Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineChinese Internet Stars

We’re all familiar with Facebook (FB:NDQ), Amazon (AMZN:NDQ), Netflix (NFLX:NDQ) and Google – courtesy of its parent Alphabet (GOOG:NDQ), aka the FANG stocks. They’ve been blazing a trail this year on spectacular trading, with soaring key performance indicators (KPIs) like new subscribers and advertising revenues growing fast.

Unsurprisingly, FANG shares have gone bananas this year, smashing the performance of the S&P 500, and that’s even after the modest sell-off in big tech names recently. Investors love their huge cash flows and high growth rates, and are rightly willing to pay a hefty premium for that.

(Click on table to enlarge)

But how well do you know their Chinese equivalents, to so-called BAT stocks, Baidu (BIDU:NDQ), Alibaba (BABA:NYSE) and Tencent (0700:HK). You may be surprised to discover that they are almost as big as their US peers, throw off similarly large amounts of cash, have arguably more diversified businesses and, crucially, are growing even faster.

Shares in Baidu, Alibaba and Tencent have shot-up an average 55% in 2017 so far, led by Alibaba’s astonishing 81% rally.

HYPER GROWTH POTENTIAL

What really confounds investment experts is the BAT’s apparent ability to defy the law of large numbers, the idea that growth rates should converge towards the mean as an organisation gets bigger. Alibaba and Tencent have both been putting up revenue growth of around 40% for the past five years and current forecasts anticipate similar progress ahead.

‘I find it extraordinary,’ says Ali Unwin, manager of the Neptune Global Technology Fund (GB00BYXZ5N79). Unwin was a fan of the Chinese internet boom long before he helped launch his Neptune fund in December 2015, and his fund has held stakes in all three of BAT stocks during the 21 months since launch.

China still has enormous growth potential. One of the reasons that so many Chinese are adopting online commerce is historical and cultural. Outside of the big cities there is little retail infrastructure, as Neptune’s Unwin explains. Where we in the UK are all used to local high streets for shopping – with a butcher, baker and candlestick maker - little of that exists in rural China, where a single hardware store may exist.

And to buy anything more than everyday goods, an iPhone say, or a book, it’s either a trek to the nearest large town, a round trip that could be hundreds of miles, or buy online.

The nation also lacked a retail business establishment, leaving the way free for BAT companies to rapidly gain scale. The Chinese government’s ongoing ban on western social media businesses, including FANG plays Facebook, Twitter, Google previous exit and Amazon’s lacklustre progress in that market to date, have also helped.

