Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEmerging markets: toxic or great opportunity?

Emerging markets haven’t been good to investors in 2018. Their meltdown has reflected a mounting trade war between the world’s two biggest economies, America and China, higher US interest rates and a strengthening of the dollar. Compounding the situation have been the currency crises and economic problems that have befallen Turkey and Argentina.

However, where there is a problem, there can be an opportunity. Prices and valuations in emerging markets are at rock-bottom levels, which makes them interesting for investors who can stomach ongoing volatility and whom already have a solid portfolio to cushion any blows should this part of the investment universe continue to have issues.

In this article we delve into the issues facing emerging markets and highlight two funds which we believe are the best ways to play this theme for those willing to take the plunge. Our top choices are MI Somerset Emerging Markets Dividend Growth (B4Q0711) and investment trust Templeton Emerging Markets (TEM).

THE BULL AND BEAR CASE

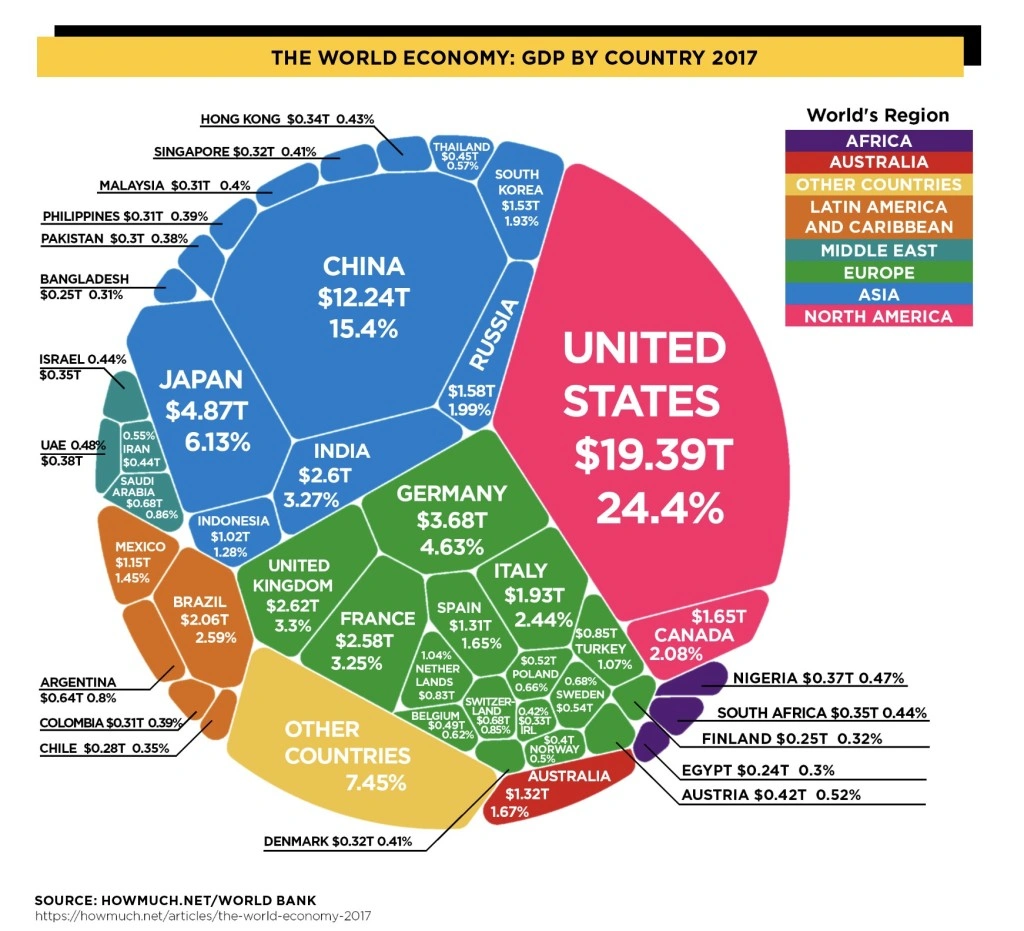

The term ‘emerging markets’ is used to describe the globe’s developing economies. They include some of the most populous nations including China, India, Brazil and Russia, as well as other countries including Mexico, Saudi Arabia and South Africa.

