Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIs pension tax relief back under the microscope?

We don’t even know the date of the Chancellor’s first post-election Budget and already the knives are out for pension tax relief.

The Sunday Times’ political editor Tim Shipman reports early stage talks are being held by Treasury officials about ways to save money, with pension tax perks once again at the top of the agenda.

So how could Chancellor Philip Hammond look to reduce tax relief? And what can you do to protect your hard-earned savings?

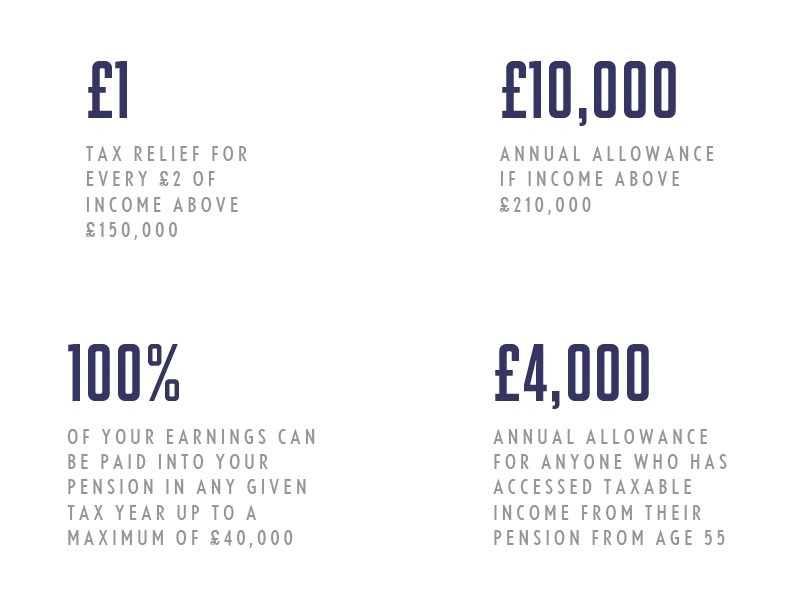

Recap: How tax relief works at the moment

The way pension tax relief operates for basic rate taxpayers (at the moment anyone earning below £45,000) is relatively straightforward.

For every £80 you pay into your SIPP, the Government will automatically top it up with £20 in tax relief. Put another way, your original £80 investment delivers a 25% return before you’ve even invested the money.

Tax relief will be added by your employer or pension provider without you having to do anything.

You can pay up to 100% of your earnings into your pension in any given tax year up to a maximum of £40,000. Those with no UK earnings can pay up to £3,600 into a pension inclusive of tax relief.

The annual allowance is much lower, being £4,000 for anyone who has accessed taxable income from their pension from age 55.

Because tax relief is granted at your marginal rate of income tax, higher and additional-rate taxpayers can claim an extra top-up through their self-assessment tax return.

Complexities for higher earners

Higher earners need to think about a few points. Firstly, there is the fiendishly complicated annual allowance ‘taper’. This reduces the amount you can pay into a pension and receive tax relief by £1 for every £2 of income above £150,000.

As a result, anyone with income above £210,000 has their annual allowance lowered to £10,000.

The final piece of the puzzle is the lifetime allowance, currently set at £1m. This restricts the amount of money you can have invested across all of your pensions. If you breach this limit you have two options – take it as a lump sum and be taxed at 55% or keep the excess in your fund and pay 25% tax on it.

It’s worth speaking to a regulated financial adviser if you’re unsure about how these limits might affect you.

How it could change

Here are some of the things that, in theory, the Government could do to reduce tax relief for higher earners:

Scrap higher-rate pension tax relief

This nuclear option would mean everyone, regardless of earnings, only gets tax relief at the basic-rate of 20% (equivalent to a 25% bonus on money saved in a pension).

This would save the Treasury billions but would also be a tax grab on anyone earning above £45,000, so may not be politically palatable.

Alternatively, a flat rate of relief could be introduced somewhere between 20% and 40%, although this would potentially be complicated to administer for employers.

Tinker with existing annual and/or lifetime allowances

A simpler option (politically at least) would be to lower the existing limits. This would likely create additional complexity as there would need to be new protections put in place for those who risk breaching a new, lower lifetime limit.

Adjust the annual allowance ‘taper’

The Treasury could shift the taper so the annual allowance drops from an earlier level of earnings than the current £150,000 starting point.

This would mean more people would be subject to a lower annual allowance, although the number would depend on where the income level was set.

Tom Selby,

Senior Analyst, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.