Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow much cash is the right amount for your portfolio?

Rising cash levels are a hot topic at the moment – from conversations among investors in the pub and on internet message boards, to well-respected professional investors amassing more cash than usual.

The bouts of volatility in stock markets in recent months have caused some to panic and claim that we should cash out to avoid market falls. Warren Buffett, the renowned investor, has even built up record levels of cash in the investment company he runs, Berkshire Hathaway.

But with inflation running at higher than the majority of savings accounts will pay in interest, any move to cash means taking a real term cut in the spending power of your money – it’s not a free option. So how much cash is the right amount to have?

STEP 1: YOUR EMERGENCY POT

Any investor should have a cash pot that they can access immediately to use as a buffer in an emergency. This could be a bout of ill health or losing your job, for example.

The rule of thumb for emergency cash is between three and six months’ expenditure – that’s to cover your essential outgoings, rather than matching six months of income.

Whether you save three months or six months of costs into this pot depends on your own circumstances. For example, if you’re a two income family and can afford much of your essential outgoings should one of you lose your job, you may err on the lower end of this scale.

STEP 2: HOLIDAY, NEW CAR, BUYING A YACHT?

Next you need to work out the big purchases you’re going to make in the next five years that you can’t afford from your usual income.

What you include in this pot depends on your own preferences, your surplus income each month to be able to afford extra luxuries out of normal income, and your attitude to risk.

Included in this pot might be any holidays you plan on taking, a new car that you know you might need to buy in the next few years, offspring going to university that you’re helping to pay for, or a deposit for a home that you plan to buy in the next few years.

STEP 3: ASSESS YOUR TRUE CASH LEVEL

Setting your emergency pot and your short-term savings aside, you then want to determine how much cash you want in your investment pot. Before doing this you need to work out the true cash level in your portfolio. Many base this purely on the 5% or 10% of their portfolio they have sitting in cash – but the level is likely to be much higher.

Many fund managers will sit on large levels of cash at any point in time – either in the very short term, because they have sold something and are waiting for a new investment opportunity, or strategically, as they are waiting for market falls and have set aside cash to spend. It’s the latter figure you need to look out for.

This is particularly the case at the moment. Marcus Brookes, who runs the multi-manager funds at fund house Schroders, has been bearish on markets for some time and currently has almost 24% in cash.

Other examples include the Marlborough Defensive fund, which has more than 21% of its assets in cash, while the SVS Church House Deep Value Investment Fund (B79XM02) has almost 24% in cash or cash equivalents (cash equivalents usually means Government bonds that have a very short time until they mature). Stewart Investors Worldwide Equity (B4KJBJ0) fund has just over 18% in cash.

