Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShould you buy Aston Martin now its shares have fallen 26% since IPO?

The news is full of talk about the UK’s car manufacturing industry as the Brexit deadline looms ever larger, but there is only one car maker whose shares you can buy on the London stock market.

British marque Aston Martin Lagonda (AML) was worth £4.3bn when its shares starting trading at the start of October at £19.00. That valuation, towards the lower end of its initial range, was still seen as toppy by many City analysts, but the shares have got a lot cheaper since, falling to £14.01. That’s a significantly greater decline than the FTSE 100 during its latest sell-off.

You might not be able to afford one of its prestige motors (they cost about £150,000 on average) but is the investment opportunity now at an appealing price for investors?

SECOND CENTURY PLAN

To answer that question we must first understand Aston Martin’s future plans and chequered past (it has gone bust seven times in its 105 year history). The company’s Second Century Plan concentrates on bringing stability to the business, making it a more robust model, and expanding the product portfolio.

Performance since 2013 shows decent success on the first measure, and it is now facing up to the second and third challenges. Having delivered 5,098 new cars in 2017, getting more models on the road is vital. It wants to push production to 14,000 by 2022 with a line of SUVs set to join its more traditional sports cars from next year.

It is even embracing the switch to electric with the Valkyrie hybrid model (albeit it with a £2.4m price tag), part of its limited line making a handful of supercars for the super-rich.

Aston Martin’s biggest market at the moment is still the UK, accounting for a third of sales, followed by the rest of the EU (25%), Asia-Pacific (24%) and the US with 20%. Surprisingly only about 6% of sales go to China, an obvious target to improve given its population, emerging high net worth market and economic growth.

Aston Martin plans to open 10 new and refurbished showrooms out there in the months ahead.

WHAT IS PRICE-TO-EARNINGS TELLING US?

Aston Martin’s stock is trading on a current year price-to-earnings (PE) multiple of 48.3, based on consensus forecasts to 31 December 2018. That falls to 25-times in 2019, but rises again to 29.2-times in 2020 due to hefty investment plans. These metrics are based on average annual growth in revenue and operating profit of 25% and 36% respectively over the next two years.

By contrast, Ferrari, the New York-listed luxury sports cars maker (widely perceived as Aston Martin’s closest peer) trades on a 2019 PE of 27.8-times, based on its current $113.96 share price.

Some investors may think these PEs imply Aston Martin is decent value, others may think differently. We tend to believe that the real valuation story lies beyond earnings largely because of the big investment required to fuel its growth ambitions. Let’s now take a look at cash flow.

IF CASH IS KING, IS ASTON WEARING NEW CLOTHES?

On the face of it, sales volumes, selling prices and unit production have all been improving in recent years, a point reflected in Aston Martin’s gross margin. It has gone from 32% in 2015 to 37% in 2016 and 43% last year. That’s helped Aston Martin turn its first pre-tax profit in 2017 after five years of red ink.

While net cash from operations has gone from £75.2m to £343.8m over the past three years, the company has also had to plough enormous sums back into the business, almost entirely wiping out free cash flow.

Modest £3.2m of free cash flow invites the question of how the company could make a pre-tax profit last year. The answer comes down to how it treats research and development (R&D).

All car makers need to invest in R&D to keep their vehicles up to date with rapid changes in technology, but at the higher end – where Aston Martin pitches its motors – this is even more important. And the company has always been quite aggressive in its policies on capitalising R&D spend.

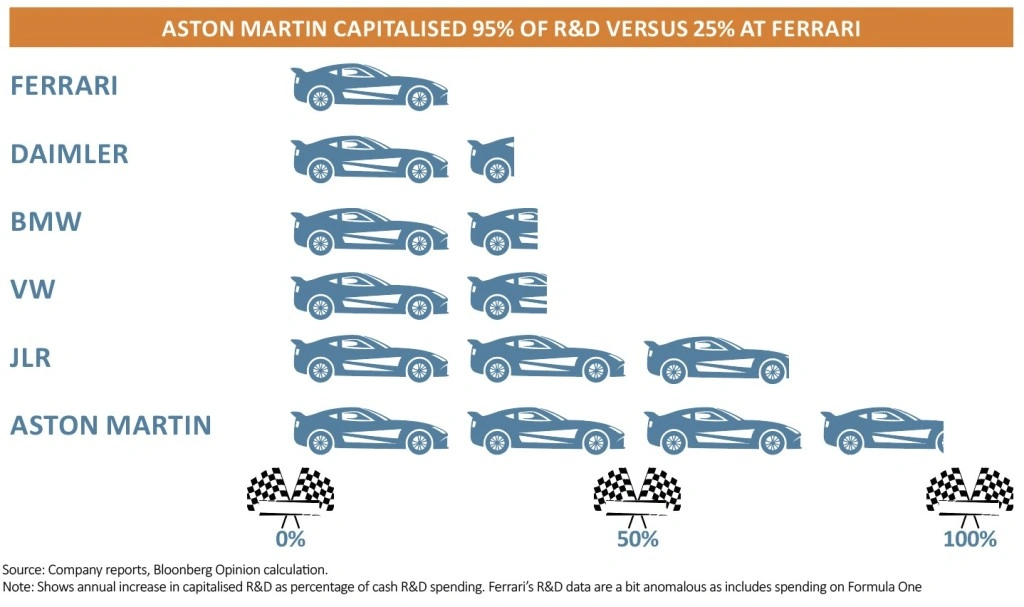

CONTROVERSIAL R&D TREATMENT

Capitalising expenses means investment is recorded as a future asset on the balance sheet rather than a cost on the profit and loss statement. Companies are allowed to do this when they can demonstrate a clear benefit down the line. That’s not always possible and there are rules around what can and cannot be ‘expensed’.

Aston Martin has always been fairly aggressive in this regard although within the rules. Company accounts show that between 2015 and 2017 it spent £484.2m on R&D, capitalising £451.7m, or about 93%. First half results for 2018 show the same ballpark (92%) figure on £95.2m of R&D.

This is not unusual for technology-led companies who are investing today for income tomorrow. When Apple wants to design the next iPhone, for example, some of that cost will be expensed, but it will earn revenue on those new iPhones in the future.

Without getting too bogged down in the arguments for and against capitalising R&D, the rules allow room to manoeuvre. But many traditional and conservative investors think this is sharp practise because it is not always easy to work out what your investment will earn you in future.

This puts Aston Martin at the more aggressive end of the spectrum compared to peers, according to research by analysts at investment bank Canaccord, and far more so than Ferrari.

The effect on Aston Martin’s profit is marked. Canaccord’s analysts calculate the company generated adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) of £207m in 2017.

Factor in the £213.2m of expensed R&D and the company’s operating profit is completely wiped out, which tallies more closely with underlying free cash flow.

With significant investment needed to meet its growth ambitions (new model designs and machinery upgrades across several production sites), investors might conclude that extra funding will be

needed. Missing growth targets would also be an obvious blow.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.