Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineISAs: Where to put your £20,000

You can now tuck £20,000 into a tax-sheltered ISA every year, a 31% increase on the previous tax year. To help you take advantage of this generous allowance, we’ve produced a list of 10 must-have stocks to fill your ISA.

The list includes a mix of selections from the Shares team and some picks from leading equity analysts. We’ve split them into five groups, making it as easy as possible for you to pick and choose certain types of investments.

The five groups are income, growth, recovery trades, picks for investors with an appetite for higher-risk investments and top quality businesses. All the stock ideas are aimed at an investor with a longer-term time horizon.

On a related note, anyone new to investing may prefer to first invest in funds in order to spread risks and develop a strong backbone to their portfolio before adding individual stocks. Read our recent articles on filling ISAs with funds here and here to get a head start.

How should I allocate my money?

So how should you spread up to £20,000 across a new ISA? Anyone able to invest a large lump sum needs to think about the risks of putting all that money in just a few stocks – or whether they would be better served by spreading the cash among five or more holdings.

What about those who can only afford to invest a little bit out of their pay packet every month? We’d suggest you consider prioritising investments that will enhance your portfolio, rather than duplicate existing holdings.

Go for quality over quantity

Many experts believe 20 holdings, whether individual shares or funds, is the maximum you need in an investment portfolio.

Anyone new to investing and fortunate enough to have a large lump sum of cash to invest may wish to spread some of their £20,000 ISA allowance across 10 funds, investment trusts or exchange-traded funds (ETFs). That would form the foundations of your portfolio, so you could then invest in five or so ‘high conviction’ stocks at any one time.

The benefits of regular investing

Many of you will not be fortunate enough to have £20,000 to invest straight away but the good news is you can drip feed funds from your monthly pay packet into the market. Regular investment even offers some handy benefits.

Many stockbrokers offer something called a ‘regular investment service’. You can place an order for a specified amount of money to buy the same share or a fund each month in the same way you’d set up a direct debit to pay your utility bill or a gym membership, for example.

Transaction fees are generally much lower than normal trading costs, often as little as £1.50 a time versus £10 typical dealing fee.

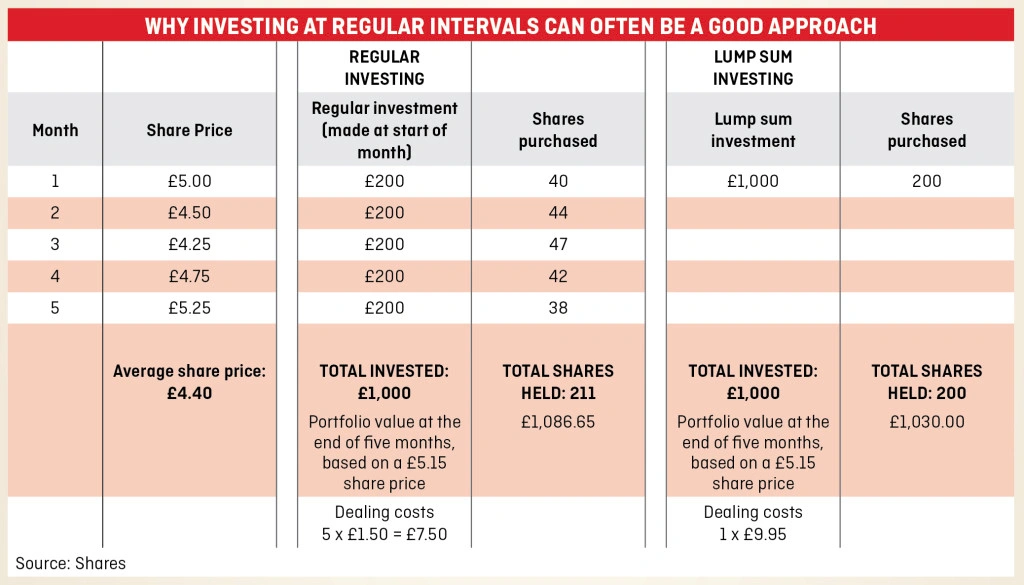

Investing regularly also enables you to take advantage of an effect known as pound cost averaging. This process can iron out the ups and downs in the price of a fund or share over time. Your money buys you more shares or fund units when the price is low and fewer when the price is high.

That can be better than mistiming the market and only making one transaction and buying when the price was high, for example.

The hypothetical example below compares the return on £1,000 invested as a lump sum versus regular investment over five months. It shows how buying regularly at higher and lower prices can sometimes result in you owning a greater number of shares than via lump sum investing.

This is just an illustration and not a guarantee you will make more money this way.

TASTY YIELD STOCKS: GREAT FOR INCOME

National Grid (NG.) £10.18

National Grid (NG.), the UK’s largest listed utility worth just shy of £36.9bn, sits in an enviable position.

While increasing competition bites across the retail energy field as consumers are encouraged to switch, National Grid owns the infrastructure through which homes and businesses get their power regardless of supplier.

Like most utility stocks, income is the big attraction and National Grid’s implied yield of 4.5% for the year to 31 March 2018 stands roughly in line with the wider sector. It comes with an RPI-beating growth promise, adding a level of natural hedge if inflation does hang around for a prolonged spell.

