Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvest with the best: why Brunner is a must-have fund

There are three reasons why Brunner Investment Trust (BUT) deserves a place in your portfolio.

First, it has an experienced management team in Lucy Macdonald, chief investment officer of global equities at Allianz Global Investors (AGI), and Matthew Tillett, UK portfolio manager at AGI.

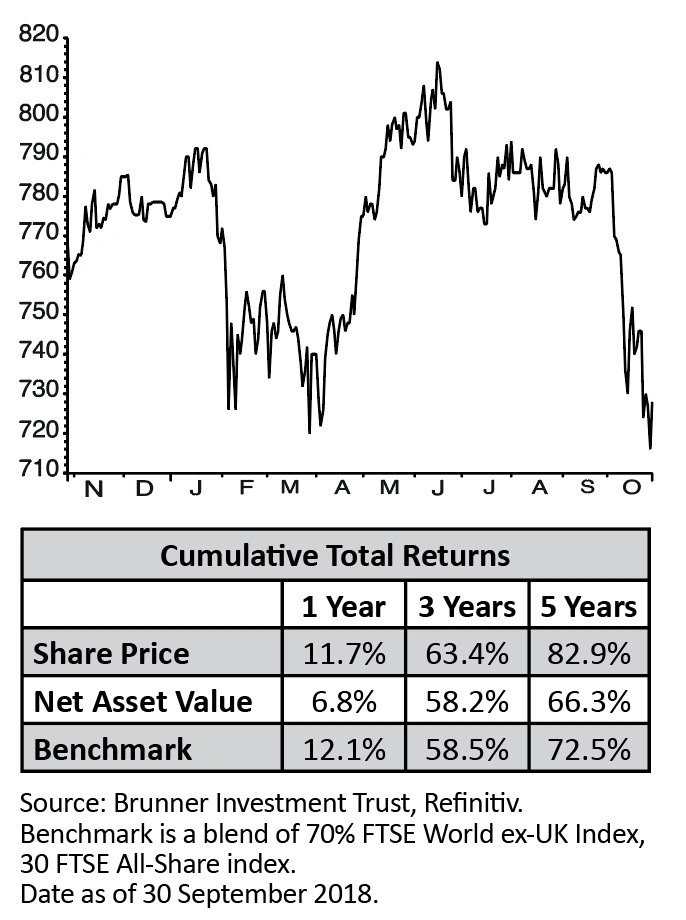

The trust’s brief is to provide a mix of growth in capital value and dividends by investing in global and UK securities, and thanks to the team’s stock-picking skills shares in the trust have beaten their benchmark consistently over three and five years.

Second, the trust’s ability to invest globally has been boosted by changing to a 70/30 split between global and UK stocks instead of the historic 50/50 split.

The list of holdings is fairly concentrated with fewer than 70 stocks at the end of September. The trust holds some UK heavyweights for dividend growth such as BP (BP.), GlaxoSmithKline (GSK) and Royal Dutch Shell (RDSB).

Consistent with its aim the tilt is more towards growth with holdings in global technology stocks such as Apple, Microsoft and Taiwan Semiconductor, and financial stocks such as Visa.

A great example of the selling discipline is Chinese internet sensation Tencent. After a huge run in the shares from 2012 the trust began reducing its stake last summer on concerns over valuation.

Now that the Chinese authorities are regulating gaming and online media companies more heavily, concerns have spread to Tencent’s growth prospects as well as its valuation and the shares have erased much of their gains.

The third attraction is the recent change in Brunner’s capital structure which not only lowers the trust’s funding costs but also underpins future dividend payments.

Over the summer it issued £25m of debt at a fixed rate of 2.84% for 30 years and repaid its outstanding debentures which carried an interest rate of 9.25%.

This will improve the trust’s returns because it doesn’t have the ‘drag’ of paying out a high rate of interest on old debt. It also means that reserves per share are higher so there is more scope for dividend growth.

It’s worth flagging that as well as having one of the highest yields in the sector at 2.3%, Brunner has the distinction of having raised its dividend consecutively for 46 years. (IC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.