Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTime to buy the banks?

Banks were put through the ringer in the aftermath of the global financial crisis of 2008. Not only did the main players’ share prices collapse, a seemingly constant flurry of alleged rate fixing and misselling of products began. Bank bashing became a national pastime.

Almost a decade on, there are signs that this once dominant sector of the FTSE 100 is back with a vengeance. Is it time to invest in the UK banking sector again?

We think the answer is ‘yes’ on a selective basis. Our preferred banks are Lloyds Banking (LLOY) and HSBC (HSBA) both as a result of their generous dividend payments.

A few points to think about

You must first consider a few issues that could impact the sector. After the Brexit result, banks may have grave trouble exporting their financial services throughout Europe, one of the largest single markets in the world.

Conversely, another distraction from investing in UK banks is the tsunami of regulation coming from the EU which can lead to higher costs of doing business.

Against this backdrop, any investment into the banking sector needs to come with decent rewards to mitigate the risks. It’s no wonder banks are like marmite for many people; you either love them or hate them.

Another point to remember is that legacy claims for mis-selling products like mortgage-backed securities and payment protection insurance are still in play. Many banks have already shelled out billions of pounds in fines and there could still be a final wave of payments to make.

Furthermore, banks are intrinsically linked to the health of the economy. Paul Jackson, head of multi-asset at exchange traded funds provider Source ETF, says the performance of banks ‘is usually not good when the economy and property markets weaken’.

Growing credit concerns

Finally, you must consider the impact of rising inflation and growing consumer dependence on credit to fund lifestyles. That is a very important issue, although some experts believe the market might be overly pessimistic.

‘UK domestic banks have underperformed since the Brexit referendum, in part because investors worry about the risk of bad debt write-offs on UK consumer credit loans as rising inflation erodes real incomes,’ says Morgan Stanley.

‘We think these fears may be too bearish and the market is likely to be positively surprised by the asset quality of major UK banks.’ It backs up this statement with four key points:

1 Employment is still likely to grow and so the unemployment rate increases should be moderate

2 Interest rates are likely to remain low and affordability metrics are benign

3 Tighter credit standards than pre-crisis give banks some protection from risk

4 A considerable proportion of consumer debt is sitting outside the major banks

Indeed, the Bank of England’s regulatory body (the PRA) is putting pressure on banks with regards to lending. That could take the heat of consumer credit growth, leading to higher profit margins and cushion the banks from rising impairment charges, says Morgan Stanley.

Banks have been asked to review their underwriting standards and provide information by September so the PRA can decide if further steps are needed to rein in risky lending.