Investors also stand to share a potential £4bn windfall in the near future from the group’s sale of US gas assets. That implies a rough 85p per share special dividend, according to analysts, plus an accompanying share consolidation and £1bn share buyback. (SF)

Card Factory (CARD) 271.6p

Specialist greeting cards-to-gifts retailer Card Factory (CARD) is a ‘highly attractive’ business paying very attractive dividends, according to investment bank Investec.

Its vertically integrated model, spanning in-house design, printing and retailing, is a key point of differentiation. It reduces external costs which Card Factory can pass on to customers and enables it to generate industry-leading margins and prodigious sums

of cash.

The model enables Card Factory to keep prices low, despite currency-driven cost headwinds; competitors will be forced to raise prices and close stores. We don’t believe digital greeting cards are a structural threat.

Record full year results revealed 3.8% growth in underlying pre-tax profit to a better-than-expected £85.1m, albeit on slower like-for-like sales growth of 0.6% (2016: 3%).

Card Factory continues to expand via new store openings and sees scope to improve the performance of its Getting Personal website.

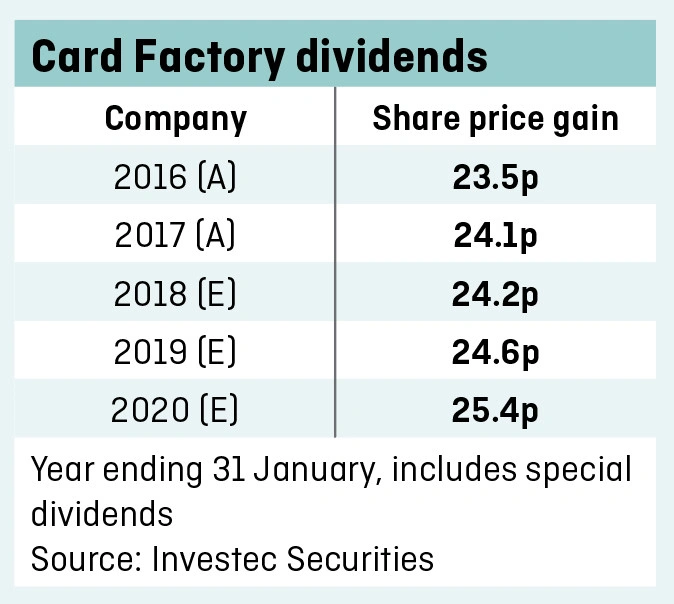

The company lifted its ordinary dividend by 7.1% to 9.1p in its most recent financial year. It also paid 15p special dividend on top.

Investec expects another batch of generous payments to shareholders in the current financial year. It forecasts 24.2p per share in total (including another special dividend) which implies 8.9% yield.

Looking at the forecasts beyond 2017, it seems Investec expects the special dividend to be a regular feature every year. (JC)