These rapidly growing regions are key contributors to global growth and could be the leading economic powerhouses of tomorrow. As such, they cannot be overlooked by serious-minded growth investors.

Although they are diverse, they typically exhibit attractive demographics and a burgeoning middle class, which are spearheading their economic growth.

Political and economic reforms in emerging markets have helped build stronger and more stable economies, with some constituents having lower debt and larger reserves. Far more companies in these regions now pay dividends to shareholders, meaning emerging markets are attractive for income seekers too.

When emerging markets are going gangbusters, bulls champion their rapid GDP growth, burgeoning middle class populations and the inexorable rise of the consumer classes.

Yet emerging markets in freefall provide fodder for the bears, who rubbish them as un-investable basket cases, with many constituents suffering weak currencies and onerous debt piles.

Equity valuations in this part of the investment universe are currently looking attractive relative to long-term averages, as emerging markets have had a torrid 2018. Bulls argue the fundamentals remain compelling.

WHY HAVE EMERGING MARKETS SOLD OFF?

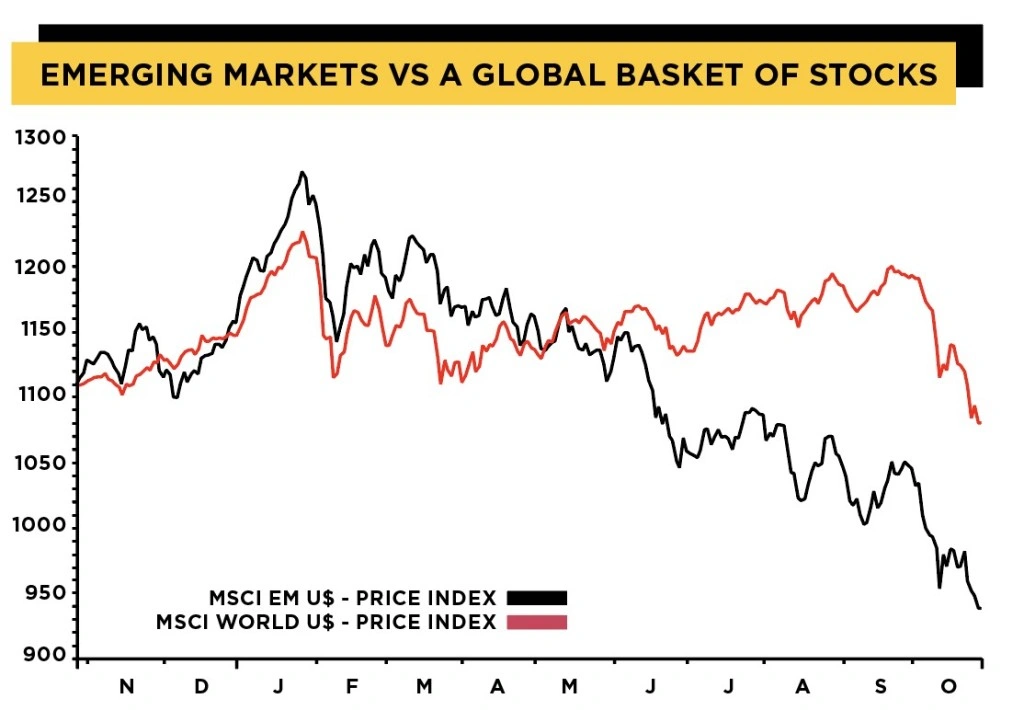

It is fair to say that 2016 and 2017 were superb years for emerging markets, with the MSCI Emerging Markets index rocketing higher and emerging market currencies surging north too. Indeed, the MSCI Emerging Currency index reached its strongest level on record versus the US dollar at the beginning of this year.

