Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCityFibre part of superfast UK broadband solution

A superfast broadband Britain is the aim and fibre network builder CityFibre Infrastructure (CITY:AIM) is an exciting way for investors to access the opportunity.

The AIM-quoted business builds ultra-fast fibre networks in medium-sized cities. Think Sheffield, Bristol, Glasgow and Leeds; these are a handful of the 42 locations being turned into ‘Gigabit Cities’ across the UK capable of providing local businesses and government organisations with state-of-the-art digital infrastructure.

It’s a risk managed model because CityFibre insists on long-term anchor tenants before committing resources, guaranteeing funding payback. This typically means a local authority or internet service provider (ISP). Once operational, service providers sell services to end users, paying CityFibre on a subscription model. If growth fails to materialise, intense capital expenditure (capex) can be ratcheted down accordingly.

Last year to 31 December 2016 was transformational, scaling the business up thanks to buying infrastructure parts of KCOM (KCOM) and Redcentric (RCN:AIM). This sparked a massive 230% jump in end users connections, or 63% in pre-acquisition organic terms. Contracted new connections jumped 206% or 58% organically, helping overall revenue increase from £6.4m to £15.4m.

Analysts value its existing fibre networks replacement value at £155m, solid asset backing for the current £177m market capitalisation. The company has £106m worth of committed future revenue over the next few years as it stands.

Funding rethink

Now Ofcom is starting to show is teeth after years of under investment in UK fibre infrastructure. For years BT’s (BT.A) Openreach has had the market largely to itself but the watchdog is demanding competition, sending a clearly encouraging signal to CityFibre.

Management are reviewing £100m of funding capacity, most at onerous interest charges. Net debt was £38.6m meaning a £7.3m interest bill last year. CityFibre will get better terms as its revenue visibility continues to improve, while the company refuses to look at equity funding due to the low valuation.

Longer-term, there also looks like a very good chance that CityFibre gets bought out, particularly with the UK’s major mobile operators all vying for Fibre network access for their own multi-play service offerings (where customers get home phone, mobile, broadband and even digital TV as a bundle).

FinnCap anticipates £24m of revenue this year, and £38m in 2018, implying this year’s £4.8m pre-tax loss will turn into a £2.1m pre-tax profit next year aided by near 90% gross profit margins. The broker has a 130p target price on the stock, while fund manager star Neil Woodford is a major stakeowner with 17.2%. (SF)

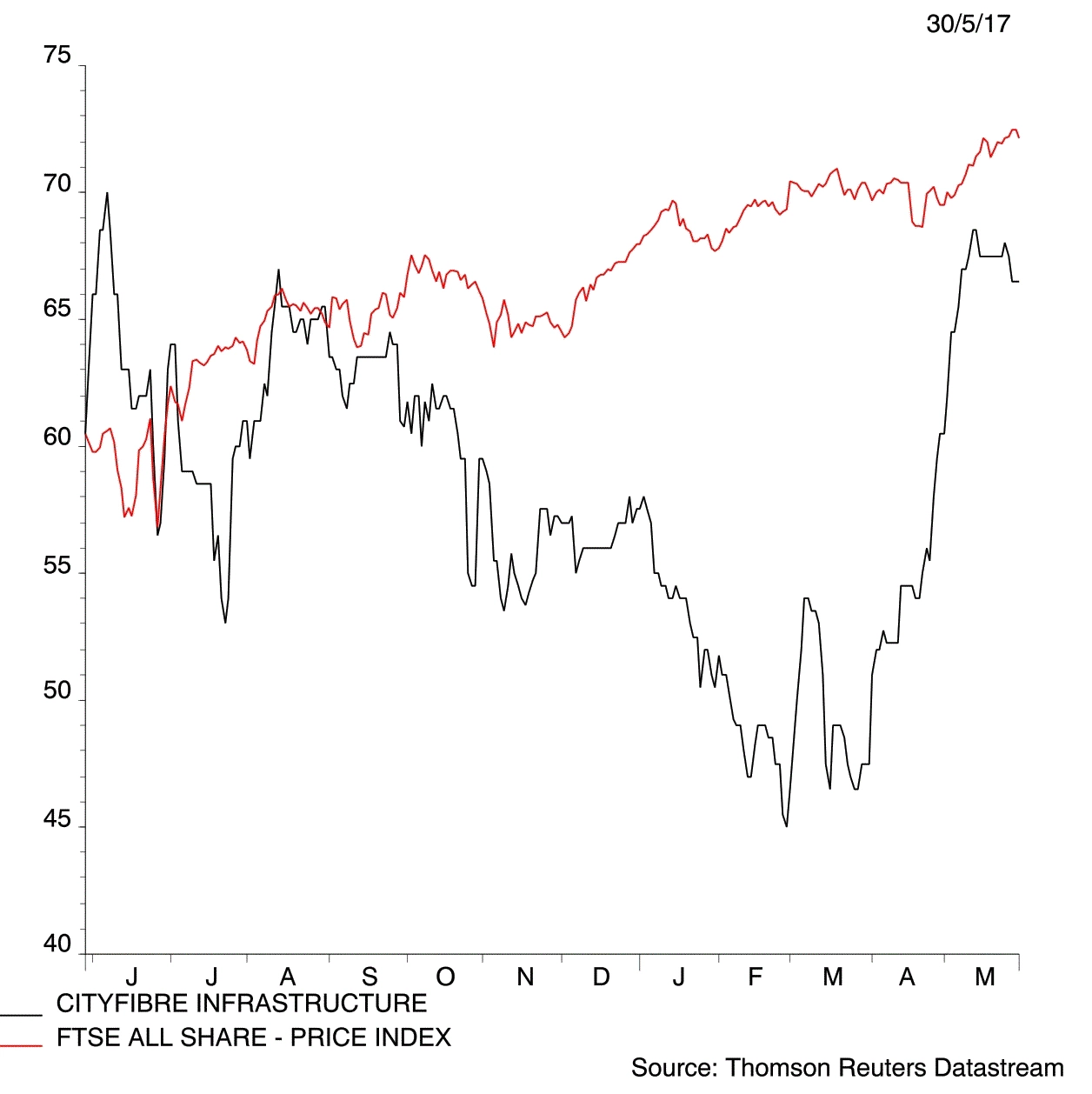

CityFibre Infrastructure (CITY:AIM) 66.5p

Stop loss: 53p

Market value: £177m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.