Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMundane Marvels

A mistake investors frequently repeat is chasing in-vogue, go-go-growth shares and shunning the ‘steady eddies’ of the stock market.

It is easy to understand how electric car maker Tesla captures the imagination, even as it burns through cash, while online fashion retailers including Amazon and ASOS (ASC:AIM) may be disrupting industries and grabbing market share, but their gravity-defying ratings leave scant room for disappointment.

As a result, some of the London market’s marvellous, if more mundane, money-making stocks are often overlooked by analysts, fund managers and private investors alike.

However, investing is as much about keeping your money safe as it is making a return on it, which means the best long-term picks can often be the dull ones. Fundamentally sound companies, whose activities are less glamorous yet generate sustainable cash flows and profitable growth, are often shunned. We think that’s a mistake.

The stock market is home to what some may regard as ‘boring’ businesses whose compelling fundamentals and ability to compound earnings and dividends are simply not well-known to private investors. The good news is that investors prepared to go against the crowd and invest in less sexy areas of the market have a good chance to making decent money.

As legendary US investor John Neff once remarked: ‘Judgement singles out opportunities, fortitude enables you to live with this while the rest of the world scrambles in another direction….To us, ugly stocks were often beautiful.’

Mindful of the old adage that ‘where there’s muck, there’s brass’, Shares has sifted through the market to shine a light on companies whose activities may be dull but the returns they deliver delightful.

Most are predicated on the provision of essential services or everyday items that customers cannot do without whatever the economic backdrop.

Our picks may lack the investment excitement of a Blue Prism (PRSM:AIM), the robotic automation process tech designer, or of premium mixers brand marvel Fevertree Drinks (FEVR:AIM) or online fashion business Boohoo.com (BOO:AIM).

But we’re happy to highlight the loot generating potential of loo roll maker Accrol (ACRL:AIM), the dependable returns on offer via disposable gloves and cleaning products distributor Bunzl (BNZL) and reckon investors can clean up with textile rental play Johnson Service (JSG:AIM). We also flag the growth and income attractions of family-run flooring firm James Halstead (JHD:AIM).

Where there’s muck, there’s brass

Waste companies are often considered by many retail investors as being safe and reliable investments. After all, millions of people are consuming items and throwing away packaging, unwanted items or bits of food every single day.

Waste firms, you might imagine, have a steady stream of work and therefore generate lots of money. In reality, these types of businesses can experience volatile market conditions with unpredictable waste volumes. As such, you shouldn’t consider this to be a low risk sector.

London-listed waste companies range from bin collection group Biffa (BIFF) to hazardous waste expert Augean (AUG:AIM). The former looks to be the most interesting stock among the UK-quoted waste firms, in our opinion.

A better bet among the market’s boring but brilliant firms is FTSE 100 business supplies distributor Bunzl, which supplies the things other companies need in order to do business; everything from disposable coffee cups to food wrap for supermarkets as well as safety equipment and syringes for hospitals.

Another dull-but-worthy enterprise is Rentokil Initial (RTO), whose growth engine is the grimy area that is pest control; the removal of rodents, flying and crawling insects and snakes (in South Africa) isn’t work for the squeamish, but it is an essential service required by businesses and homeowners globally.

Elsewhere, we’d also highlight that the textiles specialist Berendsen (BRSN), a provider of laundry services for hotels and hospitals, is being taken over by French rival Elis for £2.17bn, a princely 44% premium to the share price before Elis lodged its bid.

This offers a positive read-across for UK rival Johnson Service, a workwear and linen provider whose resilience stems from its focus on renting essential clothing to hotels, restaurants and caterers.

Rentokil Initial

The Scottish Investment Trust’s view

Pest control, providing and laundering workwear and uniforms and providing feminine hygiene units and floor protection mats are rather grimy endeavours, yet they are also essential areas of spend customers can’t cut back on.

This is good news for investors in leading proponent Rentokil Initial, whose backers include The Scottish Investment Trust (SCIN), managed with a contrarian ethos by a team led by Alasdair McKinnon, whose thoughts on Rentokil we provide below:

What is it?

‘Rentokil Initial is a UK quoted provider of business services and residential support services including pest control services (56% of sales), hygiene products and services (25%) and workwear (19%).

Rentokil is the world number 1 in the, highly-fragmented, pest control market – though only number 3 in the US behind Terminix (ServiceMaster) and Rollins.’

Why is it unloved?

‘Historically, Rentokil grew with a succession of relatively scattergun acquisitions and endured a very difficult period which was characterised by a succession of new CEOs, profit warnings and asset disposals. Current CEO, Andy Ransom, took over after the previous incumbent failed to turn around the group’s fortunes.