MIDDLE CLASS MILLIONS

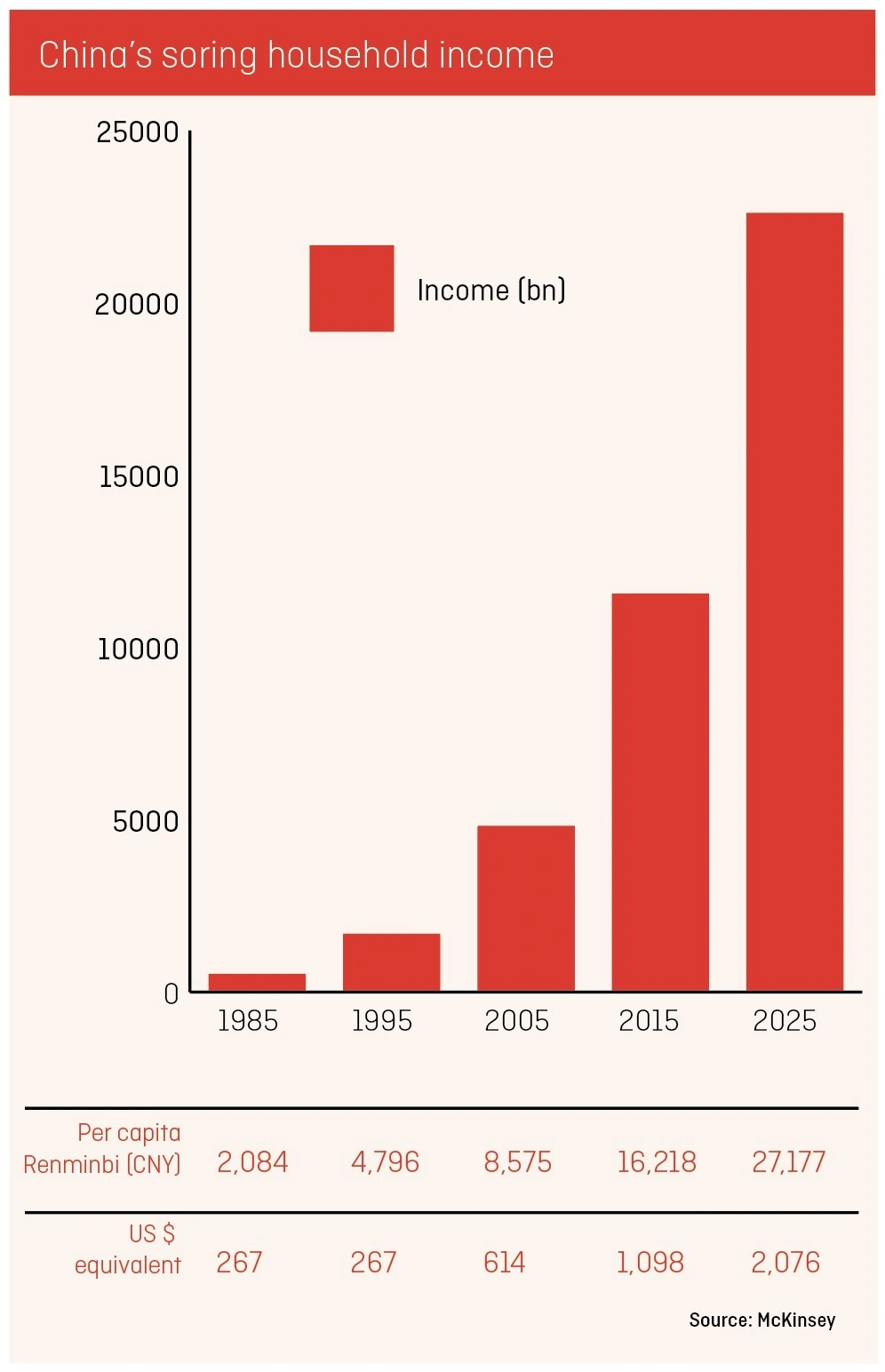

But the real growth engine is China’s rapidly growing middle class, which is having a massive impact on available spending power. Average household earnings have been outstripping the high single-digit growth of China GDP for several years, and with continue to do so.

Estimates suggest this middle class going from 50m or so a few years ago to 500m over the next decade, perhaps quicker. It is a demographic trend that Apple CEO Tim Cook has talked up in the past.

Why is this? Paul Danes, co-manager of the Martin Currie Asia Unconstrained (MCP) investment trust, uses a handy analogy. Imagine, for example, an average family earning the equivalent of say, $2,000 a year. About $1,800 of that goes on day to day necessities, food, keeping the light on and the home warm in winter, clothing, basic education and healthcare etc. That leaves $200 a year of disposable income for fun stuff – eating out, going to the pictures, and mobile phones.

But as demand for cheap Chinese labour rises from western markets, local salaries rise. If that average family’s annual income goes up to $2,500 a year, even with modest inflation in necessities (say to $1,900 annually), it means disposable earnings will have jumped 200% to $600 a year, and clearly a lot of that extra money is finding its way to BAT companies’ online platforms, one way or another.

‘We look for long-term, quality growth that is well-priced,’ says Danes. He’s a particular fan of Tencent despite the company’s frustratingly opaque disclosure.

(Click on table to enlarge)

For example, 70% of the firm’s revenue comes from ‘internet value-added services,’ with little more detail available for ordinary investors. Fund managers like Danes get the opportunity to meet management, and from those conversations have been able to work out that a massive 50% of the group’s entire income stems from gaming. Danes remains comfortable with that, but not everyone will be.

Neptune’s Unwin is less comfortable with this specific Tencent dynamic, which is why he has trimmed exposure to the company over the past few months. The fund manager remains right behind Alibaba, however, his preferred BAT play. He likes the Chinese Amazon/Ebay’s use of data to really get to know its customers and users, which helps Alibaba push increasingly relevant products and services that its user base really wants.

GOVENANCE RISKS

Baidu remains the arguable weakest link of the BAT trio. According to Neptune’s Unwin, slowing growth, the loss of key personnel (such as former chief scientist Andrew Ng earlier this year), greater competition in its core search markets and poor business transparency are key reasons why ‘I’ve sold, I’m concerned, ‘ the fund manager says.

Limited transparency and disclosure is a big issue for many investors, and Martin Currie’s Paul Danes also waves this potential red flag. Things like dual share structures that limited the voting power of outside investors.

