Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

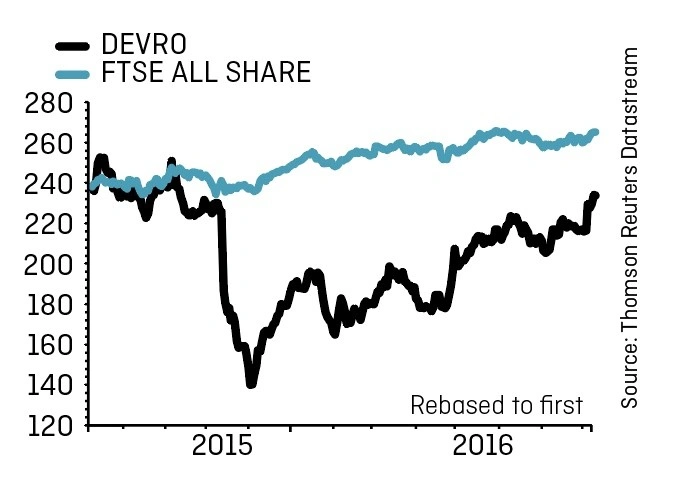

magazineDevro’s turnaround is looking tasty

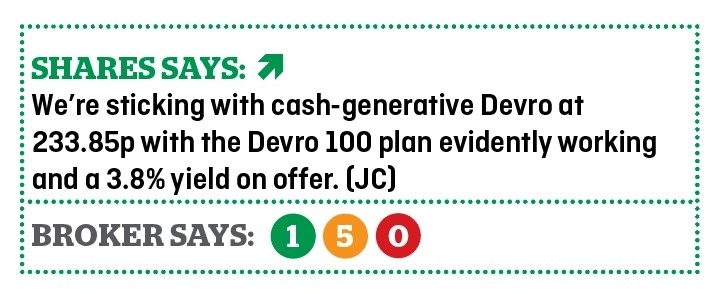

Devro (DVO) 233.85p

Gain to date: 41.3%

Original entry point: Buy at 165,5p, 22 December 2016

Sausage skin manufacturer Devro (DVO), one of our Top Ten for 2017 selections, has rewarded our faith with a tasty 41.3% gain. We’re staying positive on the food industry collagen products purveyor following encouraging half year results (2 Aug).

These revealed sales up 11% to £125.2m. The sales improvement reflected favourable currency moves and volume growth in China, where Devro’s new plant is building custom, South East Asia and Russia. While Devro is encountering pricing pressure in China, the country accounts for 40% of global collagen casings consumption and represents an exciting growth market.

CEO Peter Page also reported progress with the Devro 100 programme, running ahead of plan with £6m of cost savings expected this year, ahead of previous guidance of £3m-to-£4m. Page is confident about reducing Devro’s net debt levels over time – robust cash flows enabled Devro to hold the first half dividend at 2.7p - and is excited about a pipeline of new product launches.

Investec Securities’ Nicola Mallard has upgraded her price target from 236p to 278p. For calendar 2017, the analyst looks for improved adjusted pre-tax profit of £31.5m (2016: £31.2m) and a 9p dividend (2016: 8.8p), ahead of £38m and 9.2p in 2018.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.