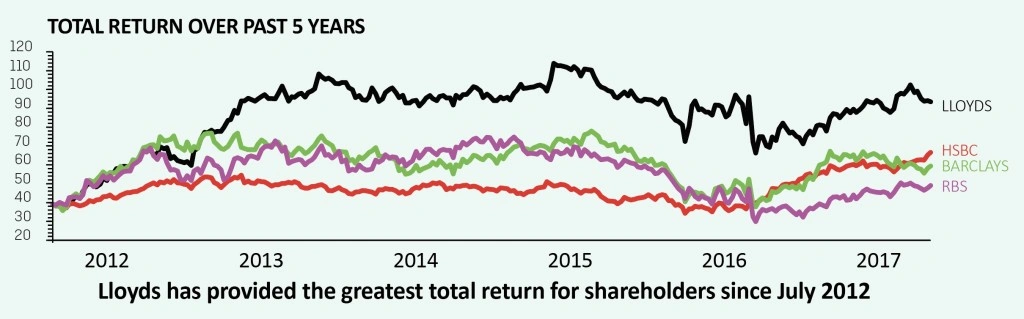

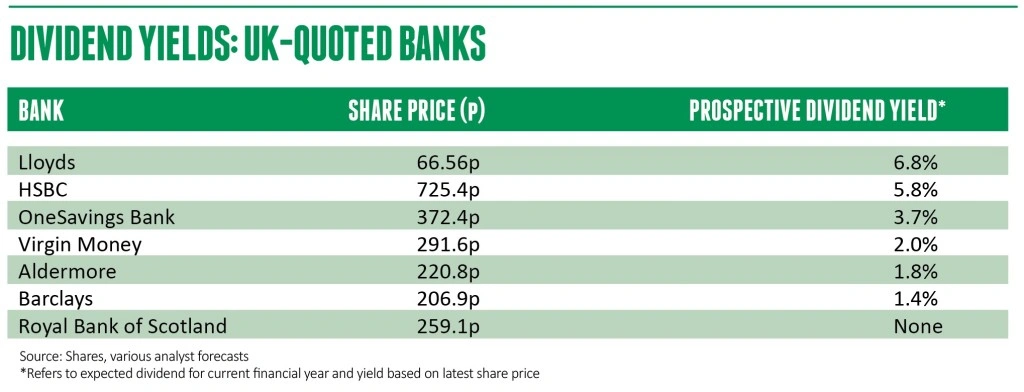

Lloyds Banking Group (LLOY) 66.56p

Bull case

Lloyds reinstated its dividend policy in 2014 and the level of payment has been growing ever since. It even announced an extra dividend payment in February this year after reporting its largest profit in a decade.

It paid 3.05p per share for the 2016 financial year, including the recent 0.5p special dividend. That equates to a 4.6% historic dividend yield based on the current share price.

The bank is forecast to pay 4.5p for the 2017 financial year, taking the yield to a prospective 6.8%. The dividend is then forecast to pay 5p in 2018, implying a 7.5% yield.

Lloyds has a healthy common equity tier one (CET1) ratio of 13%, well above the level set by regulators to prevent a repeat of the financial crisis.

The tier one ratio is a measure of a bank’s core equity capital compared with its total risk-weighted assets.

In plain English, it is the size of a bank’s cash reserves against its loans, adjusted to account for the riskier assets in the portfolio such as unsecured lending. It is a cushion that should protect against potential losses should there be another serious economic downturn.

Rob James, who co-manages the Old Mutual Global Investors UK Alpha Fund (GB0032544065), says Lloyds is a simple story. ‘It started paying dividends then special dividends,’ he explains.

Analysts at Morgan Stanley are particularly bullish on Lloyds, with their forecast 2018 impairment charges (in banking terms usually a loan default) around 30% below the consensus view.

They view Lloyds’ valuation as ‘appealing’ as its stock trades on a price-to-earnings ratio of 8.7-times, a 25% discount to the European banking sector.

Lloyds recently bought MBNA’s credit card business for £1.9bn. The deal will increase its net interest margin (NIM), the difference between income from lending and the cost of funding. It is a key indicator of a bank’s profitability.

Before the deal it stood at a respectable 2.8%, following the acquisition the figure is set to increase to 2.9%.

Bear case

Jamie Clark, co-manager of the Liontrust Macro Equity Fund (GB00B8H9GB86), thinks Lloyds is ‘under pressure in a fiercely competitive UK mortgage market, overly geared to a UK consumer that is feeling the pinch of inflation and static real wages, and its dividends may disappoint’.

A note by Morgan Stanley shows that since Lloyds bought MBNA it has the highest amount of UK consumer credit at £42.8bn.

Investment bank Berenberg also says Lloyds had one of the highest loss rates in each UK lending category in the Bank of England’s 2016 stress tests.

SHARES SAYS:

Lloyds is a great stock for those seeking income. Buy.

