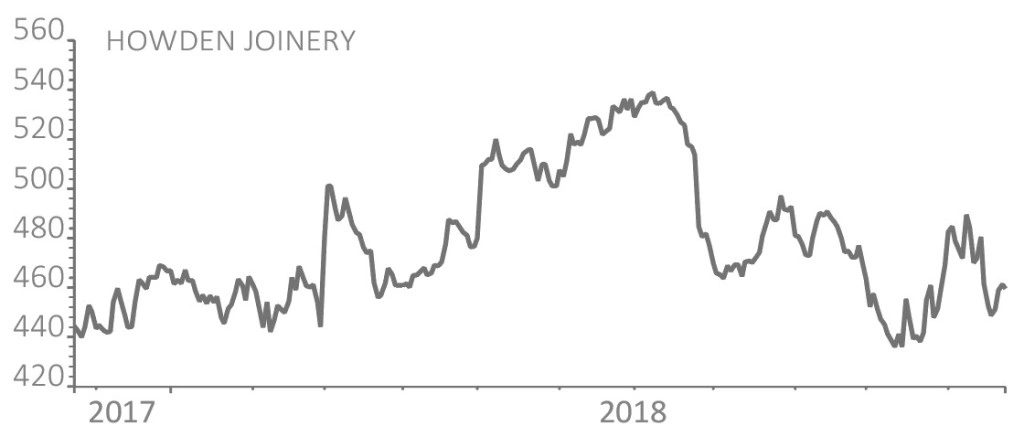

Howden Joinery (HWDN) 471.2p

There are 27m homes in the UK and with today’s busy lifestyles few of us have the time or skills to install a kitchen ourselves. When the time comes to upgrade, we employ a skilled fitter and that’s where Howden Joinery enters the equation.

Howden sells directly to the building trade rather than retail customers. Last year it sold over 4m kitchen cabinets, 2m million internal doors and 650,000 sinks and taps, making it one of country’s leading kitchen and joinery suppliers. The business has over 650 depots in the UK and almost half a million customer accounts.

Steve Davies from Jupiter UK Growth Fund likes Howden, saying it is generating strong like-for-like sales growth in a flat market and boasts high returns on capital.

First-half sales were up 7.5% (6.1% on a like-for-like basis) while investment in new stores and new product lines held operating profits back to a 4.5% rise.

The business is seen generating £245m of earnings before interest and tax this year on capital employed of less than twice that amount. In other words its return on capital employed is over 50%. On that basis the current rating of 14 times forecast earnings seems cheap.

Total returns (share price gains and dividends reinvested) over the last 10 years are 2,980% compared with 170% for the FTSE 100 index. That means an average compound annual share price increase of 40%, yet year-to-date the shares are flat.

M&C Saatchi (SAA:AIM) 310p

Advertising business M&C Saatchi is a heritage name in the sector but has branched out from traditional advertising to areas like customer relationship management and mobile advertising.

The business laid the foundations for its current earnings growth with a big investment phase in the wake of its 2004 IPO, opening up new offices in new geographies. Earnings per share advanced 17% in 2017 and are expected to grow a further 16% in 2018.

First half results this year beat expectations. In September, stockbroker N+1 Singer noted that the second half momentum looked promising ‘with enough client wins and mandates to achieve the full year and more’. The broker said the only reason it did not upgrade forecasts significantly was UK macro-economic uncertainty and caution over Brexit.

The company is not as heavily focused on consumer goods firms as some of its peers and the stock appeals to Aviva Investors’ head of UK equities Trevor Green on its current price-to-earnings ratio of 12.6-times.

Merlin Entertainments (MERL) 349p

Trevor Green, head of UK equities at Aviva Investors, flags Merlin as being an attractive stock in the current market.

Merlin runs theme parks and attractions in different parts of the world including the hugely popular Legoland sites. The company is expanding its hotel capacity with the hope of encouraging customers to spend more than one day at its sites per visit.

Its shares took a big hit in October when a trading update spooked the market with news of cost pressures, particularly tighter labour markets and the National Living Wage in the UK. That suggests near-term risks to profit margins.

The shares were also weak in the days leading up to the trading update because of negative read-across from a rival. Theme park operator Parques Reunidos issued a profit warning in early October which led some investors to worry about the state of the industry.

Share price weakness is therefore understandable in the wake of these negative issues. As such, anyone interested in buying the shares would need to take a much longer-term view and be comfortable with volatile periods for the share price.

Stockbroker Numis predicts Merlin will report £277.4m pre-tax profit for 2018 (2017: £271m). It then forecasts earnings growth will accelerate in 2019 to £291.3m.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.