Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe stocks and sectors affected by the Budget

Chancellor Philip Hammond’s last Budget before Brexit is being sold in some quarters as the biggest giveaway from the Treasury since 2010.

The financial market response to Hammond’s apparent spending splurge was modest, perhaps reflecting a view this could all be subject to change in the event of a no-deal Brexit.

Arguably the door was left open for this potential situation by the announcement that the Spring statement could be upgraded to a ‘full fiscal event’ if necessary – in effect an emergency Budget.

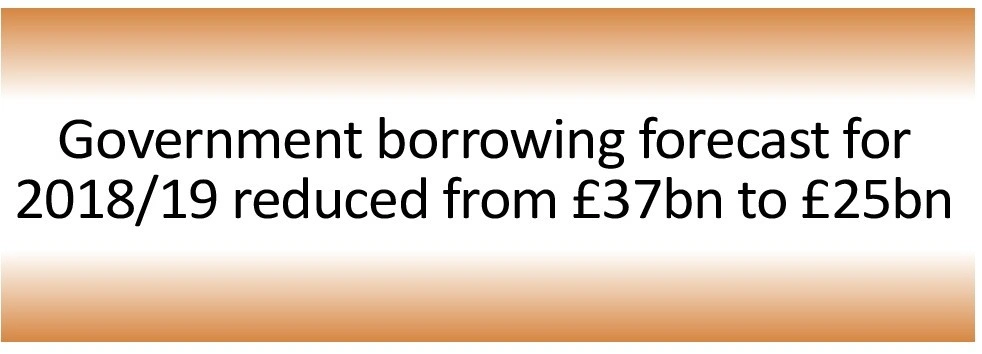

Official growth figures were slightly upgraded for the years ahead but still look skinny compared with pre-financial crisis levels. However, borrowing forecasts do show a substantially improved picture thanks to stronger than expected tax revenue.

On a sector-specific view there were some important new details for investors to chew over.

RETAIL AND LEISURE

In a potential boost to consumer spending the individual personal allowance will rise from £11,850 to £12,500 from next April, a year earlier than previously scheduled. Similarly, the threshold for higher-rate income tax will rise to £50,000 as of next April.

The increase in fuel duty has also been frozen for another year, saving car drivers an estimated £1,000 and van drivers an estimated £2,500 since the duty was frozen.

There was also a range of initiatives designed to help the UK embattled bricks-and-mortar retailers such as Debenhams (DEB) and Marks & Spencer (MKS).

In line with leaked figures there will be a £675m Future High Streets Fund to underwrite strategies to re-invigorate the traditional retailers and to finance the actual physical infrastructure including local transport.

The aim is to increase footfall on the high street which has fallen continuously over the last couple of years according to analysis from the British Retail Consortium, BDO and Springboard.

This initiative is coupled with a digital sales tax aimed at global retail platforms which in the Chancellor’s words ‘create value in the UK’ but aren’t paying their share of taxes.

The tax is projected to raise £275m in its first year, starting in April 2020, rising to £400m per year by 2023-24.

The Budget report confirms the affected industries as ‘search engines, social media platforms and online marketplaces’ – or Google, Facebook and Amazon in other words.

Pub operators should be pleased that duty on beer and spirits is being frozen. They should also benefit from news that the Government is looking to reduce ‘unnecessary red tape’ and lower the cost of wedding venues. Reports suggests this means making it easier to holding weddings in pubs, hotels and restaurants.

Remote gaming duty will increase from 15% to 21% to compensate for the loss of tax revenue from fixed odds betting terminals where stakes are being cut to £2. That is less severe than the 25% rate some people had feared, and some gambling stocks managed modest rallies in relief on 30 October as shareholders digested the news.

OUTSOURCING, CONSTRUCTION, INFRASTRUCTURE AND HOUSEBUILDING

A pledge to abandon the use of PFI contracts was arguably an easy one to make as there were none in the offing. The share prices of outsourcing groups Capita (CPI), Serco (SRP) and G4S (GFS) seemed largely unaffected by an end to austerity which theoretically implies there could be more work available from the public sector.

A boost in infrastructure spending on areas like roads and rail had been leaked in advance and had already given a lift to shares in construction-linked firms like Balfour Beatty (BBY), Costain (COST) and CRH (CRH) ahead of the Budget.

Kier (KIE) kept rising after the Budget thanks to its exposure to spending on broadband and its role as a key partner to local authorities across the UK with pothole repairs – where an extra £420m was earmarked.

Kier also has a housebuilding division so like peers such as Barratt Developments (BDEV) and Persimmon (PSN) there may have been some relief at the two-year extension of the Help to Buy scheme out to 2023. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.