Sadly rising interest rates in the US plus the escalation in trade tensions have now led to risk-off sentiment towards emerging markets.

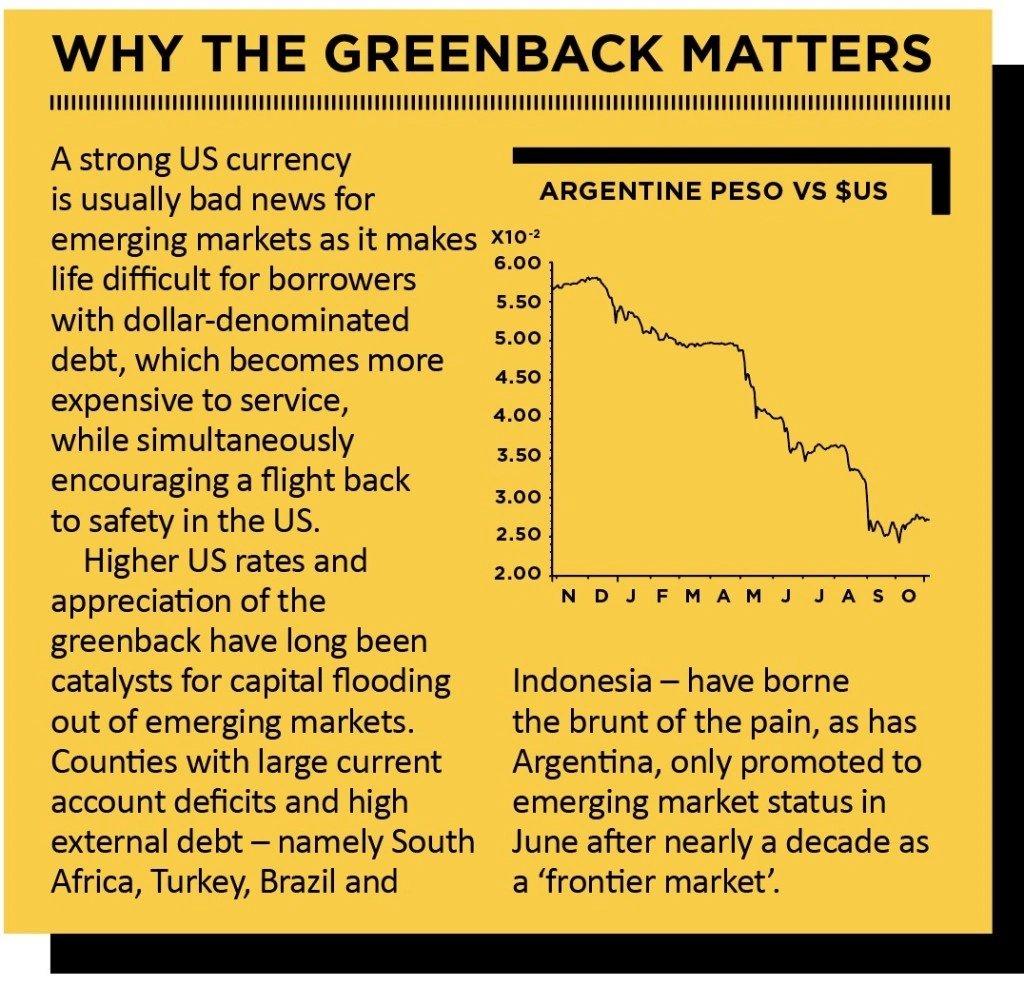

The tide began to turn with the prospect of rising US interest rates and a strong US dollar driving currency crises in Argentina, Turkey and South Africa, not to mention Indonesia, where the rupiah plunged in part due to the country’s widening current account deficit.

Contagion has swept through emerging market currency, bond and stock markets in 2018, leaving many to fear the emerging markets bubble has burst.

Chinese shares are in bear market territory, with growth in the Peoples’ Republic slowing. Soft guidance from several high-profile US companies with China exposure has also heightened concerns over the US-China spat, threatening to morph into a full-blown trade war.

