Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy small cap funds give you extra

Small cap fund managers typically enjoy the privilege of being able to meet company bosses on a regular basis. They get a chance to sit down and properly understand the businesses’ risks and opportunities.

This can provide valuable information on which to base investment decisions – not just the initial purchase of shares but also to reassess the investment case as time goes on.

Unicorn Asset Management fund manager Simon Moon says meeting management teams is a ‘hugely important’ part of his investment process. ‘It’s highly unlikely we’ll invest prior to meeting a team,’ he adds.

Retail investors – namely the general public – rarely have the luxury of spending quality time with plc bosses. They are often limited to the information provided in company announcements and the occasional video interview on a company’s website.

Investing in small cap funds can therefore give retail investors access to that investment edge possessed by fund managers.

In the second of our two-part series, we look at three more small cap funds (in addition to the three funds we featured last week) and explain their attractions from an investment perspective.

Quality leadership

The quality of leadership arguably has a far greater influence in the relative success, or not, of a smaller company than a multi-billion dollar business which has lots of managers.

That’s a key reason why Katen Patel, who runs the JP Morgan UK Smaller Companies Fund (GB0030880255) alongside colleague Georgina Brittain, meets a lot of management teams.

‘We are making sure that the management is strong and is disciplined with its funds,’ he says. ‘We like cash generating companies with healthy balance sheets.’

One of the chief stock selection criteria he uses is making sure that earnings growth can be repeated year after year. When he identifies a track record for ‘sustainable earnings progression’ it can lead to a long-term relationship with the company since ‘we like to run our winners,’ Patel explains.

Patel tends to steer clear of certain types of company. He’s not a huge fan of biotech, for example, which can often be ‘three or more years away from real revenues’ and sometimes even longer before they make a profit.

His investment style will chime with many investors that favour a more risk-averse policy.

Patel has also noted the distinct change in demand for dividends. Many small companies are not noted for paying cash rewards to shareholders. They are often early in their growth curve where surplus cash can be better used to fund expansion.

Equally, he thinks companies themselves are more aware of the investor appetite for dividends. There is a risk that firms pay dividends to lure investors when in fact that’s not the best use of their money.

Global coverage

Another small cap surprise, in some cases, is their worldwide reach. ‘A lot of smaller companies are more global than you might expect.’ he says.

Patel cites infrastructure engineer Hill & Smith (HILS) as a good example, hence why he’s been building his fund’s stake recently.

The business is growing both in the UK and overseas, and is pitched as a possible winner from extra infrastructure spending anticipated under Donald Trump’s presidency.

Patel has been buying more shares in promotional products manufacturer 4imprint (FOUR) and housebuilder MJ Gleeson (GLE).

A newish name to the fund’s portfolio is Quarto (QRT), which publishes coffee table-style books. ‘It got in new management three years ago who are turning the business round, yet it still trades on a PE (price to earnings ratio) of six, with a 4% dividend yield,’ Patel states.

Grab the market’s new names

Early access to IPOs (initial public offerings) is another reason why some investors will choose the funds route rather than waiting to buy the stock directly.

‘We have unprecedented access to management and in-house experts,’ the fund manager says.

In August his fund participated in the £26.6m fund raising of sound proofing materials designer Autins (AUTG:AIM) with Patel particularly noting its ‘great visibility’. The shares are up 37% in value since the stock market float.

A month later Patel and his team took a stake in Hollywood Bowl (BOWL), the bowling alley operator.

Structural growth drivers

Henderson fund manager Neil Hermon looks for companies with structural growth drivers. ‘(I seek) ‘long-term underlying trends – for example changing demographics, over-arching governmental policies, or technological innovations – drive revenues and enable businesses to grow regardless of what’s going on in the wider economy.’