Lesser understood risks come in the form of complex ownership vehicles, such as VIE schemes, explains Danes. This stands for variable interest entity, structures that involve owning stakes in holding companies that themselves own shares in the end business. This adds complication, while Danes also points out that these structures have never been legally tested in terms in courts.

HOW TO INVEST

Should you look for exposure to these fast growth internet stories? Yes, says Neptune’s Unwin, ‘if you are interested in material growth over the next couple of decades,’ he says. ‘It’s hard not to.’

Investors that do want to pursue the potentially vast Chinese internet growth opportunity might choose to do so through relevant funds or investment trusts. Danes’ investment trust may be an option. Other investment trust options include the Polar Capital Technology (PCT) investment trust or Allianz Technology Trust (ATT), both run by the highly respected Ben Rogoff and Walter Price respectively.

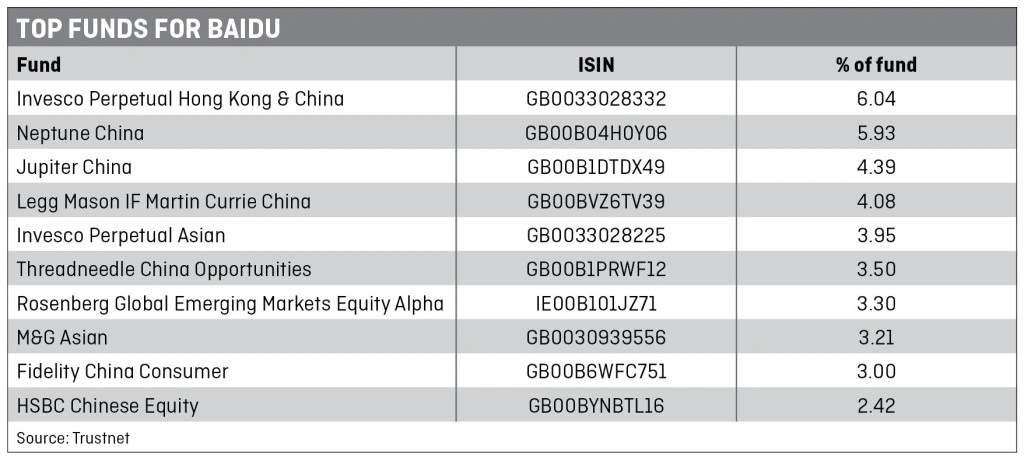

There are many funds with sizeable stakes, and we have pulled together handy lists of 10 with decent exposure to Baidu, Alibaba and Tencent in turn.

Alternatively, a small handful of exchange traded funds (ETFs) provide ways of tracking the wider Chinese internet investment theme. Some worth looking at in further detail include the BLDRS Emerging Markets 50 ADR Index Fund (ADRE), Guggenheim BRIC ETF (EEB), iShares MSCI China ETF (MCHI) or the KraneShares CSI China Internet Fund (KWEB). All but the iShares product are

US-listed ETFs.

‘Finding growth in China is not difficult,’ says Paul Danes, ‘but finding growth that translates into shareholder returns is more challenging.’

