Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSciSys ignites growth flame

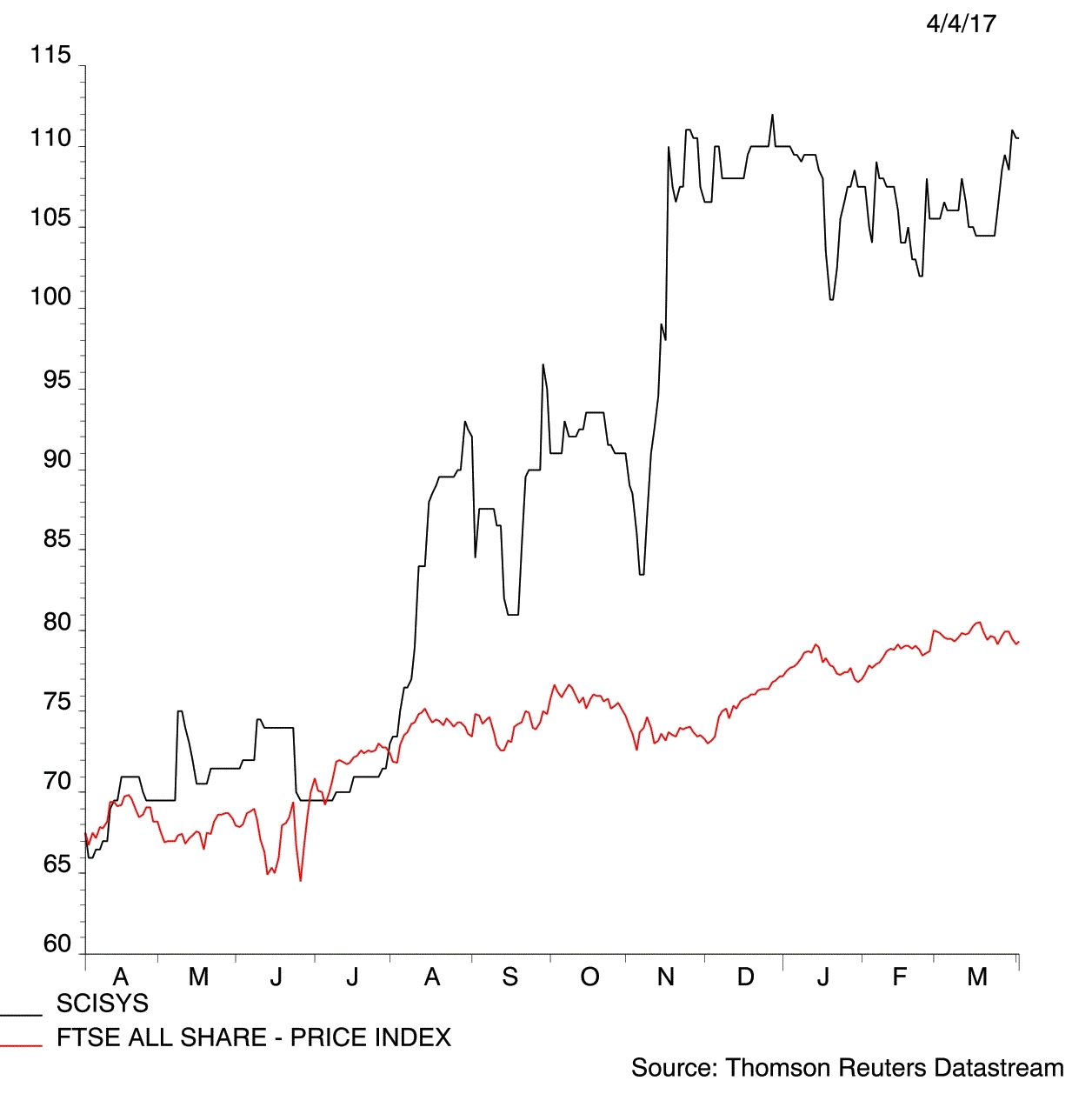

After several years of treading water SciSys (SSY:AIM) has at last found its growth groove and Shares believes there is a substantial profit opportunity for investors.

Our back of an envelope calculations suggest that a modest price to earnings (PE) multiple re-rating to 14 by the end of this year could see the share price hit the 170p mark, implying 54% upside. The current 2018 PE stands at just 9.1.

Chippenham-based SciSys provides project based IT skills and services to large public sector (the ESD division), broadcast media (M&B) and space industry clients.

The Ministry of Defence (MoD) is a big public sector client. SciSys also does a lot of work with the European Space Agency (ESA), including its Galileo project and on Mars missions, and the satellites industry.

This has previously made the company look rather disjointed with a hotch potch of software enterprises with little reason to sit under the same corporate umbrella. But more recently management has been able to spin internally developed intellectual property (IP) into multiple applications.

For example, it has piggy-backed initial project information management work for the RNLI to build its MACSYS integrated marine management platform. A similar development root produced its PLENITER advanced metrological system.

Exciting opportunity in broadcast market

Exciting in the near-term is the potential from its broadcast media arm, its most profitable division with operating profit margins of a 31.25% in 2016 (ESD 26.9%, Space 21.1%).

Up until the £23.8m acquisition of German business ANNOVA in November 2016 it was also its smallest division.

ANNOVA is a newsroom software supplier to many of the biggest European media organisations. It has a 12-year deal with the BBC. SciSys sees ANNOVA IP as a perfect fit to develop existing and new products, plus it brings a substantially bigger international presence.

The deal led analysts to increase their 2017 earnings forecasts for SciSys by 25%, which gives you some idea of the potential.

Management are a naturally cautious bunch, demonstrated by the company’s solid cash generation and dividend that will yield 2% this year.

So if FinnCap sees earnings per share jumping from 9p to 11p in 2017 (a 22% increase), it’s because the company is very comfortable with that estimate. This puts the possibility of beating expectations on the cards too, and positive newsflow through the year could act as a catalyst for a share price re-rating. (SF)

SciSys (SSY:AIM) 110.5p

Stop loss: 88p

Market value: £32.1m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Special dividend on cards for Central Asia Metals?

- FTSE 100 dividend delight on overseas earnings boost

- Margin pressure hits ASOS

- Polar Capital makes a mint after Miton raid

- Brace yourself for more British takeovers

- CityFibre seeks fresh funding deal

- Sophos shines and shares at record high

- Genus gets green light to launch GSS