As if all this weren’t enough, Latin American countries have been rocked by economic and political tumult. A series of adverse events have weighed on sentiment towards Latin American leviathan Brazil, where voters have been to the polls to decide a controversial presidential election which has hobbled this vast nation’s economic momentum.

DOES MISPRICING PRESENT AN OPPORTUNITY?

Significantly, the skittishness surrounding Turkey and

subsequent elevated worries over the China slowdown and Sino-US trade war have been extrapolated by the market across a broad, highly diverse emerging markets universe of more than 70 countries.

This is one key reason why emerging markets bulls argue these markets are mispriced, and the sell-off presents a not-to-be-missed attractive entry point for risk-tolerant investors.

They argue the Asian baby was thrown out with the Turkish bathwater in 2018, a stronger dollar, weaker commodity prices and Istanbul’s foreign borrowing woes weighing indiscriminately on all emerging markets.

Tellingly, long-term China sceptic Austin Forey, a fund manager at JPMorgan Emerging Markets Investment Trust (JMG), has become a bull.

‘Historically, Forey was cautious about China due to the high levels of non-performing loans in the country’s banks which he felt could result in a financial crisis,’ notes investment bank Stifel. ‘Having spent significant time in the country, he has now reconsidered his views.

‘He is enthused about the level of entrepreneurial activity in the economy and how companies are leveraging technology. He is particularly positive about businesses in the service sector, where some are earning high returns on capital,’ adds Stifel.

Meanwhile, Bloomberg has reported (21 Oct) that India’s top hedge fund has stopped hoarding cash and started buying shares again in anticipation of a bounce in the populous South Asian nation’s stock market.

The Avendus Capital Alternate Strategies’ Absolute Return Fund is increasing investments after benchmark indices slumped due to surging oil prices, higher borrowing costs and defaults at a local shadow lender. Andrew Holland, CEO at Avendus, is quoted as saying ‘we have turned the most bullish in at least the past six months’.

WHAT ARE THE RISKS AND POTENTIAL REWARDS?

The earnings risk associated with trade wars, depreciating currencies and rising bond yields are reasons the risk-averse might choose to sit on the side lines for now. There has always been something to worry about with emerging markets, where volatility is par for the course.

Weakened currencies make it more difficult for emerging markets firms to keep up with hard currency interest payments but they also offer more attractive prices for overseas investors.

However, it is also worth bearing in mind that not all emerging markets are equally vulnerable to the dollar. Many have overhauled their economies and reduced their foreign debt piles, and as such, would argue they’ve been unfairly caught up in the sell-off.

Omar Negyal, portfolio manager of JP Morgan Global Emerging Markets Income Trust (JEMI), insists: ‘Despite recent volatility in emerging markets, valuations are currently neutral which partly reflects an overall improvement in fundamentals following a challenging few years for emerging market economies and companies.

‘On a multi-year view we think profitability for the asset class has the potential to rise further from here. This should, ultimately, help to drive up dividends and share prices.’

Negyal continues: ‘We have a positive outlook about the long-term prospects for dividend generation. While movements in sterling may impact on the value of dividend payments, the above average quality of the companies and superior profitability of the portfolio versus the market remains high and consistent.’

He adds: ‘In the near term we’re mindful that uncertainty prevails, given the impact of rising bond yields and the risk of “trade wars” which have paused the improving earnings momentum of emerging markets companies.

‘However, we remain focused on investing in sound businesses, run by strong management, with good prospects that have the potential to deliver income and growth.’

Edward Lam, who manages the MI Somerset Emerging Markets Dividend Growth fund alongside Edward Robertson, cautions ‘we are in the middle rather than the end of a correction’. Yet he concurs that ‘the situation on the ground is actually better than people might expect in certain emerging markets’.

THE GODFATHER OF EM INVESTING

Carlos Hardenberg, one of the trio of founders of Mobius Capital Partners, who manages the recently launched Mobius Investment Trust (MMIT) alongside the ‘godfather’ of emerging markets investing Mark Mobius and Greg Konieczny, insists now is the time to revisit this pare of the investment universe. Populations and living standards have ballooned, creating enormous middle classes with growing consumption levels.