GROWTH FIRMS: ON A WINNING STREAK

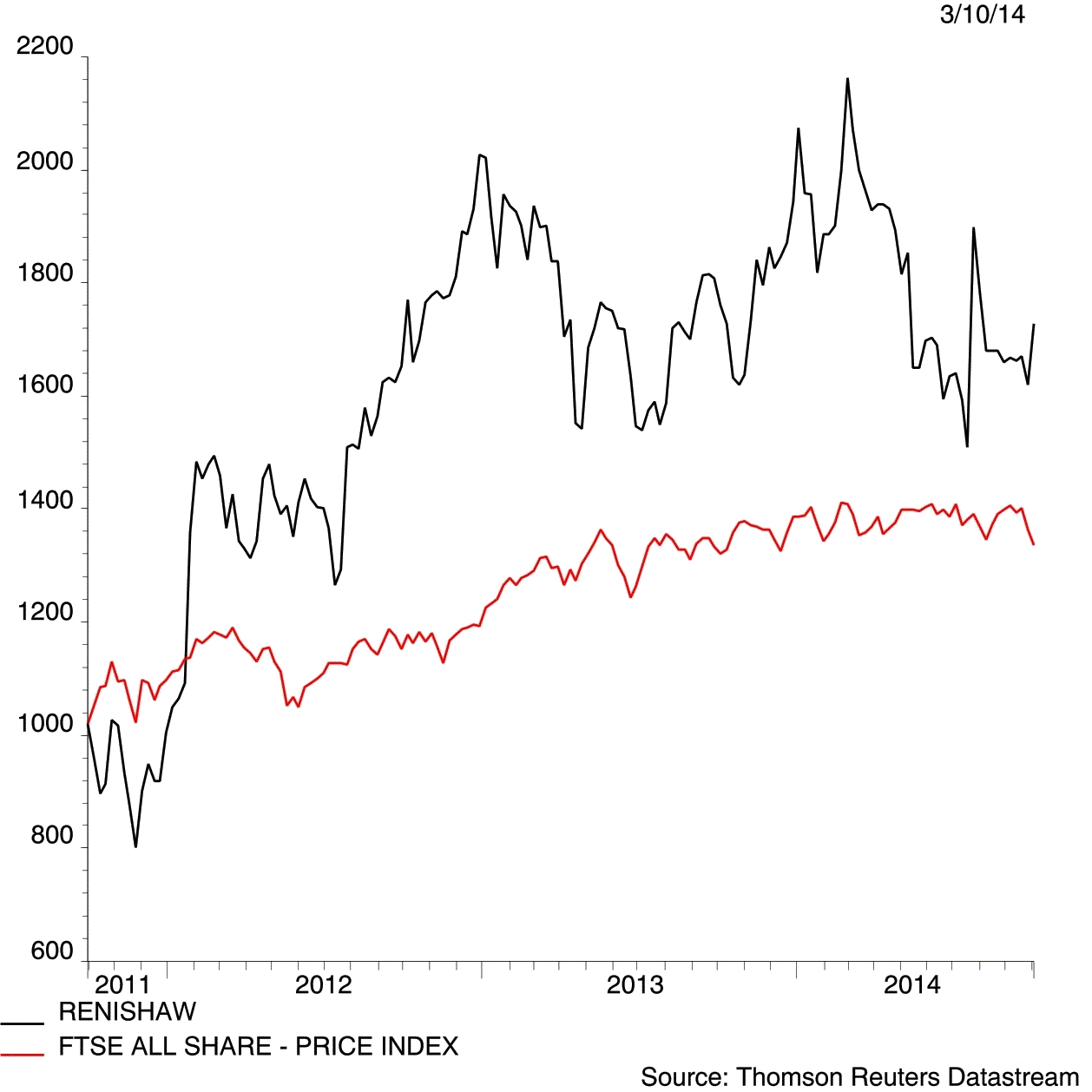

Renishaw (RSW) £31.31

Shares in precision engineer Renishaw (RSW) have been on a roll since December 2016, hitting an all-time high in late March 2017 at £32.42.

We think this is a fantastic business. It deserves a place in an investment portfolio for anyone seeking to own a high-quality company on a long-term basis.

It is a world leader in metrology equipment that monitors and analyses the work of sophisticated cutting tools in factories. Renishaw also has a healthcare division that provides specialist equipment for neurosurgery and dentistry.

It is easy to see why investors have warmed to the stock again after a patchy period clouded by the non-repeat of major contracts in the Far East,

causing some concern about lumpy orders.

The company likes to invest heavily in new products, facilities and people when it spots a growth opportunity. Costs have sometimes risen much faster than sales. That too has been a turn-off for some investors. The problem now seems to have been fixed with revenue now rising faster than costs.

‘Demand for encoding and calibration products is strong, ‘Revo’ 5-axis scanning probes are making inroads with US auto original equipment manufacturers, the new US HQ (with enhanced product demonstration facilities) has opened and healthcare has a strong order book for the second half of the financial year,’ adds Investec. ‘This growth has been achieved in the absence of any one-off large orders.’ (DC)

