Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTake a taste of Diageo

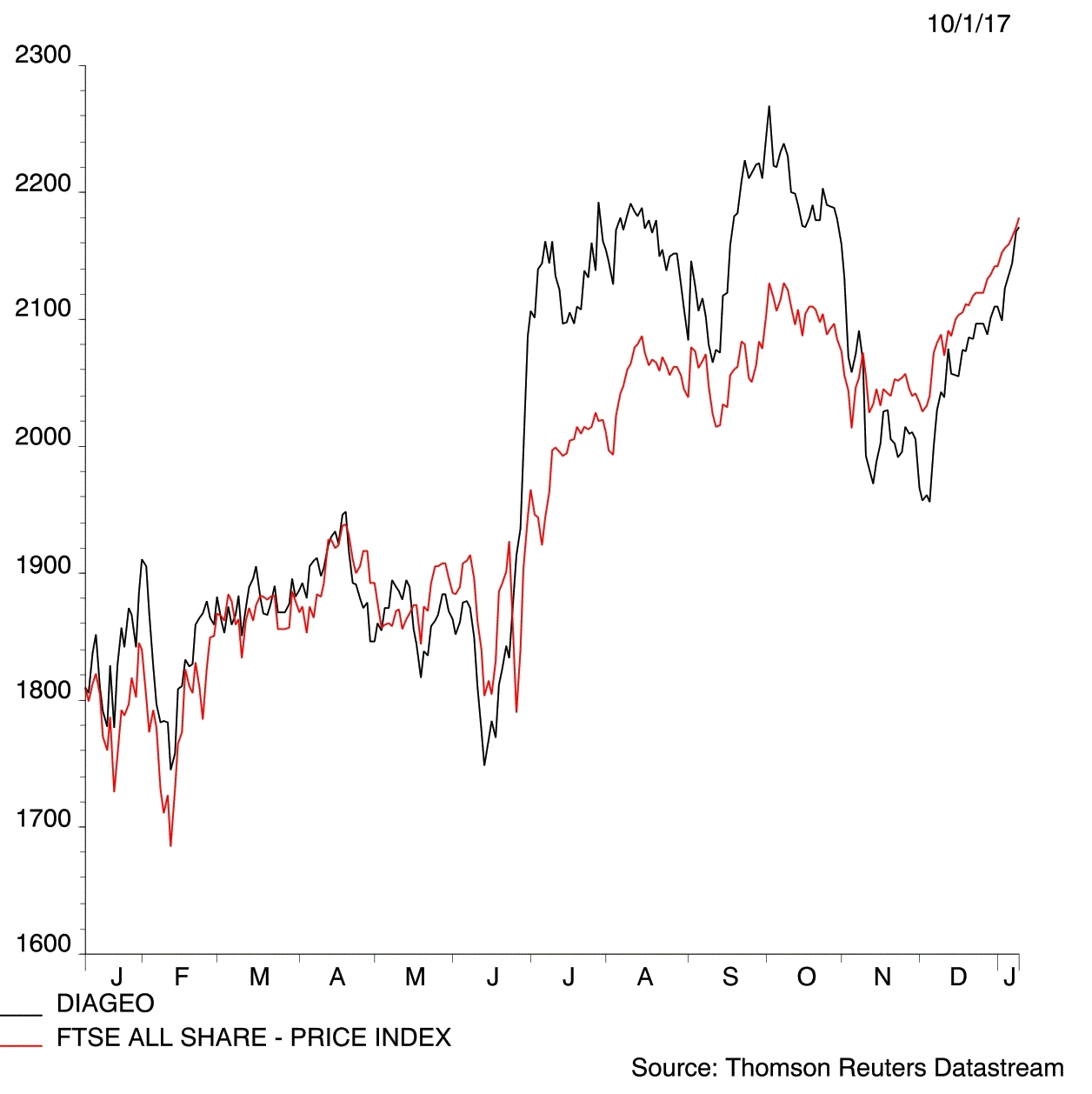

Alcoholic drinks giant Diageo’s (DGE) recent hangover is beginning to fade and the rebound in the world’s largest spirits company has further to run. A winner in the wake of the Brexit vote, Diageo then suffered during a rotation out of expensive defensives into cyclical businesses towards the end of 2016.

Yet investors are again gravitating towards the dependable earnings and cash flows of a global spirits giant selling into 180 countries plus and boasting sales growth and margin enhancement possibilities.

Reassuring tipple

Strong brands are at the heart of the economic moat of Diageo, a high-quality company whose outstanding portfolio spans global brands such as Johnnie Walker whisky, Smirnoff vodka and beloved stout Guinness, as well as local brands including Ypioca in Brazil and ShuiJingFang in China. These brands engender loyalty among consumers, confer pricing power upon Diageo and represent a high, costly entry barrier for its would-be rivals.

Amid prevailing geopolitical uncertainty, its worth remembering Diageo’s earnings are geographically diversified and free cash flow generation strong – up £134m to £2.1bn in the year to June – supporting investment in competitive advantage, acquisitions and a progressive dividend.

Top line drivers

Spirits companies are rebounding from weak results served up in recent years, with China beginning to grow again and Diageo’s US business back in growth. In September, CEO Ivan Menezes flagged a good start to the financial year to June 2017, highlighting three key top line growth drivers as scotch, the US spirits business and India. He also assured the business is on track to meet medium term guidance of 4-6% organic sales growth with margin improvement.

Diageo is also among the beneficiaries of sterling weakness, which not only provides a translation benefit, but also a transaction tailwind by making its scotch more competitive. Long-term, the £54.6bn cap offers a play on the ‘premiumisation’ trend in emerging markets. Uncertain times have seen select emerging market consumers trading down, but the burgeoning ranks of the middle class in the developing world will increasingly aspire to drink premium brands.

One negative for new investors is valuation. For the year to June 2017, Liberum forecasts growth in pre-tax profit to almost £3.46bn (2016: £2.9bn) for earnings of 103p and a 61p dividend, rising to £3.66bn, 109p of EPS and a 64.6p shareholder reward thereafter. On current year estimates, a prospective price-to-earnings (PE) ratio of 21.1 appears frothy, although it is a price worth paying for a high-quality holding and there’s a sustainable yield of 2.8% on offer too. (JC)

Diageo (DGE) £21.73

Stop loss: £17.38

Market value: £54.6bn

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.