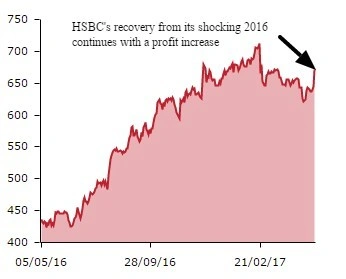

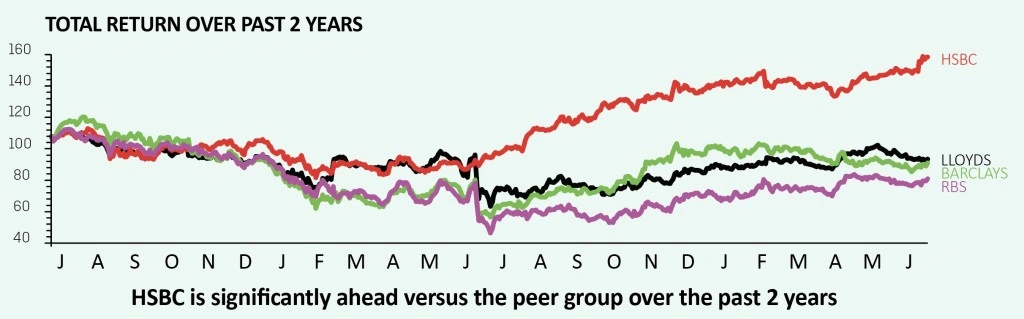

HSBC (HSBA) 725.4p

Bull case

Two years ago there were worries whether HSBC could maintain its dividend. These fears have dissipated and the bank continues to pay attract cash sums to its shareholders.

The dividend yield is currently 5.8% based on historic and forecast data. Analysts expect HSBC’s dividend payment to stay flat for the foreseeable future. However, some analysts believe the company could generate significant amount of surplus cash over the next three years, raising the potential for special dividends down the line.

Liontrust’s Clark says: ‘This March we bought into HSBC, marking the first time we had owned shares in one of the big UK incumbent high street banks for five years.’

He says HSBC has engaged in a series of non-core asset disposals, which have boosted its regulatory capital and raises the prospect of higher dividends.

The disposal of its loss-making Brazilian operations alone reduced its risk weighted assets by $37bn and boosted its CET1 ratio by around 0.65%. It now stands at around 13.6%.

HSBC’s global reach also aids the bank and not just by reducing its exposure to Brexit related fallout. With US interest rates on the rise, HSBC’s operations in that location are set to benefit from a higher NIM.

Old Mutual’s James says HSBC puts its surplus cash into two-year US treasuries that currently yield around 0.5%. If the Federal Reserve raises interest rates to 1% that would in turn increase the bank’s profitability. James is among the experts who believe the bank will return any surplus cash in the form of dividends.

Bear case

Investec analyst Ian Gordon says the bank has seen a sharp decline in its NIM over the last 10 years, moving from 3.1% to 1.6%. ‘That’s a function of a run-off of high margin low quality business such as household in the US coupled with the low interest rate environment,’ he explains.

The analyst believes returns have been structurally weak and below a 10% return on equity target which he doesn’t expect the bank to reach before 2020.

Given HSBC’s Asia exposure, it could be hurt by any economic slowdown in China.

The bank trades on a premium price-to-book ratio of 1.3-times so some investors may consider the stock to be fully valued.

SHARES SAYS:

The dividend is very attractive, so buy the shares for income.

Barclays (BARC) 206.9p

Bull case

Despite Barclays cutting its dividend by more than half earlier this year, some analysts believe there are still good reasons to invest in the bank.

For example, Barclays has largely disposed of its Africa business which has boosted its CET1 by 0.73%, now forecast to be 12.6% for 2017.

David Smith, who runs Henderson High Income Trust (HHI) investment trust, says: ‘Barclays’ retail division has good market share and is producing good returns. Barclaycard is one of the best returning credit card businesses globally.’

Barclays is among the cheapest of UK incumbents, with a price-to-book ratio of just 0.7. This means that you’re paying less than the value of the assets of the bank (which are plentiful).

The bank is well ahead of its restructuring target to reduce its non-core risk-weighted assets from £110bn identified in 2014. It has already brought these assets down to around £25bn.