As he opines on the Mobius Capital Partners website: ‘Governance has improved significantly, with shareholder engagement and activism not just supported but actively encouraged by companies and governments alike. Most crucially, emerging markets now offer a dramatically more attractive set of companies. These businesses and management teams no longer follow – they lead.’

Hardenberg also explains that both private and public debt levels in most emerging markets are far lower than in past debt-driven crises. This mitigates concerns about the rising cost of hard currency interest payments.

‘Even in the case of companies with high levels of debt, active investors can carefully run through individual company balance sheets and talk to management to identify firms that are able to protect themselves,’ he thunders.

‘In China, technology “unicorns” are being born with increasing frequency, without ever leaving the domestic market.

‘In Indonesia, entire sectors (such as banking) remain undeveloped, offering numerous multi-billion-dollar markets to tap into for

South East Asian companies that can combine cultural and domain expertise.

‘These sorts of domestic and regional growth opportunities, regardless of what happens in developed markets, offer resilience at a time when many are concerned about fallout from the ongoing trade war.’

HAVE MARKETS OVER-REACTED?

Chetan Sehgal, lead portfolio manager of the pioneering Templeton Emerging Markets, says emerging markets have faced ‘a perfect storm’ year-to-date, referring to higher rates and weaker currencies.

Yet Sehgal is keen to stress the strength of the balance sheets of many firms in his investable universe. ‘The typical corporate in emerging markets is not on a borrowing spree. Stocks have sold off on expectations of a far worse outcome than the reality is.’

In terms of turning the tide of negative sentiment, any resolution of the US/China trade war would be an obvious catalyst, to his mind. ‘We are hoping that they come to a compromise,’ says Sehgal.‘And if China was to make a large investment in physical infrastructure in the US that would help.’

Medha Samant, investment director at Fidelity Asian Values (FAS), says the key short-term risk for investors is trade wars and their impact on supply chains in Asia, principally China, but also Korea and Taiwan.

‘Trade protectionism is never good in the long term and investors are worried about the earnings side,’ concedes the analyst.

Managed by Nitin Bajaj, Fidelity Asian Values seeks to achieve long term capital growth through investments in the Asian region excluding Japan. Samant explains that ‘most of the correction is

being seen in the cyclical names. Large cap names have held up better than small and mid-cap, and the selling has been in the low quality, cyclical names.’

Across the emerging markets universe, Samant says ‘a lot of the opportunities are coming from China’ – Bajaj has added China Mobile to the portfolio – ‘and we’ve found some really good quality names in Indonesia.

‘India has been a source of funding for some of these names,’ she explains, noting that the South Asian powerhouse being ‘less impacted by trade wars and benefiting from domestic investor support’.

Fidelity Asian Values continues to have high conviction in India’s HDFC Bank, ‘an all-weather stock that is best in class, taking share from the traditional lenders and has a good growth profile’, and has also been buying a water utility in the Philippines, namely Manila Water.

WAYS TO GAIN EXPOSURE

Before even considering emerging markets, investors should already boast a well-diversified portfolio and make sure they wade into

these choppy waters with their eyes wide open, in the expectation of further volatility.

There are numerous funds offering exposure to this part of the investment universe. Examples include Hermes Global Emerging Markets (B3DJ5K9), Baillie Gifford Emerging Markets (0602064), Neptune Emerging Markets (B8J6SV1) and Invesco Global Emerging Markets (BDJ0CC7).

Emerging markets funds may offer broad exposure to the full range of countries or they may specialise in just a few countries. It is important to do thorough research and fully understand each fund’s investment focus and process before you hand over any money.

