Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePositive trends and potential put spotlight on UDG

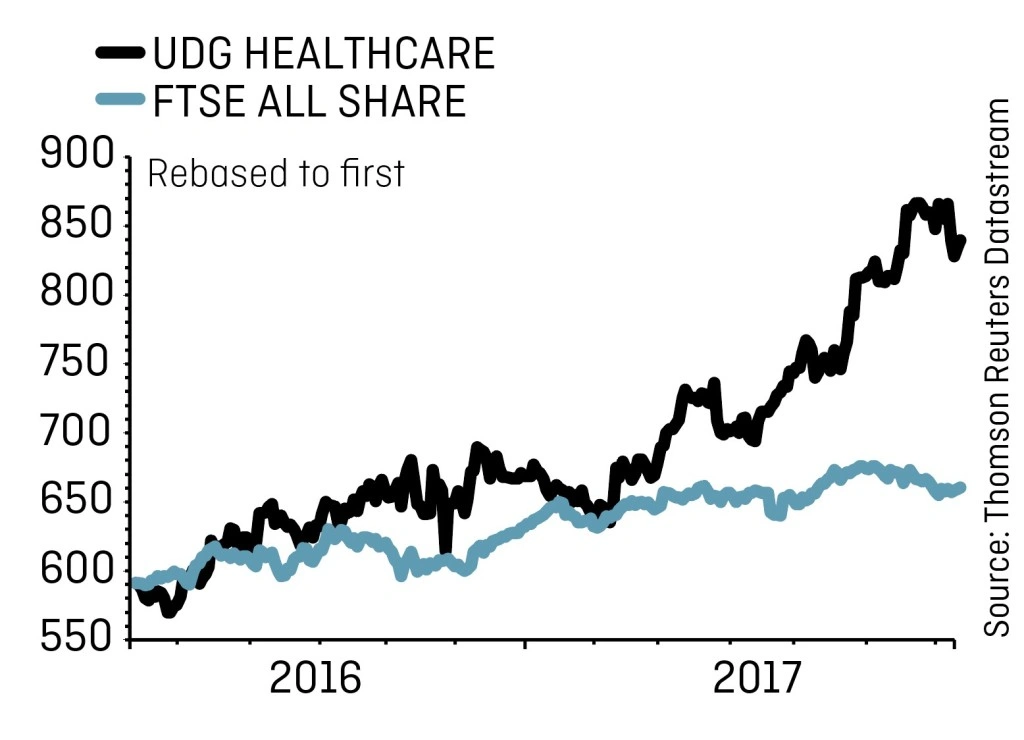

UDG Healthcare (UDG) 835p

Gain to date: 45%

Original entry point: Buy at 575p, 28 July 2016

Healthcare services provider UDG Healthcare (UDG) plans to take advantage of emerging trends and pursue further acquisitions

in higher margin services to boost growth.

Chief financial officer Alan Ralph anticipates strong organic growth, particularly in the Sharp packaging division which is benefiting from good demand in the US for serialisation services.

Shares in the firm have rallied by 25% this year and by 45% since we said to buy just under a year ago. We think the stock has further to run.

UDG is capitalising on rising drug sales in the developed world and further outsourcing of service work by larger companies.

Its United Drug division was sold for €407.5m in 2015, providing funds to make acquisitions, particularly in the fragmented healthcare communications sector.

In October 2016, the firm acquired STEM Marketing for £84m (€94.8m) to help pharmaceutical companies communicate the benefits of their drugs for clinical trials.

This week (12 July 2017) UDG announced the acquisition of US management consultant Vynamic in a deal worth up to $32m.

Liberum analyst Graham Doyle said in May this year that UDG should beat its full year earnings per share guidance of 15% to 18% growth in the year to 30 September 2017.

Doyle has a 930p price target for the stock.

By diversifying and expanding its services both organically and through acquisitions, UDG is positioning itself for further growth. Keep buying at 835p. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- Worst Performing Engineers

- Best Performing UK Engineers

- Surge in butter price points to looming supply shortage

- Odd share price activity ahead of 19% of UK takeovers in 2016

- Australia cuts export earnings forecast by A$13bn

- 3,142% gain made on Domino’s

- Soaring demand for cyber coverage

- Brand Architekts does the business