Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGear4music in the groove

Online musical instruments retailer Gear4music (G4M:AIM) earned yet another round of earnings upgrades following its trading update (6 Jan). We remain bullish, with a premium valuation justified by the growth potential.

Shares has been excited about York-headquartered Gear4music since its IPO (3 June ‘15) and urged investors to buy at 150p – see Small Caps, 11 Aug 16 – this summer. We correctly identified Gear4music’s attractions as a structural retail winner and status as a Brexit-busting growth stock.

Round of upgrades

Triggering another round of upgrades following the Brexit vote in June, the latest excellent update showed sales up 55% to almost £24.4m in the four months to December and improved gross margin, reflecting market share gains in the UK and Europe as well as stellar 63% growth in higher margin own-label sales.

Particularly impressive was the 130% surge in Europe and Rest of the World sales to nearly £9.4m – UK revenues rose 29% to £15m – while active customer numbers have grown 53% to 324,000.

Guided by CEO Andrew Wass, the £104.6m cap is tapping into the profound distribution shift towards selling instruments and equipment online. Keenly priced products, fast and flexible delivery options and best in class customer service are competitive strengths.

Selling own-brand instruments and premium third party brands including Fender, Yamaha and Roland, Gear4music is at the foothills of growth in a fragmented market. The fall in the pound is also boosting European exports, Gear4music reaping the benefits of investment in multi-lingual, multi-currency websites.

Significantly, a Swedish distribution centre is already operational and a German one will be up and running before the end of February. These hubs will help power rapid growth on the continent, not only reducing customer delivery times but also providing local buying opportunities.

Rich rating

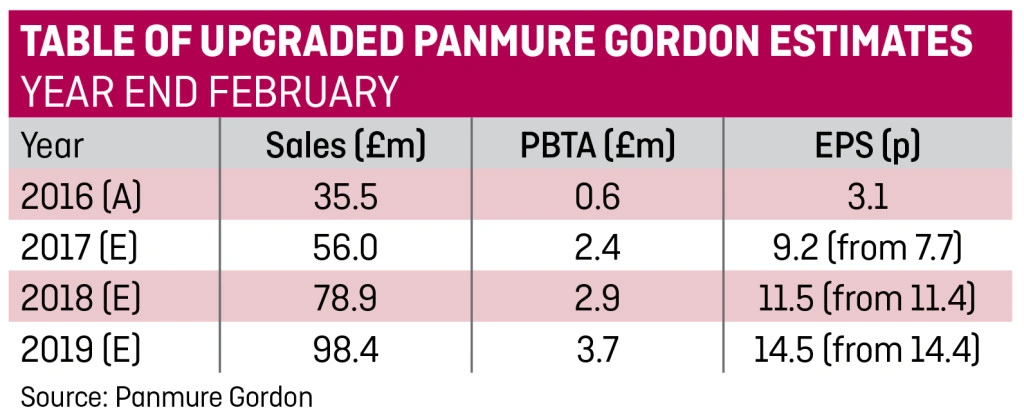

Panmure Gordon’s Peter Smedley has upgraded his pre-tax profit forecast for the year to February by 20% to £2.4m, building on a 21% upgrade as recently as October, and upped his earnings estimate from 7.7p to 9.2p, forecasts which leave Gear4music on a rich forward earnings multiple of 56 times plus.

Raising his price target from £4 to £6, Smedley prudently leaves his £2.9m 2018 pre-tax profit estimate unchanged to reflect investment in infrastructure and products to drive growth, which will constrain short term profit upside. However, given the overseas growth Gear4music is delivering, we believe this estimate could prove conservative.

We’re staying bullish on Gear4music at 519p for its structural growth attractions and note 15.6% upside to Panmure’s price target.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.