Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy PayPoint faces downgrades?

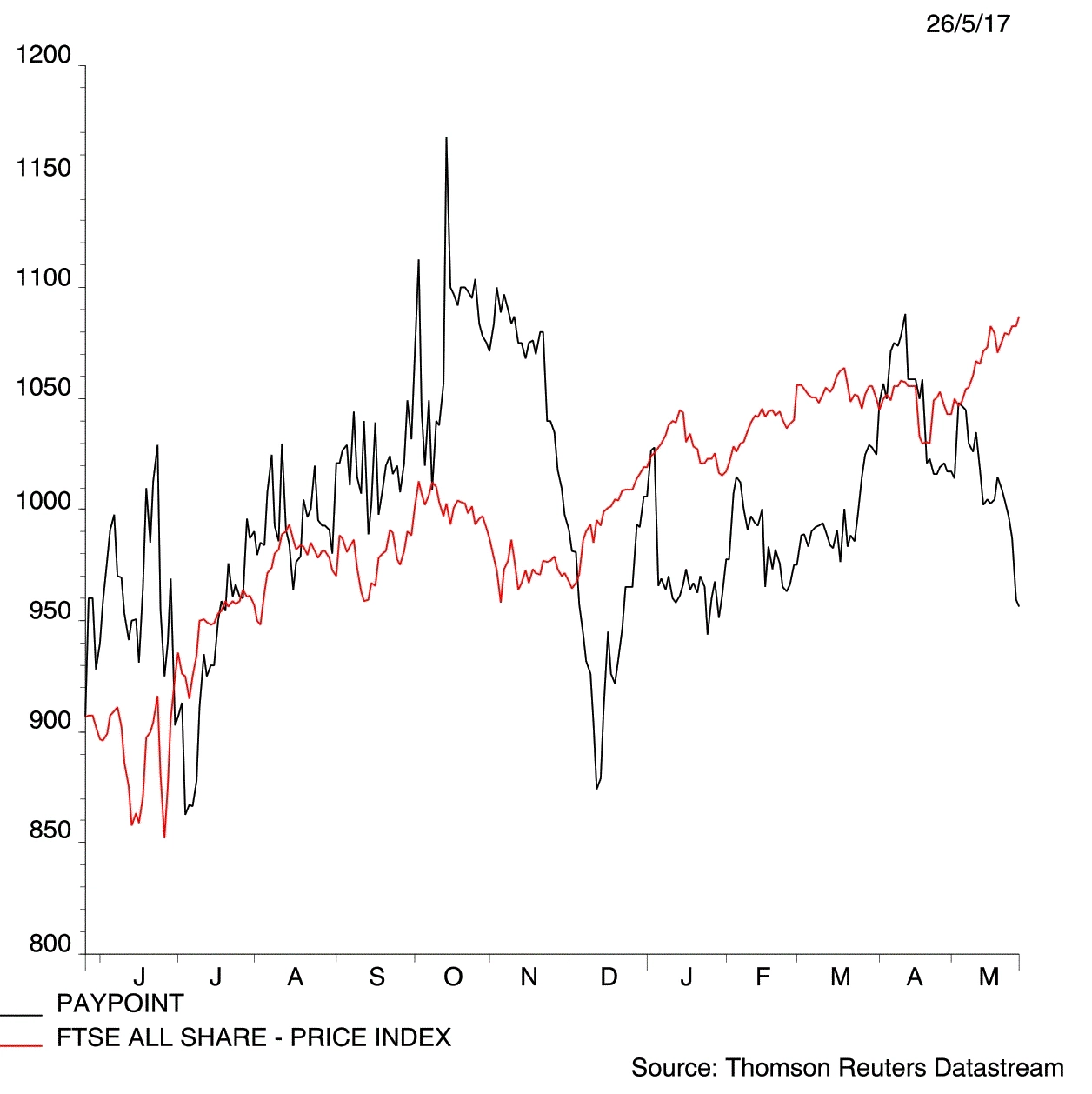

Investors in convenience store payment specialist PayPoint (PAY) should be aware of growing risks to the investment case, as reflected by a weak share price since April.

Full year results on 25 May perhaps represent a turning point for the business. Net revenue was flat at £123.9m and adjusted operating profit nudged ahead by 4% to £52.3m.

The mobile payments business has been sold and a new retail payment system has started to be rolled out to convenience store operators. Its parcel delivery and collection joint venture Collect+ has become profitable.

Why the gloomier outlook?

Investment bank Liberum has downgraded its earnings per share forecast for the year to 31 March 2018 by 9%; and slashed the following’s year forecast by 11%.

Fees to Collect+ partner Yodel will increase; a £2.4m VAT recovery in 2017 is non-recurring and the end of a government service this summer will cost PayPoint £4m a year in lost revenue.

The latter relates to the Department of Work & Pensions winding up its Simple Payment Service, which allows consumers to receive benefits as cash via PayPoint stores.

It is also worth considering changes to the way customers are paying for their energy using PayPoint’s services. The company makes money per transaction but consumers are now paying larger amounts, fewer times. While impacting its net revenue, PayPoint is hoping to mitigate this loss in volume by improving margins.

Liberum believes the Romanian operations and PayPoint’s core retail services will continue to grow, but expects further money will be spent on the PayPointOne retail terminal.

‘The incremental sales from PayPointOne terminals in the 2017 financial year are a little more than £500,000. Management continues to target 3,000 to 4,000 customers per year and PayPoint has started well with 3,600 six months after the launch in September 2016,’ says Liberum.

‘We continue to believe that medium term, 20,000 to 30,000 retailers should be possible, particularly given that all of PayPoint’s retail partners will eventually be migrated to PayPointOne.’

What do others say?

Canaccord Genuity has also slashed its 2018 and 2019 financial year estimates, lowering pre-tax profit forecasts by 9% for each of the two years.

‘PayPoint is undergoing a transition. Headwinds in the traditional payments business are being offset by growth in retail services (PayPoint One, ATMs, card acceptance) as PayPoint aims to pivots itself at the heart of running the retailers’ business,’ says Canaccord analyst Daud Khan.

He has a £11.62 price target for the next 12 months whereas Liberum expects to shares to ease back to 900p. They traded at 962.71p at the time of writing.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.