Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow have Lifetime Isa investors fared in their first year?

It’s a year since AJ Bell launched its version of the Lifetime ISA, a few months after the newest form of the ISA was launched in April 2017.

Since then around 8,000 individuals have signed up to the YouInvest Lifetime ISA, one of the few investment platforms that allows unrestricted investment within the ISA. See the box (overleaf) for the basics of the Lifetime ISA account and how it works.

But how have investors fared in that first year?

FIRST YEAR CHECK

Of the top 100 investments made by AJ Bell Lifetime ISA customers in their first year 48% are passive funds – either tracking one index or multi-asset funds using passives. AJ Bell’s in-house passive funds take many of the top spots, as do Vanguard’s ever-popular range of LifeStrategy multi-asset funds.

Lifetime ISA investors opting for funds spread their risk by plumping for global stock market funds, rather than placing their bets on one region. Of the top 10 funds, half have a global focus. The only exception to this is Japanese funds, which make up three of the top 10 funds, in addition to Jupiter Asian Income (BZ2YMTY) fund, which invests in Asian companies excluding Japan.

Investment trusts make up just 12% of the top 100 list, with investors preferring to use funds over trusts. Where Lifetime ISA investors have picked trusts, they have broadly opted for trusts with proven track records that have been running for decades, as popular trusts include Scottish Mortgage (SMT), Finsbury Growth & Income (FGT) and City of London (CTY).

The only anomaly is Woodford Patient Capital (WPCT), which only launched in 2015 and made the list of most bought trusts, despite its share price plummeting by 20% in the past year.

A portfolio evenly split between the top 10 investments would have returned £793 in the past year, on the maximum £4,000 annual Lifetime ISA contribution plus the £1,000 Government bonus. That’s significantly ahead of the £305 return you’d have got from investing in the FTSE 100 over the past year and also ahead of the £615 return from the MSCI All World index.

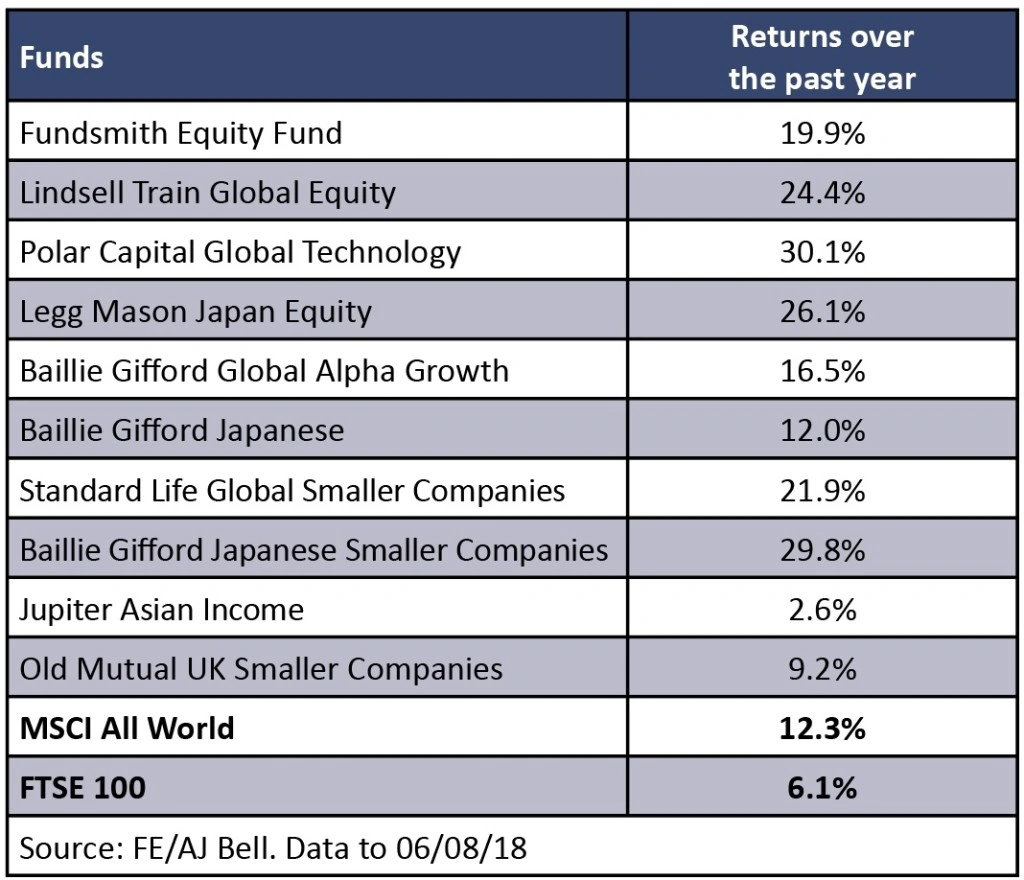

THE FUNDS

Lifetime ISA customers have been savvy when it comes to picking funds, with all but one exceeding the returns from the FTSE 100 over the past year.