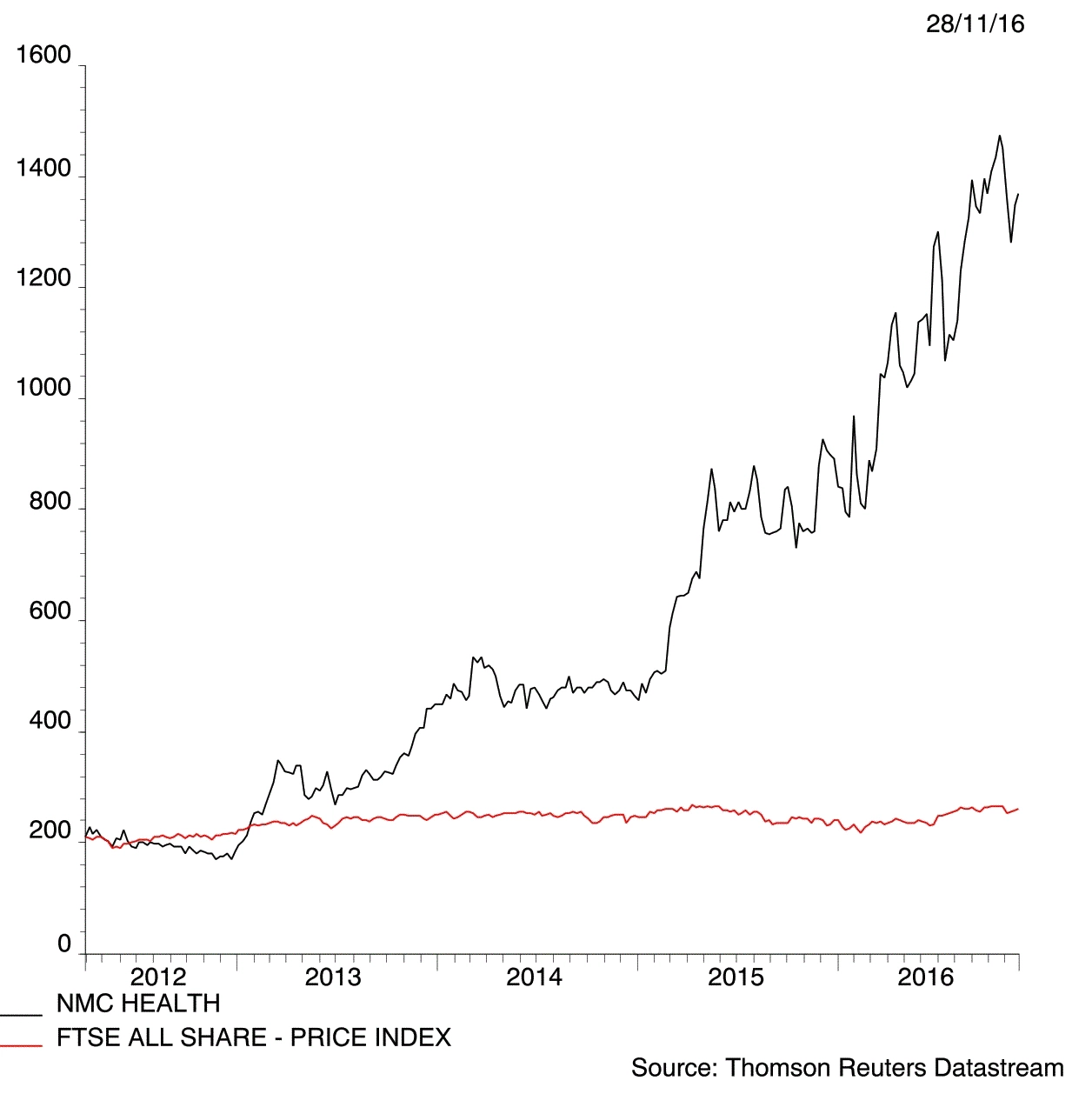

Hermon manages Henderson Smaller Companies Investment Trust (HSL). One holding that fits the bill for structural trends is Middle East hospitals company NMC Health (NMC).

Admittedly NMC is now a mid-cap stock worth £2.5bn rather than a smaller company as its market value has increased sevenfold in the past four and a half years. However, that performance shows the potential gains to be made if you the pick the right stock.

‘Small and mid-size companies – where we focus our attention – serve to further enhance exposure to the underlying structural growth trends.

‘Their inherently small, nimble, ambitious management teams, unencumbered by red tape or giant operations, are able to seek-out new markets, launch new products or services, or look at new ventures overseas; ultimately, to build sales rapidly and tap into the trends that underpin the business’ success,’ says Hermon.

‘Growth investing is inherently risky; a delicate and volatile balance exists between top-line growth and share price performance. Increasing the reliability of revenues by gaining exposure to long-term structural trends strategically aims to mitigate some of these risks, and by looking at smaller companies to seek out these opportunities the exposure to these trends is only further concentrated.’

Niche preference

Simon Moon, manager of Unicorn UK Smaller Companies (GB0031791238) likes stocks that are profitable, generate cash and operate in niche areas of their chosen end markets.

‘Companies at the smaller end of the market capitalisation spectrum don’t tend to be as well covered by brokerage houses and as such don’t have exhaustive earnings estimate consensus, as such we feel that by putting in the ‘leg-work’ we’re often able to uncover some ‘hidden gems’ that are underappreciated by the market.’

Somero Enterprise (SOM:AIM) is the largest position in his portfolio. The AIM-quoted manufacturer of specialist concrete levelling machinery has seen its share price nearly double in the past year.

‘The machinery increases the efficiency and productivity of a build site and is attractive compared to the manual alternative. The company is attractively valued, pays a well-covered dividend,’ says Moon.

‘It is exposed to markets which are being driven by significantly increasing infrastructure spending and as such is growing revenues and profits strongly. The international nature of the business means it’s also a beneficiary of the strengthening US dollar.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.