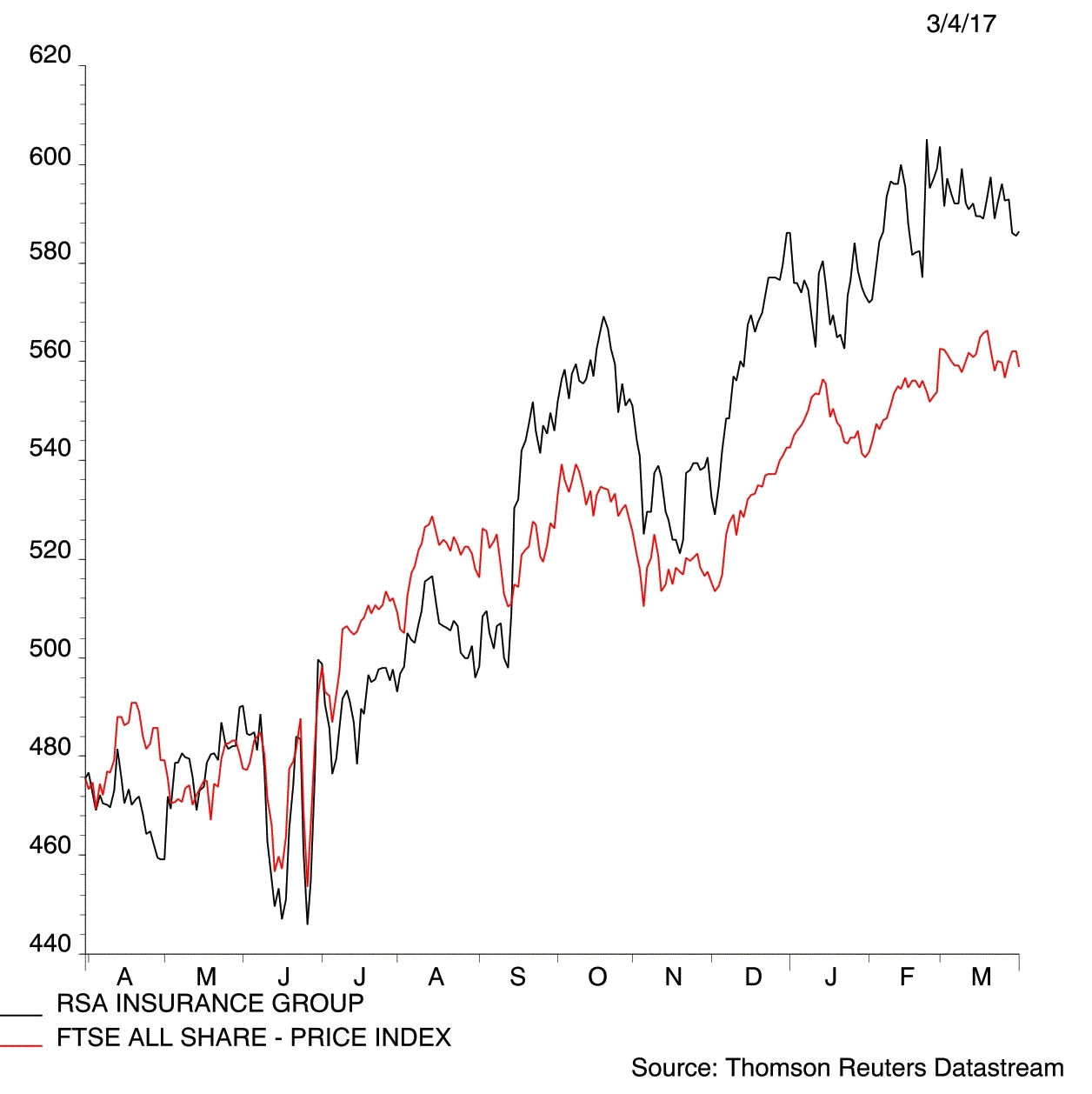

RSA Insurance (RSA) 584p

The man at the top of non-life insurer RSA (RSA), Stephen Hester, may have fallen short in his efforts to turn around troubled bank Royal Bank of Scotland (RBS) but he is enjoying much greater success in his current ‘Mr Fixit’ role.

Results for 2016 came in substantially ahead of expectations, illustrating how RSA is on a winning streak. Investors have been rewarded with 20%+ share price gains in the past 12 months and there could be much more to come, according to investment bank Morgan Stanley.

It believes RSA’s share price could reach 650p over the next year, helped by an improved balance sheet feeding into ‘a strong capital return’.

Group operating profit in 2016 was up by a quarter to £655m and ahead of the consensus forecast of £626m. The combined operating ratio, which measures the performance of its underwriting business, came in at 94.2%. Anything below 100% implies a profit.

A deal to dispose of £834m worth of legacy insurance liabilities in the UK is being well received and simplifies the investment case.

Hester and his team are bullish on the outlook, hiking the full year dividend by 52%, raising the return on assets target from 12%-15% to 13%-17% and pledging that in performance terms ‘the future can be brighter still’. (TS)

RECOVERY STOCKS: THE COMEBACK KIDS

Telecom Plus (TEP) £12.00

The stock market has been a fickle master for the past three years but Telecom Plus (TEP) remains a true quality company, in our view.

The multi-utility supplier remains a unique play on customer expansion thanks to a scalable platform, low capital cost requirements, high recurring revenues and improving earnings quality and visibility.

Trading as Utility Warehouse, the company typically starts supplying gas and electricity to customers. It then progresses to cross-selling home phone, broadband and mobile calls, texts and data, offering its ‘members’ access to cheaper third party goods and services via its discount card.

This year should see Telecom Plus add insurance (home, car, travel, etc) and water, with the latter being opened up to competition by its Ofwat regulator. This could help to make customers even more sticky and valuable.

Energy tariff price hikes make the big six suppliers increasingly unpopular while many smaller independents are being squeezed by unhedged rising wholesale costs, putting Telecom Plus in prime position to pinch customers.

To date it has only got a 1.5% share of an estimated £40bn UK energy market, leaving plenty of room to grow. The cost of deepening its claws into UK households is capped surprisingly low thanks to its word-of-mouth distribution model. (SF)

