Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow much capital should I sell in retirement?

For many years investors were advised to spend investment income in retirement and leave their capital untouched. But longer life expectancy and low interest rates mean this is no longer possible for many people.

In some instances, selling capital could be more advantageous than withdrawing money from dividend-yielding assets, particularly from a tax perspective.

The difficulty is figuring out how much capital you should sell so that you can fund a comfortable retirement without running out of money.

Why is the 4% rule no longer relevant?

In the 1990s a study in America suggested that withdrawing an annual income equivalent to 4% of your portfolio would ensure your money lasted throughout your retirement.

This theory has now been thrown out by many experts. Government figures show life expectancy at birth has increased by an average of 13.1 weeks a year for men and 9.5 weeks a year for women since 1980. Your retirement could last a lot longer than your parents’ and grandparents’, so your money also needs to last longer.

Another problem with the 4% rule is that in the 1990s US interest rates ranged between 3% and 7%. In the UK today, interest rates are at rock bottom which has reduced the yield available from cash and bonds. This has increased the demand for higher-yielding assets, which in turn has led to an increase in prices.

It is much harder to generate the level of investment return that was assumed by the 4% rule without taking on a lot more risk.

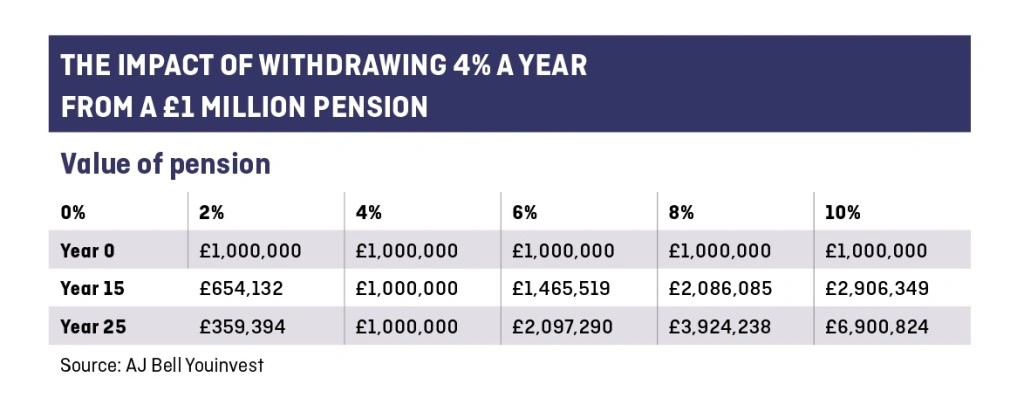

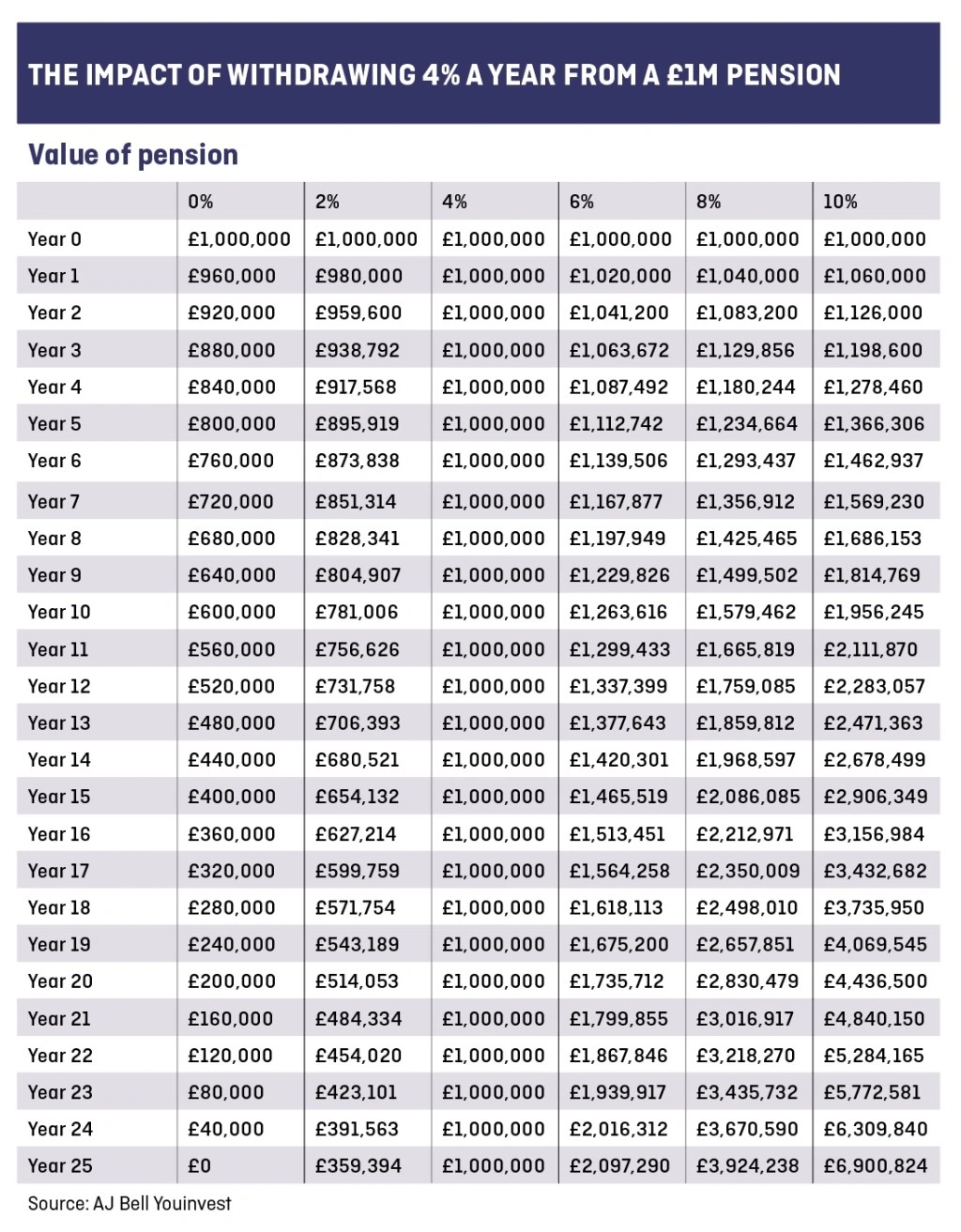

Figures from AJ Bell Youinvest show that if you had a £1m pension pot which only grew by 2% a year and you withdrew 4% each year, after 25 years it would be worth £359,394. If the annual return was 6%, the £1m pot would be worth just under £2.1m after 25 years. The figures assume a consistent annual return, which is somewhat unrealistic, but they give a rough idea.

Even if you think the 4% rule is good in theory, it is unlikely to be suitable for everyone.

In fact, Simon Andrews, a financial planner at financial advice firm 1825, says most people don’t want to be restricted to withdrawing a certain amount each year.

‘They want flexibility to use their money when they choose; maybe to pay for a child’s wedding, to put down a deposit on a property or to go on the trip of a lifetime. It will be different for everyone, and that’s why people need a personal plan,’ says Andrews.

The benefits of selling capital

A willingness to sell capital in retirement can provide flexibility. Even if you can generate enough income from dividends to cover your essential expenditure, there could be occasions when this is insufficient.

