Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineG4S back in the news for the wrong reasons but positives remain

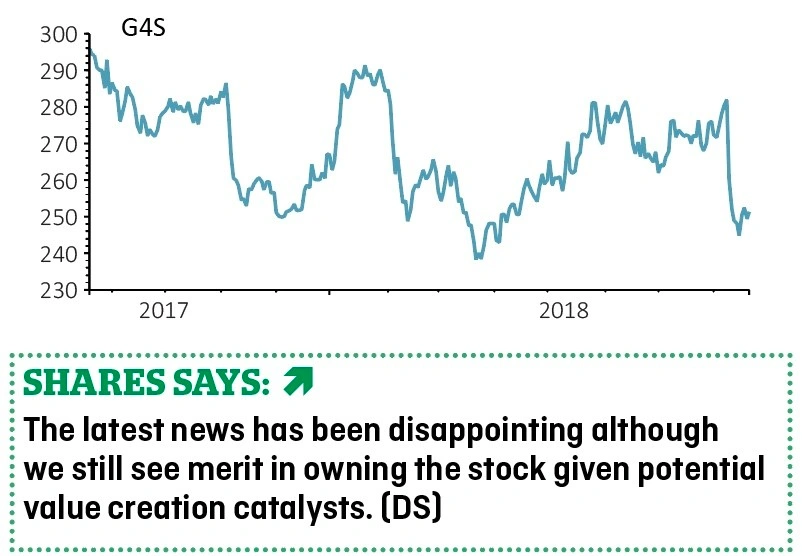

G4S (GFS) 251p

Loss to date: 2%

Original entry point: Buy at 256.2p, 16 November 2017

Security services company G4S (GFS) has had a torrid time in recent weeks. The Government has assumed control of Birmingham Prison from the company after a report revealing major widespread failings.

Prison inspectors said the prison had fallen into a ‘state of crisis’, with the chief inspector of prisons, Peter Clark, describing it as the worse prison he had ever seen.

This followed results released on 9 August which showed a company whose pre-tax profit had declined by 3.2% to £212m while operating cash flow fell 2.2% to £179m on a year-on-year basis.

However, we still remain positive on the company as it can sell off its Cash Solutions business which would plug its pension deficit and give the company more options.

Kean Marden, analyst at investment bank Jefferies, says selling the business would lead to around £2bn in surplus capital to ‘deploy on technology acquisitions’.

Jefferies is not the only voice that sees the potential for G4S from making disposals; fellow investment bank UBS has been saying this for some time. Back in January it was suggesting that the company could either dispose of its Cash Solutions business or alternatively demerge it and list it separately.

The shares trade on 11.3 times 2019 forecast earnings per share of 22.24p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Hill & Smith directors take advantage of profit warning-led share weakness to snap up stock

- Investors shift focus to defensive stocks

- Pressure on corporate brokers implies potential wave of M&A

- Trump attacks the US Federal Reserve

- London hoteliers set to report bumper numbers following July heatwave