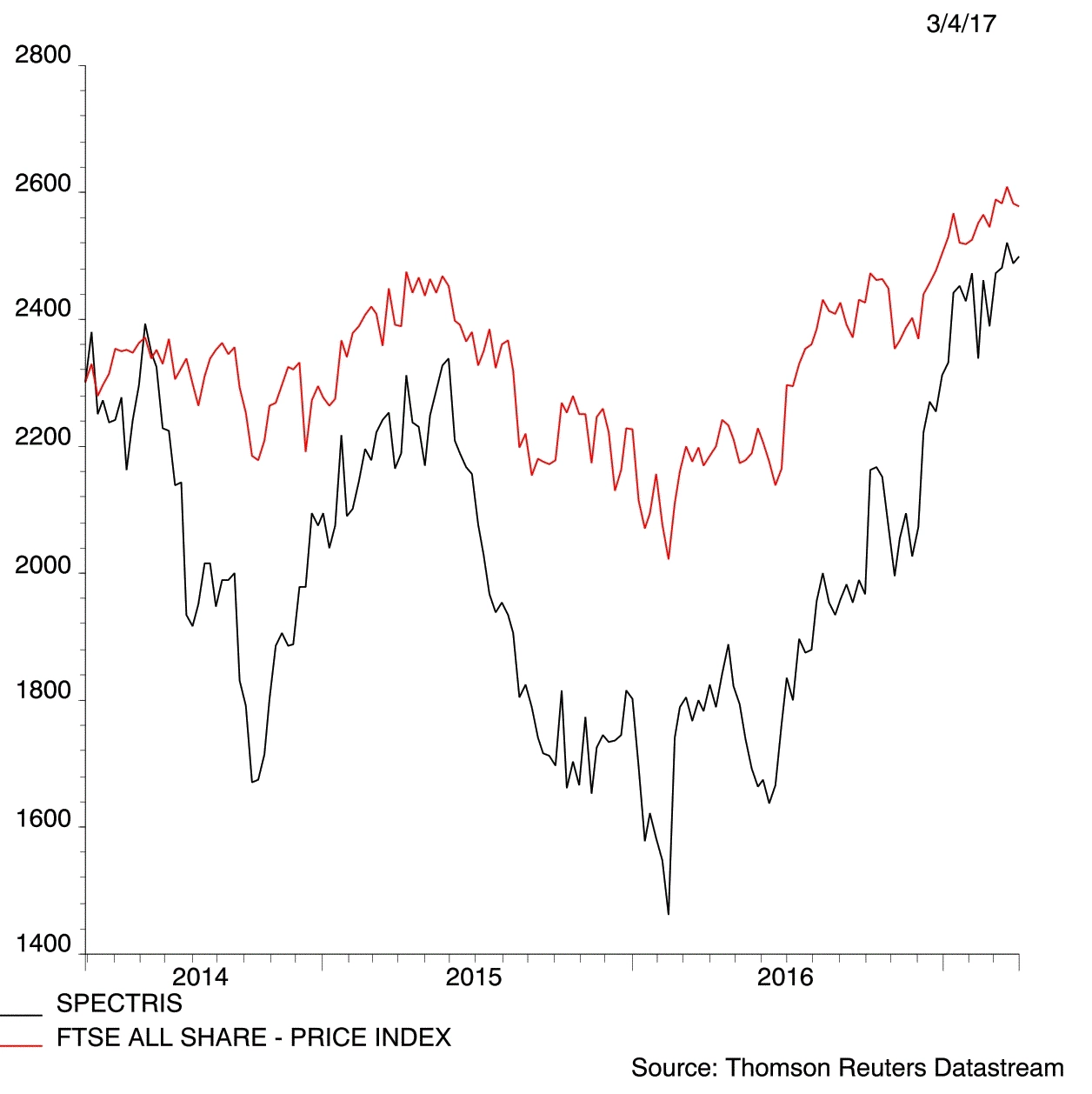

Spectris (SXS) £24.88

Egham-based Spectris (SXS) supplies the sort of labour saving, productivity aiding instrumentation and controls used by manufacturers around the world. Sales have been stagnant for many years, but analysts now predict a brighter future.

Investec believes there is good potential share price upside for anyone prepared to wait. In February it said: ‘Prospects of sales growth are welcome, after several years of flat (or worse) momentum.’ Shore Capital says the shares could keep rising if Spectris meets its cost saving goals and there is further improvement in its end markets.

The bulk of last year’s £1.35bn of sales come from slower-burning developed economies, such as North America, Europe and Japan, where capital investment has been stuck in a rut for the past few years.

Expansion across emerging markets in Latin America, China and Asia Pacific is now becoming increasingly important.

New product lines should also support growth expectations, thanks to Spectris’ ongoing commitment to research and development.

The £3bn company remains cautious on its near-term future but analysts seem reasonably confident of ongoing progress, with ‘buy’ ratings from eight of 15 analysts who cover the stock.

Spectris is a fine and innovative British company with years of experience and expertise. Management deserve credit for pulling the right levers during a challenging spell over which it has had little control, a point reflected in the 24% share rally over the past six months. (SF)

