Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy equities are hoping corporates stay in credit

One of the many arresting features of the 2007-09 financial crisis and resulting equity bear market was how stock markets were laid waste by problems in US housing and the bond markets.

In other words, those investors who had heavy equity exposure were blindsided by a downturn in different asset classes which looked entirely unrelated – until it turned out that they were not unrelated at all and a downturn in US housing roiled bonds, drained banks and markets of liquidity and all boats sank together (just as the rising tide of cheap money had lifted them all higher).

Investors who are heavily exposed to equities may need to look beyond more obvious candidates – such as tariffs, trade wars, Brexit, Italy or rising interest rates – when stress-testing their portfolios, as one year ends and another comes on to the horizon.

And if there is to be a surprise coming out of left field, perhaps it is the bond markets which could deliver a nasty blow, at least if recent price and yield action is any guide. Rising interest rates and tighter monetary policy (especially in the US) could therefore exert a powerful influence, but they could do so via the fixed-income market, at least initially, if current trends continue.

SPREAD THINLY

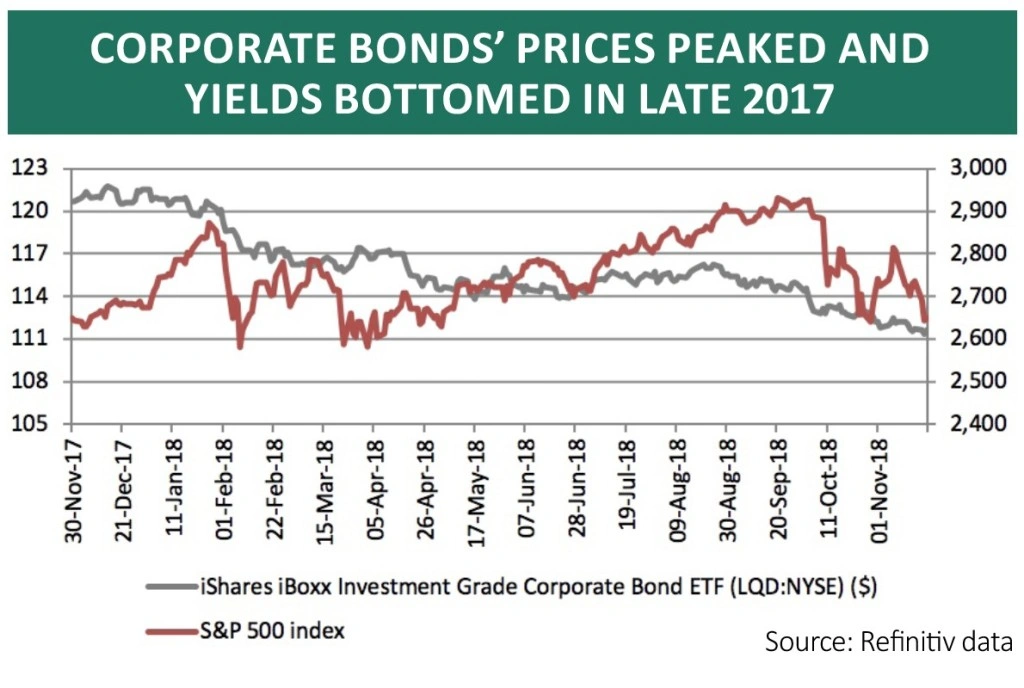

Thankfully that is still a matter of ‘if’ rather than ‘when’ but the seemingly inexorable slide in the price of the New York-listed exchange-traded fund iShares iBoxx Investment Grade Bond ETF must be followed closely for two reasons.

First, this instrument, which trades under the ticker of LQD, peaked last December and has since lost 8% of its value. That might not sound a lot but it is when the yield bottomed at 3.21% when the price peaked, because the capital losses have eaten up a lot of income already.

As investors know only too well, bond prices and yields move inversely, so when prices rise, then yields fall and vice-versa.