If you sell capital assets within a pension plan or ISA they won’t be subject to capital gains tax (CGT).

Outside of a pension or ISA, taxable capital can be a lot more efficient than taxable income. Income is taxed at 20% if you’re a basic rate taxpayer and 40% if you’re a higher rate taxpayer. CGT is 10% and 20% respectively.

Everyone is entitled to an annual CGT allowance of £11,300, regardless of your income tax band. It’s possible to carry forward reported capital losses from previous tax years to reduce your capital gain.

The biggest drawback of selling capital is if the investments have dropped in value you’ll end up crystallising your losses. It could be extremely difficult for your portfolio to recover.

High yielding investments

It may be possible to generate a sufficient income in retirement by investing in high-yielding stocks, rather than selling capital.

The challenge is to find these stocks. During times of low interest rates the increased demand for high-yielding stocks can make them expensive. There’s also a risk that they won’t stay high yielding forever.

David Thurlow, wealth management director at financial advice firm Mattioli Woods, says investors need to watch out for high yielders where the dividend is in jeopardy and be prepared to sell the capital.

On the flip side, if a yield is sustainable, then the high yielder could become a lower yielder purely by virtue of the share price rising. ‘Eventually, it makes sense to sell out of that share and reinvest in something else that will deliver a higher income. It’s a bit more work, but can reap high rewards,’ he says.

A downside of focusing on high-yielding stocks is you reduce your investment choice. Douglas Kearney, investment director at Intelligent Pensions, says many attractive investment opportunities are focused on growth and choose not to pay a dividend or income return.

‘The critical element is to avoid selling any component at a loss as that creates a huge hill for the portfolio to climb. Diversification within the portfolio should mitigate this risk significantly,’ he says.

Is there a new withdrawal ‘rule’?

Instead of having a hard and fast rule advisers suggest being flexible.

Simon Andrews of 1825 says one way of figuring out how much money you need is to look at your goals, rather than automatically resigning yourself to 20 or 30 years of 4% withdrawals.

Often people want to spend more at the start of their retirement when they’re likely to be more active. Spending may take a dip in mid-retirement when things start to slow down. In later life you may have increased outgoings if you need to pay for care.

‘The 4% rule doesn’t allow for this, and so doesn’t really stack up for real-life retirement,’ says Andrews.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.