HIGHER-RISK STOCKS: FOR THE MORE ADVENTUROUS INVESTOR

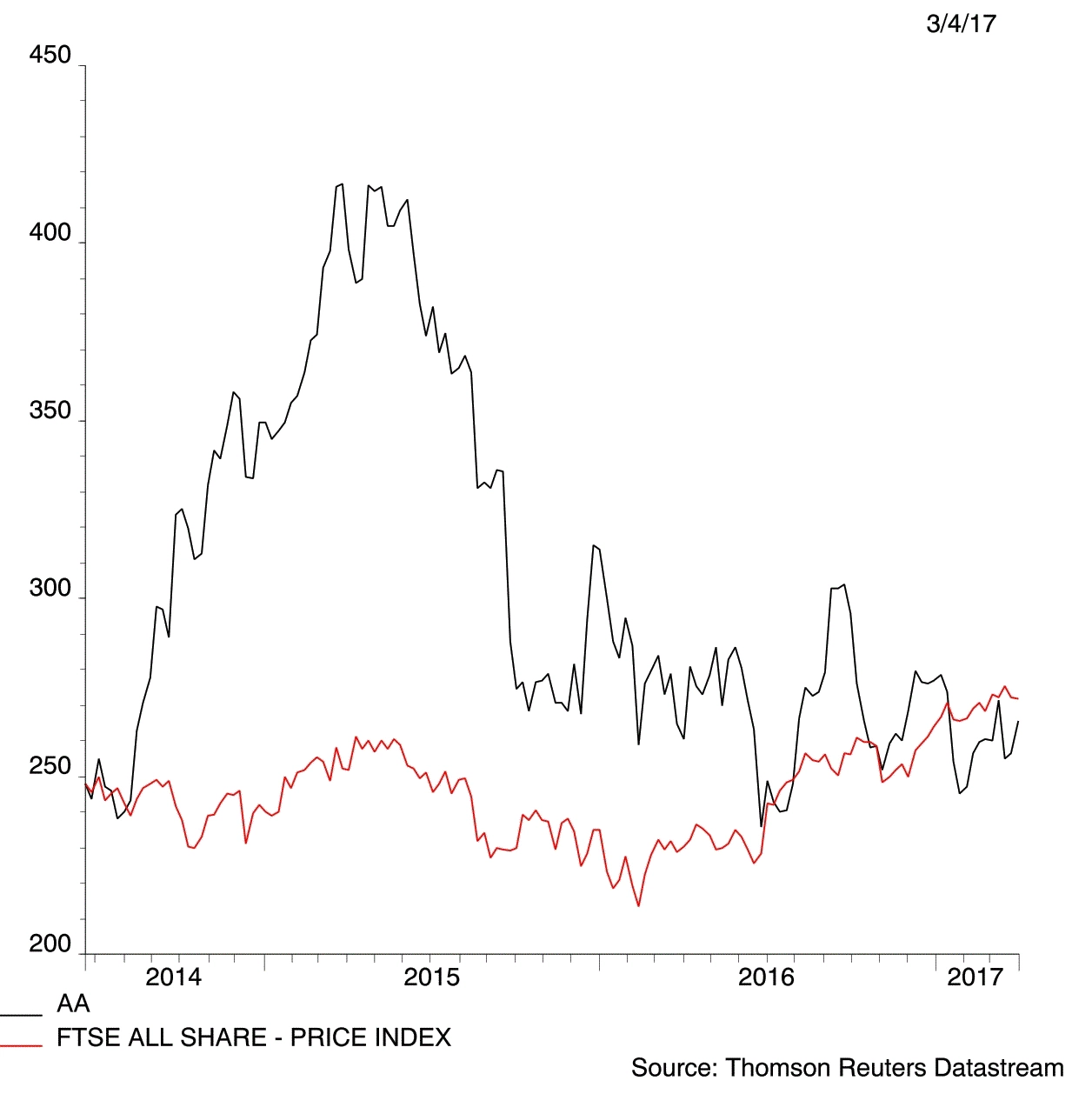

AA (AA.) 264.7p

Although AA (AA.) is best known for its road side assistance business, the £1.6bn cap also generates revenue from insurance services and driving instruction.

We believe it could be a good stock over the long-term as its strong cash flow is dependable enough in our view to keep reducing borrowings. Net debt stood at £2.62bn as of 31 January 2017 which is about 1.6 times its market cap.

A new IT system is helping to deliver costs savings with more efficient processing, among many other areas. A new customer relationship management system should be ready to support more personalised and targeted marketing from Autumn 2017 when all the data is fully uploaded.

The company has finally halted its decline in membership due in part to the higher adoption of its phone app. It has also launched ‘Car Genie’ which spots issues with a car before they arise and allows them to be fixed before a breakdown occurs.

The AA wants to be seen as a business which helps drivers across the board – not necessarily just saves them after a breakdown.

Liberum says longer term concerns about the outlook for the roadside market have been overstated. Many people suggest electric vehicles – which are becoming more popular – are more reliable, so there is less need to use the AA’s services. ‘The biggest cause of breakdowns for the AA is batteries and wheels; electric and self-drive vehicles have both,’ says the investment bank. (DC/DS)