The problematic City Link parcel delivery business was sold for just £1 before eventually going bust. Rentokil is still unfairly judged on its past challenges by backwards-looking investors.’

What’s changed?

‘Having disposed of non-core assets, the group is now focused on its core area of pest control. A growing, stable market which is driven by increasing regulation around the world and rising wealth as well as higher hygiene standards in emerging markets. Customers tend to be sticky as you are unlikely to risk changing your pest controller if they are doing their job.

Rentokil is consolidating the fragmented pest control market by acquiring smaller local competitors in attractive regions. This approach has significant operating leverage as customer density increases along existing service routes which in turn boosts margins; rising turnover and margins has a geared effect on profits.’

Potential takeover?

‘Despite the shares having rerated, the valuation (22x FY18 PE after today’s move) is at a significant discount to peers such as Rollins (44x FY18 PE). This could make the company an

attractive takeover candidate.’

Shares’

key boring-but-brilliant picks

Accrol (ACRL:AIM)

Share price: 138.5p | Market value: £130.7m

In terms of activities, the manufacture of toilet rolls, kitchen towels and industrial wipes is about as unglamorous as it comes, although this should not dissuade investors from putting money to work with cash generative Accrol (ACRL:AIM).

One of Shares’ running Great Ideas selections, the Lancashire-based business supplies customers including Booker (BOK), B&M European Value Retail (BME), Wilkinson, Aldi, Lidl and Tesco (TSCO) and is geared into the structural shifts towards the discounters and cheaper own-label products.

We like Accrol’s relatively capital light, flexible model. The £130.7m cap buys in 100% of its parent reels (paper) and doesn’t have any capital tied into paper mills, giving it the flexibility to take advantage of an over-supplied industry.

Results for the year to 30 April 2017 revealed a 58% surge in adjusted pre-tax profit to £13m on sales up 14.2% to £135.1m, with net debt reduced by £41.7m to £19m.

For the current financial, Liberum forecasts pre-tax profit of £14.6m for earnings of 12.5p (2017: 11.8p) and a hike in the dividend from 6p to 7.5p, leaving Accrol on a modest prospective price-to-earnings (PE) multiple of 11.1 implying re-rating scope, whilst offering a bumper prospective yield of 5.4%.

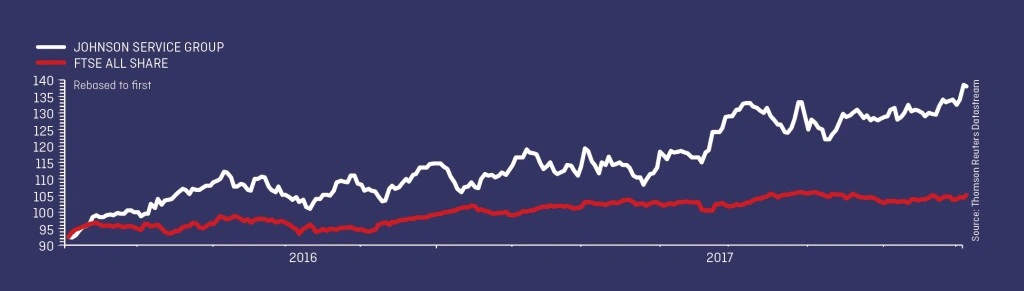

Johnson Service (JSG:AIM)

Share price: 138.25p | Market value: £507.6m

Textile rental may not quicken the pulse but Johnson Service (JSG:AIM) is wearing well as a dependable growth and income

pick and interim results (4 Sep) could spark further share price appreciation.

Having sold its lower margin Drycleaning business in January, Cheshire-headquartered Johnson is consolidating the higher margin, fragmented and resilient textile rental sub-sectors.

Already the UK’s leading workwear and protective wear supplier through its Apparelmaster brand, through its Stalbridge, London Linen, Bourne and Afonwen brands, the £507.6m cap also provides premium linen services for the hotel, catering and hospitality markets.

Johnson Service has a strong five-year track record of top-line, operating profit, earnings per share and dividend growth and is trading strongly. Chief executive Chris Sander remains focused on driving the cost benefits from last year’s successful acquisitions – Afonwen, Chester and Zip Textiles – and is now considering ‘further opportunities’.

Following an upbeat pre-close update (4 Jul), Investec Securities upgraded its full year earnings forecast by 2% to 8.1p, reiterating its ‘buy’ rating and 160p price target which implies 15.7% upside. For the current year to December, the broker forecasts improved normalised pre-tax profit £36.6m (2016: £33.8m), building to £37.4m and £39.3m in 2018 and 2019 respectively.

Reassuringly, this year’s forecast dividend payment of 2.7p (2016: 2.5p) is covered three times by forecast earnings of 8.1p

(2016: 7.6p).