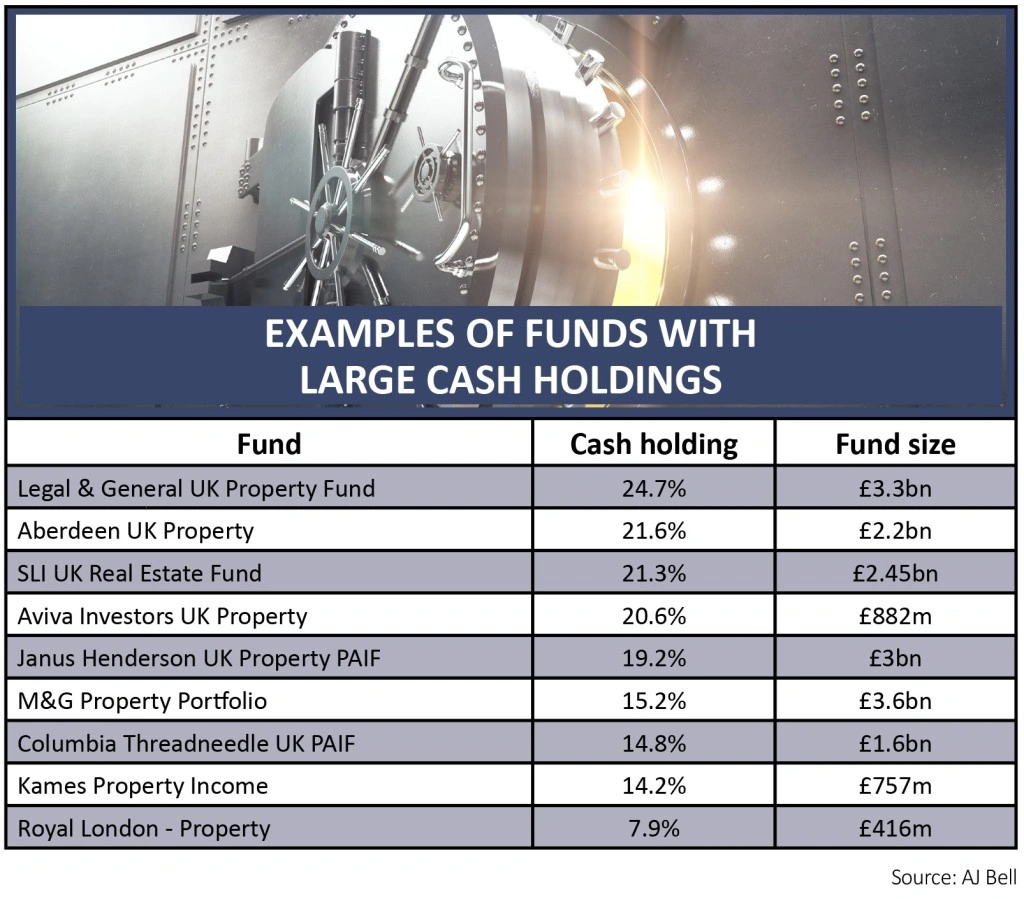

Property funds in particular usually have high levels of cash holdings. This is because property is an inherently illiquid asset, taking a long time to sell, and so property funds need to hold a decent level of cash in order to meet any requests for redemptions from investors.

The effects of this situation were seen just after the Brexit referendum in 2016, when fears about the UK property market led many investors to sell their property fund holdings.

In turn, many property funds ran out of ‘liquid assets’ or cash to meet these sell requests, and so ended up shutting the funds to redemptions. As a result, some have increased their cash levels in the wake of the panic, in order to help buffer against the same thing happening again.

The £3.3bn L&G UK Property (BK35DTI) fund has among the highest cash holdings of the property funds, with almost a quarter of the fund in cash, but the accompanying table shows the cash levels of these funds.

So when you think you have £10,000 invested in the markets in a property fund, you may actually only have £8,000, or in some cases £7,500, invested in bricks and mortar.

You need to do the forensic look-through into your funds to determine the true level of cash. Most funds will publish this cash figure on their factsheets, although some don’t make it obvious or use more complicated language.

STEP 4: WHY DO YOU WANT TO HOLD CASH?

The level of cash you want in your investment portfolio depends on three questions:

Are you nervous of market falls and want to build a bit more safety in your portfolio? This is an understandable reason to hold cash, and can help limit your losses if a market fall was to happen – but make sure you know why you’re holding it and what you’re waiting for.

Is everything a bit expensive? If you’re struggling to find investments that you want to buy at current prices then you might want to keep some cash for the short time to buy at a later date. The benefit of this and the above point is that should markets fall you’ll have a ready pot of money available to buy the dips.

Are you reaching a crucial, costly stage in your life? Many people will want to amass a bigger cash buffer if they are embarking on a more expensive stage of their life or where they will become reliant on their investments.

An obvious example is if you’re nearing retirement and want to ensure you have a certain level of income set aside and safe. Other examples might be if you’re setting up your own business or taking a career break and won’t have a reliable source of income for a while.

STEP 5: GET THE CASH FROM SMART PLACES

If you’re planning to sell assets to generate cash for any of these reasons, then get it from the right place. Use this as an opportunity to rebalance your portfolio, to ensure it’s sticking to your original asset allocation.

This usually means selling some of the funds that have performed well and reinvesting that money back into the ones that have underperformed. But if you want to generate cash you should be selling those outperformers and keeping the cash from there, rather than indiscriminately selling from any old fund.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.