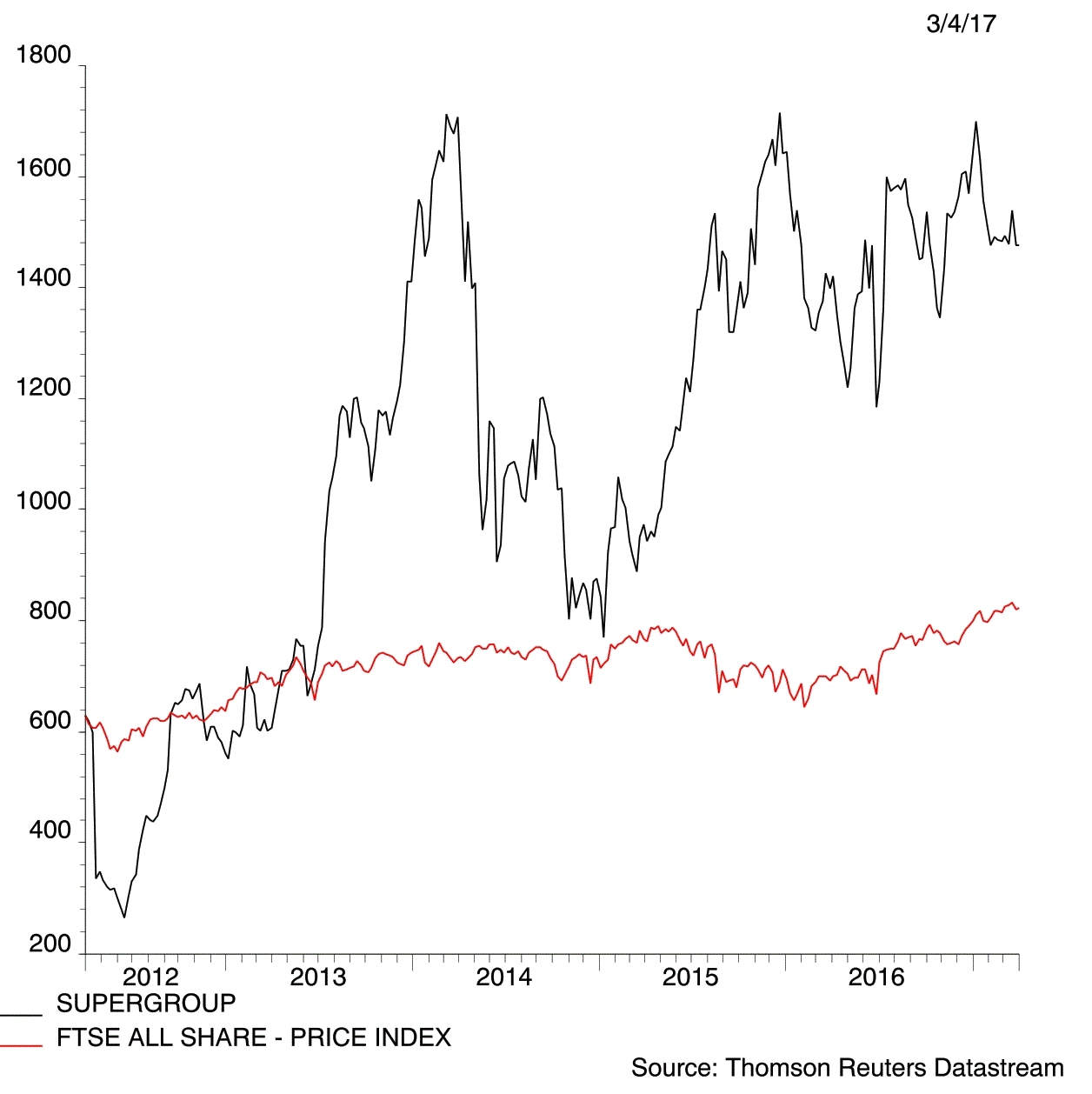

SuperGroup (SGP) £14.59

Risk-tolerant investors wanting exposure to an international growth story may find multi-channel fashion retailer SuperGroup (SGP) appealing, according to bullish comments from Panmure Gordon analyst Michael Stewart.

He claims SuperGroup is one of the most undervalued global brand roll-out stories within the UK retail sector. He believes the market is not fully appreciating SuperGroup’s best-in-class revenue growth and profit margins.

The analyst is confident the shares could hit just shy of £19 over the next year.

Admittedly we have a very cautious view towards the UK retail industry at present, in light of rising inflation and our forecast for a drop in consumer confidence levels. SuperGroup is a bit different as the growth story is focused overseas, accounting for more than half its sales. That said, we would class this stock as one for a more adventurous investor because of the near-term risk to the UK proportion of sales due to tough market conditions.

Growing its store portfolio at a steady clip in Europe, SuperGroup is progressing in North America and has a promising joint venture in China.

For the year to April 2017, Stewart forecasts a pre-tax profit jump to £83.5m (2016: £72.4m) and a 27.3p dividend, rising to £96m and 31.4p respectively by April 2018. (JC)

TOP QUALITY FIRMS: ESSENTIAL STOCKS TO OWN

Halma (HLMA) £10.25

FTSE 250 member Halma (HLMA) is an excellent example of a high quality business that would sit well in an ISA portfolio.

It is a global manufacturer and supplier of health, safety and environmental equipment typically designed to meet the ever-widening regulations net. Halma should, theoretically, see revenue and profit growth whatever the economic weather.

For that reason, we believe it is the sort of share that can be tucked away and largely forgotten about. That’s ideal for medium to longer-term investors.

Organic growth is bolstered by carefully selected, bolt-on acquisitions.

Halma typically looks for strong returns from resilient growth drivers based on advances in safety regulations, ageing and urbanising populations, and other demographic trends.

The impressive formula works. It creates a virtuous circle of reliable growth and cash generation that pays for the next stage of investment. Operating margins have been reliably maintained in the low-20% range for many years.

There is incrementally more surplus cash to pass on to shareholders. We note that Halma has increased the dividend by more than 5% every year since 1979; a staggering achievement that feeds superior returns of compounding growth stories.