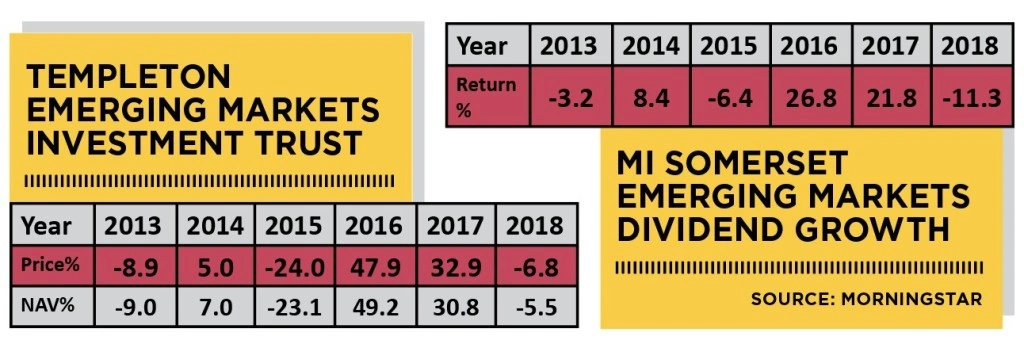

OUR CHOICE OF FUNDS

We like the MI Somerset Emerging Markets Dividend Growth fund. It has a concentrated portfolio of around 40 quality conviction ideas and invests in companies which demonstrate prospects for long-term cash flow and dividend growth.

Leading portfolio positions include SK Hynix, a lately unloved, Korea-based dynamic random access memory (DRAM) producer and seller; Samsung Electronics; Brazil-based car insurer Porto Seguro; and Coca Cola HBC (CCH), the emerging markets-focused coke bottling behemoth with opportunities in markets ranging from Russia to Nigeria.

Speaking to Shares, fund manager Edward Lam highlights a deliberate underweight to China, reflecting a lack of single stock ideas as well as his concerns over the Chinese banking sector. That said, a relatively new holding for the fund is Chinese oil producer CNOOC, a beneficiary of higher oil prices whose production growth and cost efficiency initiatives are back on track under new management.

MI Somerset Emerging Markets Dividend Growth has also been making some in-roads into the domestic Indian market. ‘We’ve been adding to India on the sell-off, somewhat opportunistically,’ explains Lam, who has put money to work with Maruti Suzuki, the motor car maker and ‘great franchise’ which has been increasing market share and deepening its competitive position.

For those preferring to own investment trusts, the average discount to net asset value in the AIC’s Global Emerging Markets sector stands at 10.7% compared with an average discount of 3.6% for all UK investment trusts.

It is quite normal for emerging markets-focused trusts to trade at a wider discount because underlying holdings are often considered higher risk and potentially more illiquid versus stocks from developed markets.

Examples of single country investment trusts that fall under the emerging markets banner include India Capital Growth Fund (IGC); VinaCapital Vietnam Opportunity Fund (VOF); Fidelity China Special Situations (FCSS); and BlackRock Latin American Investment Trust (BRLA).

Broader trusts with greater country-level diversification included the newly-launched Mobius Investment Trust and Fundsmith Emerging Equities Trust (FEET).

‘STABLE MANAGEMENT TEAM’

Investment bank Stifel views JPMorgan Emerging Markets

as the best trust through which to gain exposure to the theme.

‘It is the only generalist emerging markets trust that we cover that has had a stable management team in recent years,’ says its investment trust research team.

‘The manager, Austin Forey, has led the trust for over 20 years and proved his ability to deliver good levels of outperformance. The portfolio is comprised of quality growth companies, many of which are global in nature and operate outside of the areas impacted by the trade wars.’

We see upside potential at Templeton Emerging Markets, whose 11% share price discount to NAV might entice value investors.

Fund manager Chetan Sehgal seeks long-term capital appreciation through investment in companies listed in, or deriving a significant chunk of their revenues from, emerging markets.

As at 30 September, the investment trust’s top 10 holdings include South Korean electronics giant Samsung Electronics, best known for its Galaxy smartphones and flash TVs; Cape Town headquartered internet-to-entertainment giant Naspers; and BMW car seller Brilliance China Automotive. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.