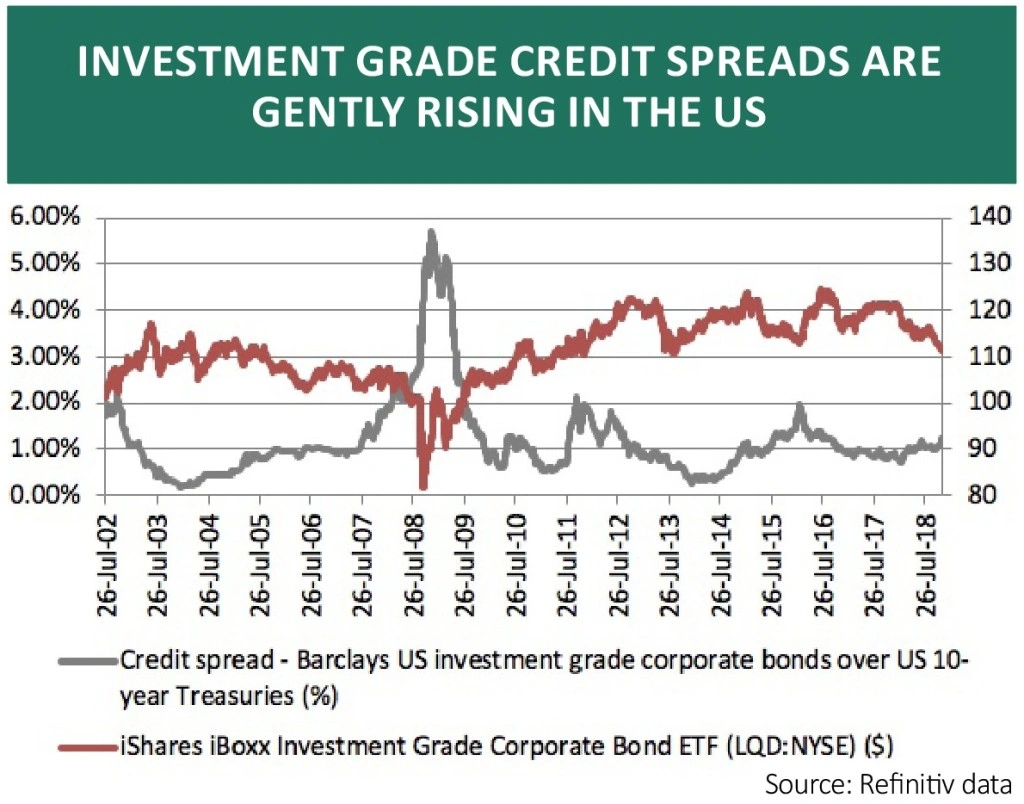

Yields are now rising and so – even more pertinently – are credit spreads. At the time of writing, the aggregate yield available from the members of the basket of bonds that makes up the LQD ETF is 4.33%. That compares to 3.07% from US 10-year Treasuries so the premium yield – or spread – is 1.26%.

That compares to the lows of barely 0.25% in early 2016, as the US Federal Reserve slowly embarked upon its mission to ‘normalise’ monetary policy and this year’s 0.72% low-point in January, as bonds and stocks basked in the perceived benefits of US president Donald Trump’s tax cuts.

This gradual widening of the credit spread reflects Fed policy, and particularly the faster pace at which the central bank is withdrawing quantitative easing. It may also reflect how US corporations have borrowed freely, enthused by record-low interest rates and cheap money.

Research this summer from S&P Global revealed that US corporate debt has risen from $3.6trn to $6.3trn in the past five years alone.

The good news is US firms have $2.1trn in cash on their balance sheets. The bad is that most of this liquidity sits with barely 25 firms. Strip those out and many investment-grade borrowers have a similar cash-to-debt ratio as ‘junk’, high-yield rated bond issuers, at around 21%.

That statistic may explain why more than 40% of the total value of US corporate bonds were rated BBB for the first time ever this summer, according to S&P Global’s research. Credit quality is slipping.

BACKBUY BLUES

Bond investors are paying attention because they are demanding higher coupons to compensate themselves for the risk, and a higher premium relative to Treasuries even as their yields rise.

Equity market participants are paying attention too. Thankfully, spreads are moving higher at a slow pace. But investors will need little reminding that a sudden spike in credit spreads has been a harbinger of increased equity volatility, and even some nasty falls, on at least six occasions in the last 20 years.

In addition, one equity strategy which had previously worked very well has started to encounter trouble, namely encouraging companies to carry out share buybacks.

The US-listed Invesco Buyback Achievers ETF peaked in January and its UK-listed counterpart Invesco Global Buyback Achievers ETF (BUYB) did the same and has since fallen by 13%.

This is not to say that all share buybacks are bad. In theory companies with so much cash on their balance sheet that they can afford to give it back should be a good thing.

But many of these companies have been using cheap debt to fund the buybacks and as debt gets more expensive that may look less smart,

from the perspective of the holders of both the bonds and the equity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.