Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

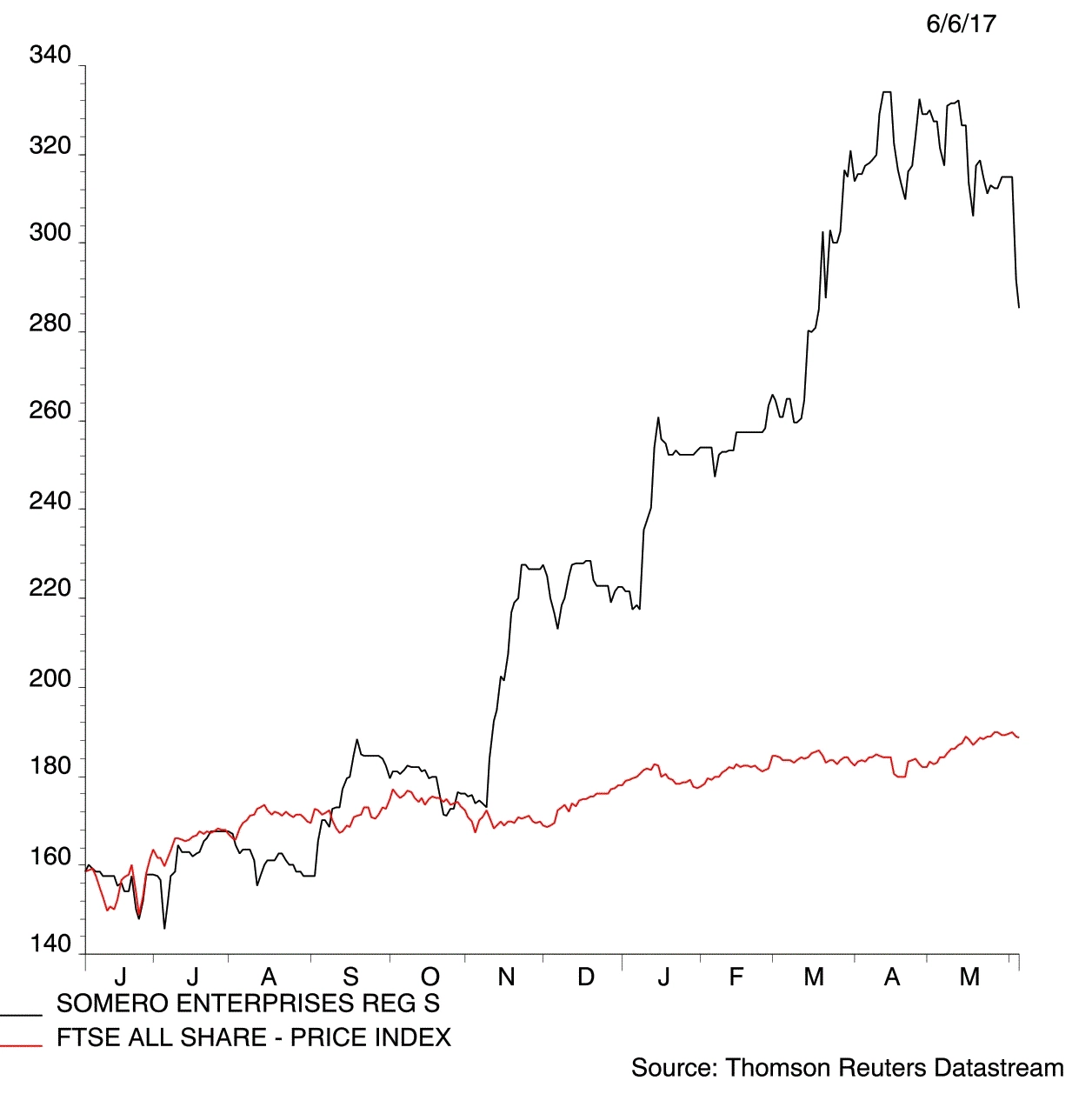

magazineSomero smashes expectations and boosts dividend

Somero Enterprises (SOM:AIM) 232.5p

Gain to date: 68.5%

Original entry point: Buy at 138p, 14 January 2016

The US-focused specialist machinery manufacturer has issued a very positive trading update for its financial year ending 31 December 2016. Revenue, earnings before interest, tax, depreciation and amortisation (EBITDA) and net cash are all expected to be ahead of market forecasts.

The company is so confident about the health of its trading that it will start to pay a greater percentage of earnings in dividends to shareholders. The payout ratio is moving from 30% to 40% of adjusted net income.

Its net cash level is also above the $10m target, so it has hinted at paying a special dividend in 2017. That will depend on requirements for current business needs and future investment in the first half of the year.

Broker FinnCap has upgraded its 2017 pre-tax profit forecast by 6.4% to $23.3m and reckons its will report $21.8m for 2016. Its price target for the next 12 months has been lifted from 217.5p to 254p.

We tipped this stock a year ago and it has since risen by 68.5%; a superb result. We remain big fans of the company as the stock isn’t overly expensive and there is a supportive backdrop amid implications that Trump wants to bring manufacturing back to the US. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.