Perennially popular names such as Terry Smith’s Fundsmith Equity (B41YBW7) and Nick Train’s Lindsell Train Global Equity (B3NS4D2) made the top 10 list, as investors look for managers who have proven their worth over decades.

Investors’ focus on Japan as a region has paid off over the past year, with Baillie Gifford Japanese Smaller Companies (0601492) returning almost 30% and Legg Mason Japan Equity (3350746) returning 26%, while Baillie Gifford Japanese handed investors a 12% return.

Jason Pidcock’s Jupiter Asian Income fund has fared less well, and is the worst performer of the top 10 funds, delivering just 2.6% over the year. However, one year is not a long time period to invest nor judge the performance of a fund.

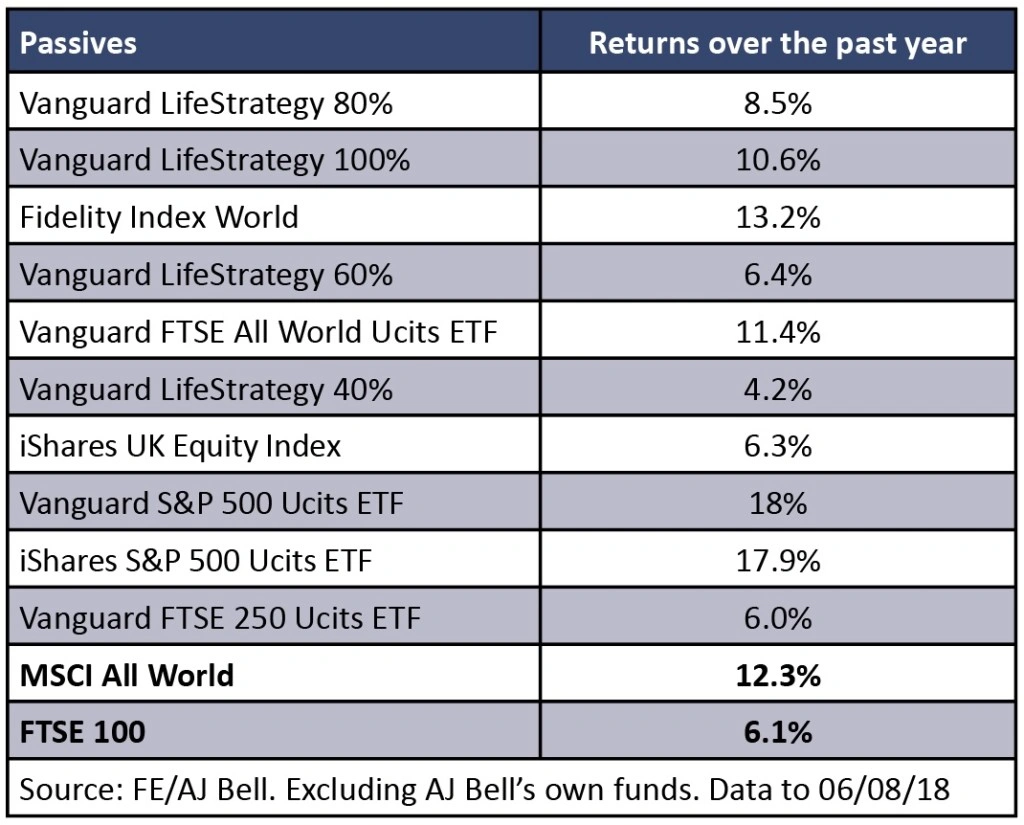

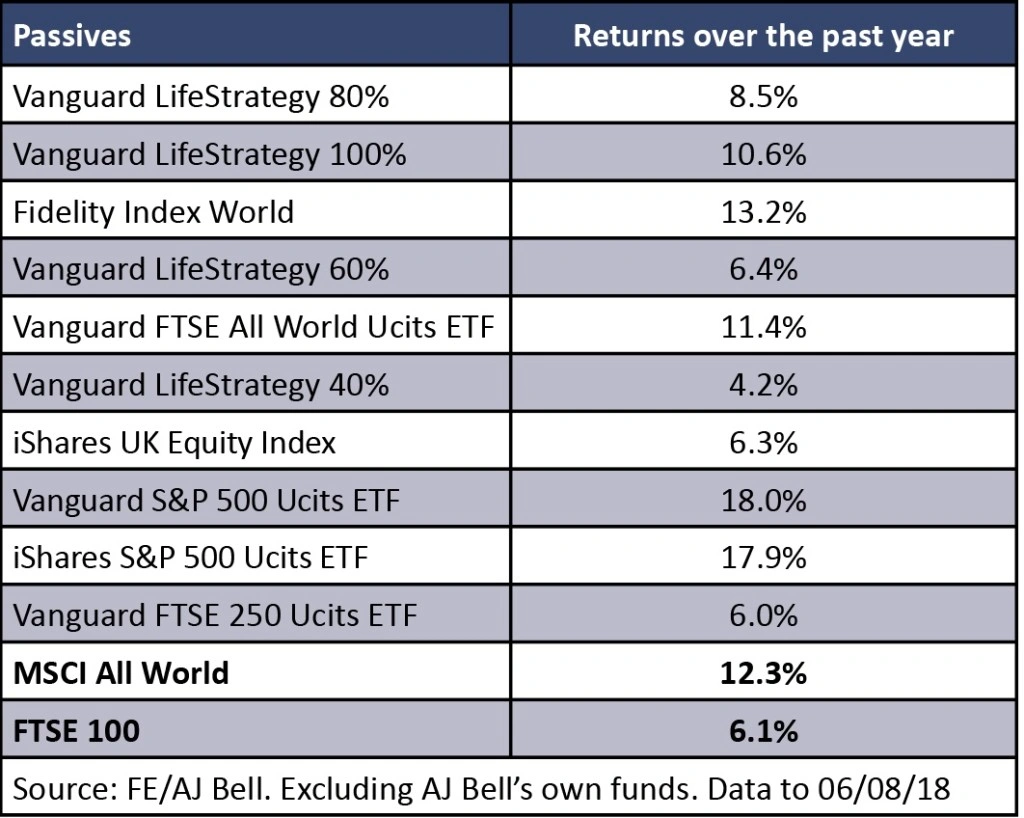

THE PASSIVES

Lifetime ISA investors will often be investing for the first time, so it makes sense that the Vanguard LifeStrategy range of low-cost multi-asset funds feature heavily in the top 10 list.

These funds are intended as a one-stop-shop and take the decisions about how much money to allocate to different regions and sectors out of investors’ hands. They invest in a range of underlying passive funds, spreading the investments across different asset classes. The funds differ in how much they have allocated to the stock market, with the funds with the higher allocations proving most popular for Lifetime ISA customers.

The popularity of these funds, as well as AJ Bell’s similar in-house funds, is also likely a result of the fact that Lifetime ISA investors will not have large wealth amassed in these accounts yet.

Elsewhere, investors focused on developed markets, opting for trackers of the main UK and US indices, or of global markets. For those getting into investing for the first time, tracker funds can be an easy-to-understand entry point to help them build confidence with markets. They also present a low-cost option for investors conscious of the amount fees will eat into their ultimate returns.

THE INVESTMENT TRUSTS

Investment trusts only represent a small proportion of Lifetime ISA’s portfolios. This is a trend we see across many investors, who plump for funds over trusts, but is also understandable as first-time investors may find investment trusts harder to understand.

