Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

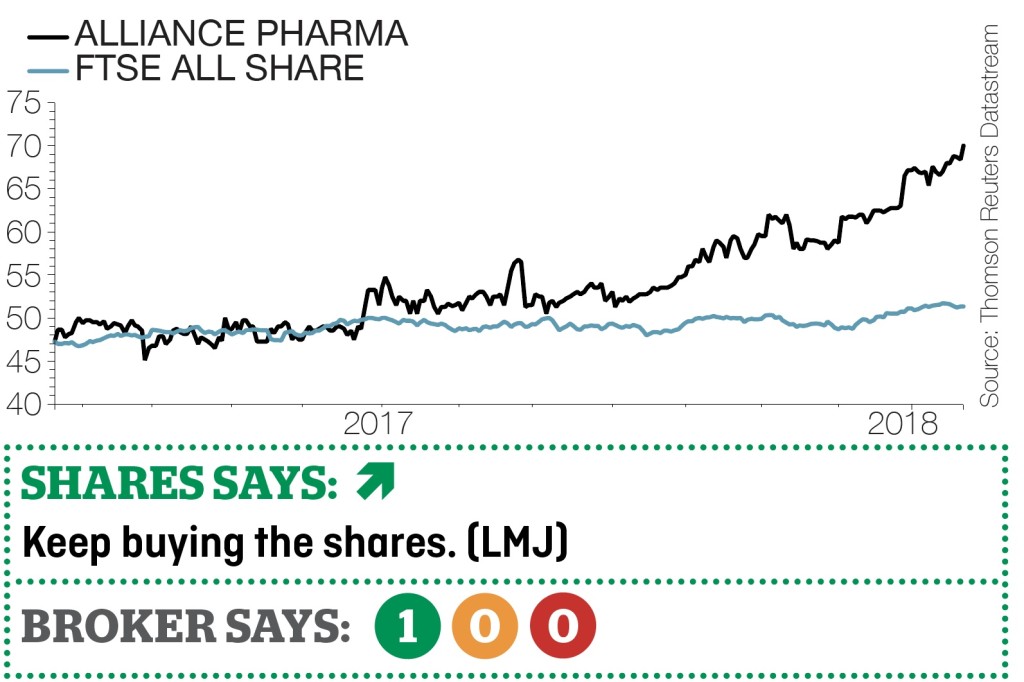

magazineWhy Alliance Pharma is in good health

Alliance Pharma (APH:AIM) 71p

Gain to date: 13.6%

Original entry point: Buy at 62.5p, 21 December 2017

Alliance Pharma (APH:AIM) has issued a reassuring trading statement, saying that full year revenue for 2017 will be 6% higher on the previous year at £103.3m.

Alliance Pharma is one of our top stock picks for 2018 as we like its growth potential, which is expected to be supported by targeted marketing and bolt-on acquisitions.

The company acquires and licences pharmaceutical and healthcare products to deliver to patients.

Sales of scar reduction product Kelo-Cote jumped 33% to £13.3m in 2017. Age-related macular degeneration treatment MacuShield sales rose 37% to £7.3m in the same period.

The weaker pound had a beneficial effect on revenue, but had less of an impact on operating profit due to higher costs, leaving 2017 pre-tax profit in line with expectations.

Cash generation increased significantly from £13m in 2016 to £21.5m in 2017, helping to drive debt lower.

Numis analyst Sally Taylor says the recent acquisition of Smith & Nephew’s (SN.) topical gel Ametop and worldwide rights of TyraTech’s (TYR:AIM) head lice treatment Vamousse should help lift sales by 11.5% in 2018.

The analyst forecasts continued double-digit sales growth momentum for Kelo-Cote, MacuShield and Vamousse in 2018.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- EMIS stung by after-care foul-up

- Draper backing for cryptocurrency start-up

- Market shock after Dignity unveils radical new pricing structure

- Top performing funds are harder to find

- US treasury yields hit highest level since 2014

- Bookies bashed on £2 betting stake cap reports

- Connect crashes on profit warning