Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLessons from the pension freedoms

When the pension freedoms launched in April 2015, nobody was quite sure how savers would react.

Some feared people wouldn’t be able to resist draining their pots quickly to fund immediate spending needs. Others, including former pensions minister Steve Webb, insisted people could be trusted with their savings and wouldn’t splurge the lot on sports cars.

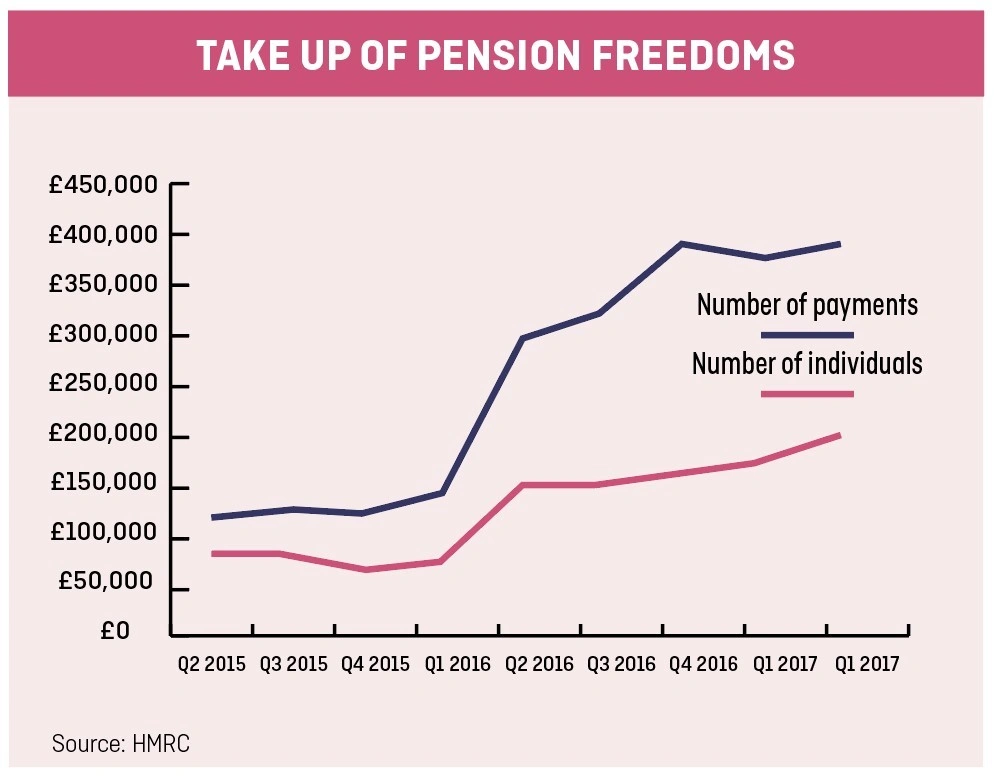

We are now beginning to get a clearer picture of how the flexibilities are being used and the retirement choices people are making.

So far the worst fears about people spending their retirement pots irresponsibly have not been borne out.

SAVERS MAKING SENSIBLE RETIREMENT INCOME DECISIONS

In fact, the average amount withdrawn per person has been steadily declining since April 2015, according to the latest Government stats. The average value of withdrawals dropped from £11,132 in the second quarter of 2016 to £9,300 – or £3,100 per month - in the same period this year.

More savers also appear to be setting up regular payments from their pensions, with the average number of payments per person increasing from 1.86 in Q2 2016 to 1.97 this year. It’s impossible to draw firm conclusions from this limited data, of course, but if people are taking less out of their pension at regular intervals that feels like a good sign.

The sustainability of these withdrawals is still not clear, however, and will depend on the circumstances of the individual investor. For example, a healthy 65 year old with a £1m pot can be confident withdrawals of £15,000 a year should last throughout their retirement (with something left over to pass on to the kids). If the same person had a total pot worth £100,000 then there is a serious risk their money would run out.

It’s absolutely vital you think about how long your fund will need to last when you make your retirement income plan. Someone retiring at 65 might need their pension to last for 30 years or more, so a sustainable withdrawal plan needs to reflect this.

TIP: THINK CAREFULLY ABOUT WHAT YOU WANT TO DO WITH YOUR MONEY

One of the mistakes a lot of people make when using the pension freedoms is to access their pot without really considering what they want to do with the money. For some it is a trust issue – the pensions ‘brand’ is tarnished and they would simply rather have the money elsewhere.

If this is you, think carefully about your decision. Pensions are extremely tax efficient, with any investment growth free of capital gains tax. Furthermore, if you take any taxable income from your pot, the amount you can subsequently save into a pension and receive tax relief will plummet from £40,000 a year to just £4,000.

You also need to think about how you will protect your money from rising prices. The rate of inflation currently stands at 2.6%, so if you withdraw your pension and put it in a Cash ISA paying an interest rate of 1%, the value of your savings will be guaranteed to fall in real terms. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.