Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStrong trading at EKF triggers earnings upgrades

Things are looking up for medical diagnostics specialist EKF Diagnostics (EKF:AIM) as its latest trading update (6 Jul) triggered a round of earnings upgrades, putting the spotlight on strong sales and profit growth potential over the next few years.

N+1 Singer analyst Chris Glasper upgraded earnings before interest, tax, depreciation and amortisation (EBITDA) forecasts by 10% to £9.6m for 2018. He also hiked EBITDA expectations by 9% to £10.4m in 2019.

What does EKF do?

The company develops, makes and distributes chemical reagents and analysers that measure glucose, lactate and haemoglobins among others. Its in-vitro diagnostic (IVD) products are used in GP surgeries, pharmacies, blood banks, clinics, hospitals and laboratories.

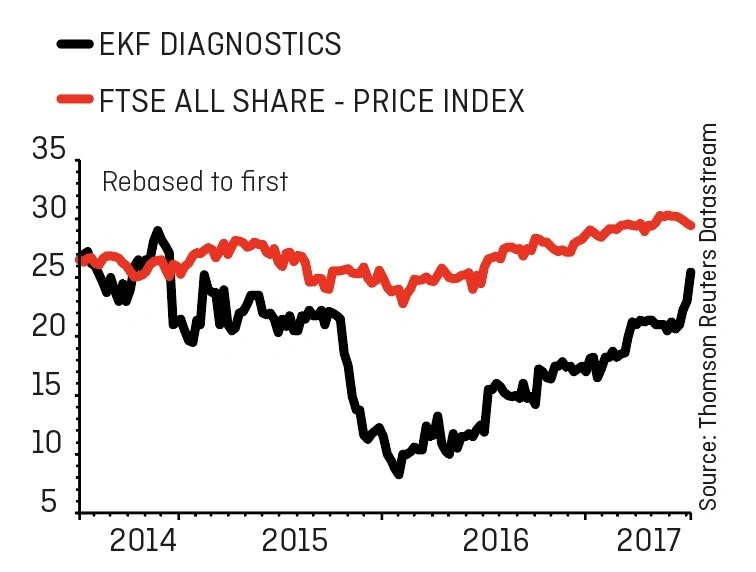

In the year to 31 December 2016, adjusted EBITDA was £6.1m, up from a loss of £0.3m in 2015 helped by a 16% uplift from currency movements.

The positive trend has continued. EKF says sales were ‘notably strong’ in June 2017 and this was driven by incremental organic growth rather than major one-off tenders. As a result, 2017 EBITDA will be ‘comfortably ahead’ of expectations, it says.

Panmure Gordon analyst Julie Simmonds has upgraded EBITDA forecasts by 8% to £8.6m for 2017. The analyst flags improved margins thanks to an increased focus on core product lines, which should help to drive growth in the future.

In particular, she highlights haemoglobin measurement device HemoPoint H2, diabetes monitor Quo-Test and testing reagent for ketosis, Beta-Hydroxybutyrate (BHB).

What's next for EKF?

EKF chief executive Julian Baines says the company’s recurring revenue model and global market focus has driven its momentum over the last 18 months.

The medical diagnostics company derives 50% of its sales from the US and also does significant business in Saudi Arabia and Eastern Europe.

With £4m in cash, Baines says the priority for EKF is to continually invest in the business and undertake share buybacks. He has ruled out any acquisitions.

EKF currently trades at 23 times forecast earnings per share for the year to 31 December 2017. While that is a rich rating, the company is poised for high earnings, sales and profit growth in the future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- Worst Performing Engineers

- Best Performing UK Engineers

- Surge in butter price points to looming supply shortage

- Odd share price activity ahead of 19% of UK takeovers in 2016

- Australia cuts export earnings forecast by A$13bn

- 3,142% gain made on Domino’s

- Soaring demand for cyber coverage

- Brand Architekts does the business