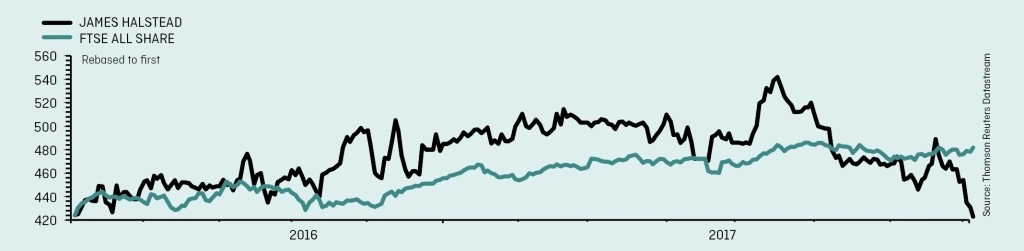

James Halstead (JHD:AIM)

Share price: 423.71p | Market value: £895.8m

Recent share price weakness offers a buying opportunity in Manchester-based commercial flooring products maker and distributor James Halstead (JHD:AIM), whose long sales, profit and dividend growth history puts most businesses to shame.

James Halstead’s total shareholder return from 1 January 2001 to 31 December 2016 is over 4,700%, which compares favourably to the FTSE All Share index (124%) and FTSE AIM All Share index (-31%).

The Halstead family continues to guide the £895.8m cap, Geoffrey Halstead in the chair and Mark Halstead ias chief executive. Admittedly commercial flooring isn’t an activity that’ll get the blood pumping but patient portfolio builders won’t mind as Halstead continues to grind out superb returns.

Despite a UK market slowdown and adverse price pressure on raw materials, Halstead is on course to once again report record turnover and profits for the year to June 2017 and will likely hike its dividend for the 41st consecutive year.

Despite this dependability, the business is anything but a dullard in terms of its customer mix and range; its wares are found everywhere from ‘Thalia’ book stores throughout Germany and the Freedom of the Seas, the world’s largest cruise ship, to the Machu Picchu Railway in Peru.

Halstead’s flooring is also in use at Scott Base in Antarctica and in the Svalbard Hotel on the edge of the Polar Icecap.

Tellingly, James Halstead, which has pedigree in paying special dividends, is a holding for the CFP SDL UK Buffettology Fund (GB00B3QQFJ66). Its well-followed manager Keith Ashworth-Lord backs strong operating franchises and experienced management teams. His other positions include the less-than-glamorous bonding materials specialist Scapa (SCPA:AIM) and industrial fastenings engineer Trifast (TRI).

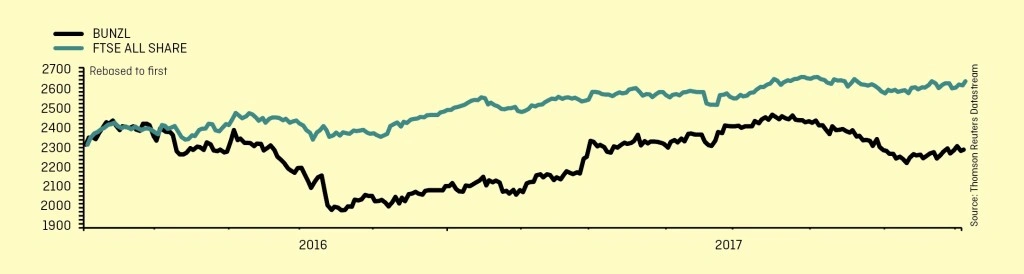

Bunzl (BNZL)

Share price: £22.91 | Market value: £7.67bn

For a company operating in the not too glamorous world of coffee cup and toilet paper supply, distribution and outsourcing group

Bunzl (BNZL) is actually a brilliant investment. It operates globally, offering essentials to hospitals, schools, offices and more including disposable gloves and cleaning products.

Bunzl supplements organic growth with bolt-on acquisitions – nothing too big, nothing too transformational or risky – then improves the performance of the purchases, leading to increased profitability and cash flow with all of the deals self-funded.

Bunzl is one of just 27 FTSE 100 firms to have increased its dividend for each of the last 10 years consecutively and its streak of increases in fact stretches back 24 years. Bunzl recently announced (27 Jun) that revenue is expected to increase by 7% in the six months to 30 June 2017, benefitting from improved underlying growth as well as a boost from acquisitions.

Recent bolt-on deals include two businesses in Canada, AMFAS and Western Safety, which together have annualised revenues of C$16m.

It has also bulked up its Spanish offering with the acquisition of Technopacking; made an offer for a group of businesses in France; and bought UK digital signage sector play Pixel Inspiration.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.