Among the 12 trust selections two have failed to match the returns of the FTSE 100 index over the past year. Neil Woodford’s Woodford Patient Capital Trust woes have been well documented, with shares in the trust falling in value by more than 20% over the past year, thanks to several underperforming investments in this early-stage investing fund.

City of London trust, run by Job Curtis at Janus Henderson, also disappointed over the past 12 months, delivering a 4% return in a year where the FTSE 100 returned 6.1%.

However, stellar performance has been delivered by the trusts focusing more on technology companies, such as Allianz Technology (ATT) and Baillie Gifford-run Scottish Mortgage, delivering 48.9% and 30% respectively. Meanwhile, Edinburgh Worldwide (EWI), which is also run by Baillie Gifford and invests in early-stage companies, including a number of technology firms, has returned 44% in the year.

Laura Suter, personal finance analyst, AJ Bell

How does the

Lifetime ISA work?

Investors can use the Lifetime ISA to either save for a house deposit or for retirement. The money can only be used to buy your first home or at the age of 60 to help fund your retirement. Any withdrawals for any other reason, other than if you’re terminally ill, will incur a 25% exit charge.

Savers can put up to £4,000 into the Lifetime ISA each year, which is topped up by a 25% Government bonus - to a maximum of £1,000 each year.

If you are using it to buy a property, you must be a first-time buyer, the home must cost £450,000 or less and it must be for you to live in (so not a buy-to-let property).

To open a Lifetime ISA you must be between the ages of 18 and 40, and you can carry on paying into the ISA (and getting the Government bonus) until you reach 50. This means if you started at 18 and put the maximum away each year, you could amass around £400,000 by age 50, assuming 5% investment growth after fees. This would rise to almost £660,000 by the age of 60, assuming the same annual growth and no further contributions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Hill & Smith directors take advantage of profit warning-led share weakness to snap up stock

- Investors shift focus to defensive stocks

- Pressure on corporate brokers implies potential wave of M&A

- Trump attacks the US Federal Reserve

- London hoteliers set to report bumper numbers following July heatwave