Don’t be put off by its premium equity valuation of 23 times forecast earnings for 2018. It has consistently been an expensive share – yet it consistently rewards shareholders with tasty dividends and has an excellent track record of capital appreciation. The share price has increased by 355% over the past 10 years. (SF)

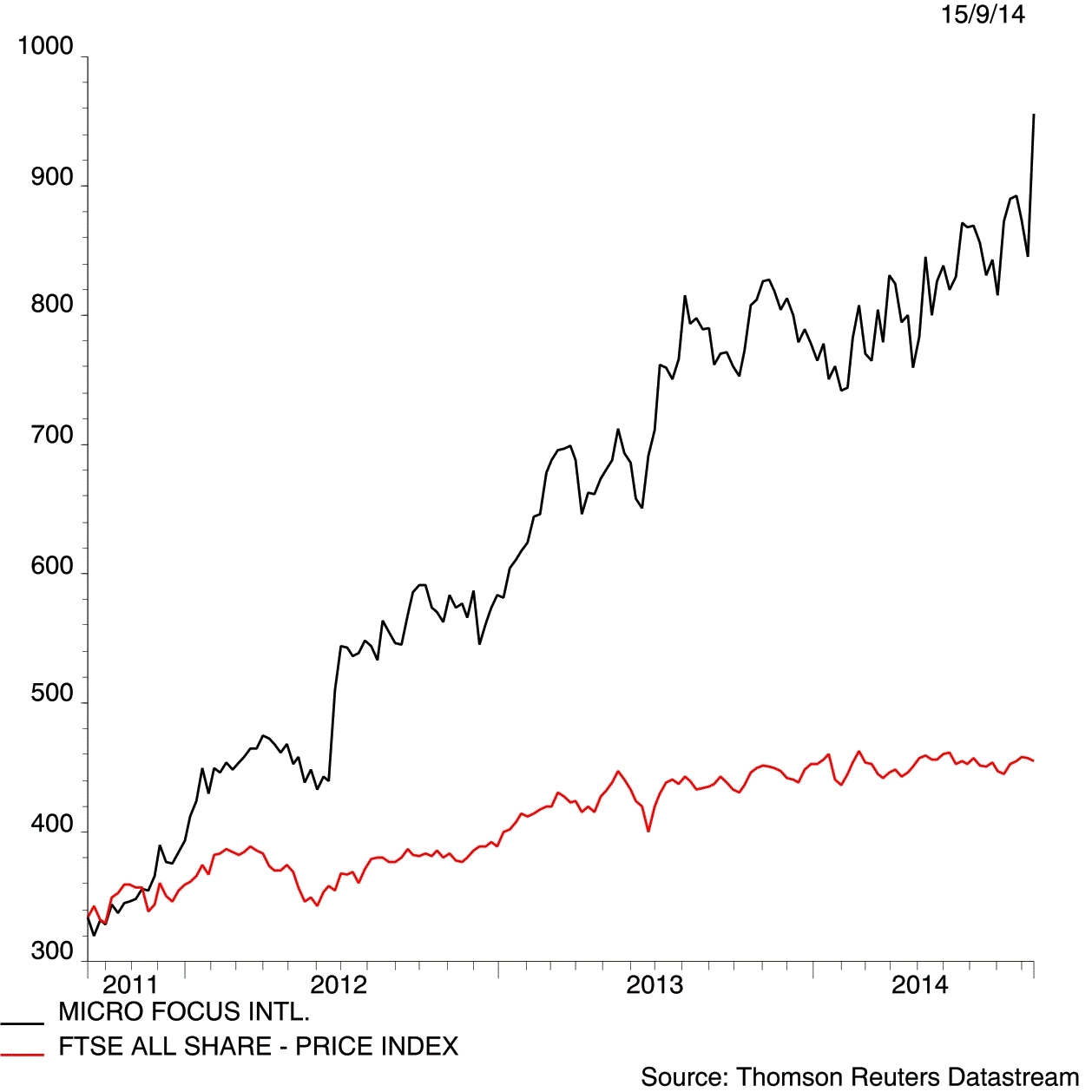

Micro Focus (MCRO) £23.50

Micro Focus’ (MCRO) key attractions are cash generation and its total shareholder return track record, says Stifel analyst George O’Connor. Its applications help companies bring together existing IT and emerging technologies, as well as bridging the gap between old and new IT innovation trends.

Its latest deal, the $8.8bn merger with software assets of US IT group Hewlett Packard Enterprise, will make Micro Focus one of the world’s largest software providers. The deal is expected to complete in September this year.

‘This slick, efficient operating company represents a rare opportunity to invest in a private equity dynamic around restructuring gains, cash generation and cash returns,’ says O’Connor. ‘Merging with HPE Software helps Micro Focus to super-size its model – making it more appealing to a broader investor audience.’

We calculate that £5,000 invested in Micro Focus shares 10 years ago would now be worth £66,217, if you had reinvested all your dividends.

Micro Focus is the market leader for COBOL development and deployment tools. COBOL is a computer programming language designed for business use. It is also involved with software testing, data centre solutions and security management among many other business lines.

Highly cash generative, Micro Focus also has a long history of recycling surplus cash back to investors, via ordinary dividends and special payments. A 91.5c forecast dividend for the year to April 2018 equates to a prospective 3.1% yield.

Shares has written about Micro Focus on many occasions, first flagging the stock back in 2011 at 313p. Stifel has a ‘buy’ rating on the stock and believes the company’s involvement in the mergers and acquisitions space has further to run. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Special dividend on cards for Central Asia Metals?

- FTSE 100 dividend delight on overseas earnings boost

- Margin pressure hits ASOS

- Polar Capital makes a mint after Miton raid

- Brace yourself for more British takeovers

- CityFibre seeks fresh funding deal

- Sophos shines and shares at record high

- Genus gets green light to launch GSS