The investment banking division, long seen as a drag on the business, is showing signs of improvement. The hire of chief executive Jes Staley, former boss of best-in-class JP Morgan’s investment bank, is widely viewed as a good move.

Barclays’ dividend is forecast to start growing again in the 2018 financial year, putting the yield in the 4% territory.

Bear case

Barclays has taken two reputational hits this year alone. Jes Staley attempted to unearth the identity of a whistle blower in April which led to a regulatory investigation.

The bank is also facing potential charges by the Serious Fraud Office relating to a 2008 emergency fund raising of £7bn. The bank is potentially looking at two charges; conspiring to commit fraud and unlawful financial assistance.

Furthermore, Barclays is in a dispute with the US Department of Justice (DoJ) over mis-selling mortgage-backed securities during the financial crisis. The claim was brought by the DoJ last year and could potentially cost the bank billions of pounds in fines.

SHARES SAYS:

Barclays’ disposal of its Africa business makes this stock more appealing due to its increase in regulatory capital. Its retail and Barclaycard businesses are performing well and its investment banking issues are being addressed. However, we are uncomfortable with the threat of significant fines, meaning this is not a stock which we would want to own at present. One to watch.

Royal Bank of Scotland (RBS) 259.1p

Bull case

Berenberg regards Royal Bank of Scotland’s strategy of growing lower risk lending and cutting costs as superior to its rivals. For this reason it regards Royal Bank of Scotland’s core earnings as more sustainable.

Dividends are forecast to resume in 2018, circa 3% yield.

Its CET1 capital ratio is also forecast to improve this year, from 13.4% to 13.9%, according to Investec.

Bear case

Royal Bank of Scotland has been loss making for nine consecutive years and isn’t expected to make a profit until at least 2018. It also currently doesn’t pay a dividend, unlike its peer group.

Investec’s Gordon says that ‘unresolved conduct issues continue to dog the bank’. It incurred £7.76bn in exceptional items last year.

RBS is last in the queue to resolve legacy mortgage-backed securities with the DoJ which could potentially hit the bank for billions of pounds in fines.

SHARES SAYS:

Avoid. Despite its decent core business performance, there are still too many risks when it comes to possible fines that mean the bank may not return to profitability for some time.

The Challenger Banks

Ian Gordon at Investec believes there is more value in the challenger bank section of the sector rather than the FTSE 100 stalwarts.

He says: ‘challenger banks are materially mispriced based on a mistaken view that they are vulnerable to a slowdown where the opposite is true as they have far greater lending buffers and minimal unsecured exposure’. He adds: ‘As they are small players in niche or large markets they can continue to grow even as markets slow.’

Virgin Money (VM.) 291.6p

One of the larger, more mainstream challenger banks with a market cap in excess of £1.3bn. It trades on forecast earnings for 2017 of just 8-times. This is predicted to drop to what Gordon describes as ‘fairly absurd’ 5.8-times in 2019.

Aldermore (ALD) 220.8p

The bank is involved in mainstream activities such as mortgage lending. It has a respectable NIM of 3.5%, bettering some of its FTSE 100 peers.

Shailesh Raikundlia, an analyst at Panmure Gordon, includes Aldermore in his firm’s conviction list for 2017 with a 285p price target.

‘At current valuations we continue to believe Aldermore remains significantly undervalued despite current worries regarding the UK economic outlook,’ he says. The stock currently trades on 7.5 times forecast earnings for 2017.

Onesavings Bank (OSB) 372.4p

The bank is a specialist lender and retail savings group with a reputation for being big in buy-to-let.

OneSavings had a return on equity figure of 34.6% in 2016. This is expected to drop to 26.7% for 2017, which is still an attractive figure.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- Worst Performing Engineers

- Best Performing UK Engineers

- Surge in butter price points to looming supply shortage

- Odd share price activity ahead of 19% of UK takeovers in 2016

- Australia cuts export earnings forecast by A$13bn

- 3,142% gain made on Domino’s

- Soaring demand for cyber coverage

- Brand Architekts does the business