UNDERSTANDING THE BAT STOCKS

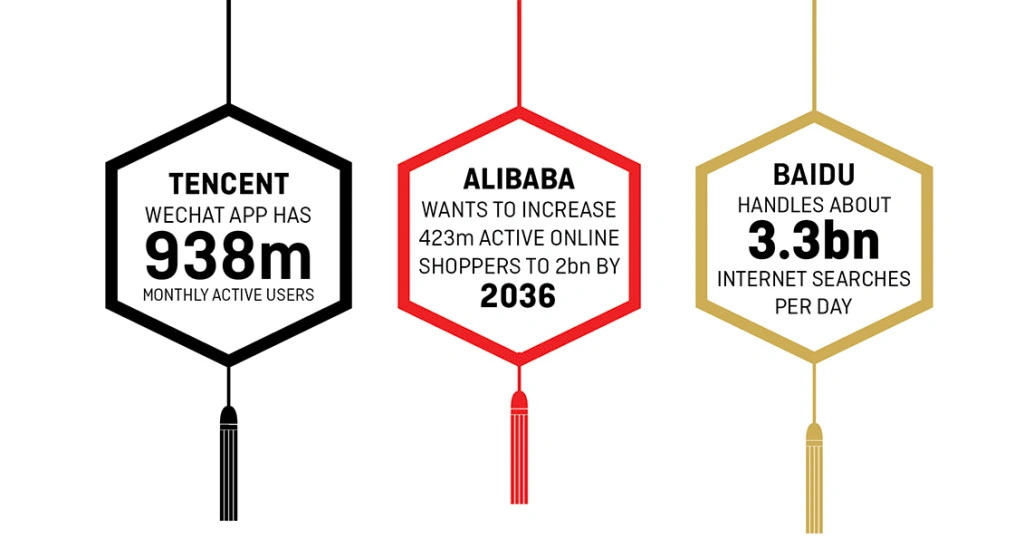

Nasdaq-listed Baidu is the largest Chinese language search engine in China, with an estimated 80% market share that sees about 3.3bn searches per day. About 80% of Baidu’s revenue comes from online ads across its search services, through applications such as Baidu Encyclopedia, maps, image search, music and video search, news search and so on.

Like its US peer, Baidu has expanded beyond its original search market. Its offering includes a translation service capable of recognising subtle differences between the many Chinese dialects.

These days the other 20% of its revenue comes from Baidu Wallet, a mobile payments app, and iQiyi, a video streaming service. This latter business has grown fast and is now reckoned to be the largest online video platform in China.

This is typically higher margin, subscription based income although it also means Baidu must spend fortunes in both buying in quality content as well as investing in its in-house production arm.

Baidu has undoubtedly benefitted from Google’s exit from the Chinese market in 2010 but it has come up against accusations of slowing growth and declining gross profit margins more recently.

In 2016 a gross margin of 50.1% represented the fourth straight year of decline and the 71% levels of 2012 seem like a long time ago. There’s also ballooning research and development costs as Baidu pushes into potentially large future markets (healthcare technology, artificial intelligence, augmented and virtual reality, for example).

(Click on table to enlarge)

Ranked as the largest IPO of all-time, when the company floated on the New York stock market in 2014, clawing in $25bn for selling shareholders. Alibaba operates China’s largest e-commerce platforms Taobao and Tmall.

The latter is a classic business to consumer platform (B2C) where online retailers sell to individuals, more like Amazon. In contrast, Taobao is a consumer to consumer (C2C) marketplace model that’s more in tune with Ebay (EBAY:NDQ).

With more than 700m Chinese already online, that’s about the same number of people as the entire EU population, and a far greater proportion of China’s 1.6bn-odd population is expected to join them in future. That gives Alibaba an enormous domestic market alone.

But that hasn’t stopped the company from expanding into new growth areas, such as cloud computing, digital media and entertainment.

Alipay, their third-party online payment platform, has now become the dominant player in the Chinese online payment market, which neatly links its main businesses into a coherent digital ecosystem. The big push now is to rapidly hike its active buyer base. It has around 423m buyers now but the company wants to hit 2bn by 2036, an astonishing ambition.

To do this Alibaba has made digital vertical investments into things like smart logistics, payment services, cloud computing, online marketing services, travel booking, music and video streaming. It has also fired the gun on overseas expansion, with Indonesia and other South East Asia territories in its sights. India is also on the cards.

The e-commerce giant has already steered the market to expect revenue growth of between 45% and 49% this year to 31 March 2018.

(Click on table to enlarge)

Tencent is an investment holding company that provides internet value-added services and online advertising across mainland China, Hong Kong and elsewhere internationally. That rather loose description basically covers a wealth of messaging and social networking platforms - Weixin/WeChat and QQ.

Weixin/WeChat is a phenomenon and one of the world’s fastest growing social apps. Released in 2011, the platform combines messaging, social communication and lots of mobile games, all in a single easy-to-use app. Estimates suggest the average Chinese user is on the platform for up to four hours daily. The equivalent figure for the likes of Facebook, Twitter, Instagram, Whatsapp is one-and-a-half hours.

QQ provides an internet-based all-in-one instant messaging service, with text messaging, video, voice chat as well as online/offline file transmission.

Both services have upwards of 800m monthly active users, implying than the majority use both services for different things. Website QQ.com, for example, is China’s largest local language portal integrating news, interactive communities, entertainment products and widely used basic services.

Like its peers, Tencent has also been busy expanding elsewhere, with cloud computing support, video streaming and its TenPay app, which are all growing fast. Integrating TenPay with its social platforms is also streamlining the purchase of products and services. The stock is listed in Hong Kong and Tencent is one of the largest public companies in Asia.

(Click on table to enlarge)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.