Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHitch a ride with Vietnam funds

Vietnam is one of the world’s fastest growing markets. The emerging economy is based on growing manufacturing prowess, a reducing reliance on commodity and extractive industries and a shift towards consumption.

This frontier market has an attractive growth profile, having generated GDP growth of 6.7% in 2015 powered by a young, well-educated and growing workforce.

Average GDP growth over the past 20 years has exceeded 7%, which is second only to China according to investment fund Vietnam Holding (VNH).

Vietnam’s 94.3 million strong population is the world’s fifteenth largest with a literacy rate of 94.5%, while a median age of 29.6 years means Vietnam benefits from a ‘demographic dividend’.

If you are looking for ideas to diversify your portfolio, the investment case for Vietnam is undeniably attractive, in our opinion. There are several funds available to UK investors that provide easy exposure to this country.

Bouncing back

Vietnamese markets are in the midst of a bull run, bouncing back from a torrid 2006-2009, driven by several years of high earnings growth.

Vietnam’s new government appears business friendly and GDP growth of around 6% is forecast this year, slightly lower than anticipated at the start of the year due to the impact of drought on agriculture, though Vietnam has both a trade surplus and reasonable foreign exchange reserves.

Even though the market has already re-rated, Vietnam bulls argue it remains cheap on a relative basis. Vietnamese companies have demonstrated resilient earnings growth in recent years and that ongoing reform in Vietnam is expected to benefit equities, with privatisation and reform of state-owned enterprises remaining on the agenda.

How to get exposure

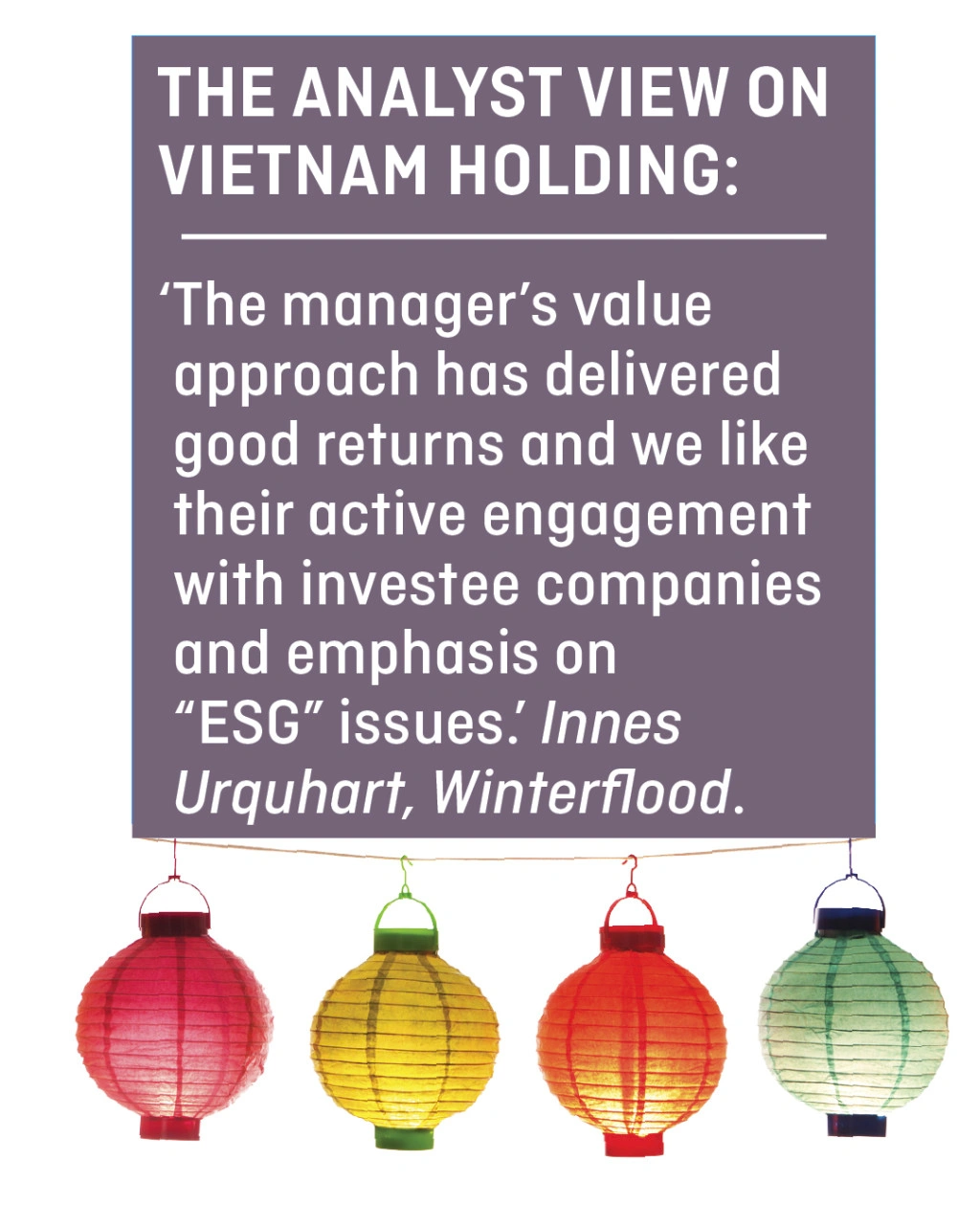

We’ve had our eye on Vietnam Holding for some time, having flagged it at 87c in 2011. Even after surging to $2.26, the fund presently trades at a 22% discount to latest estimated net asset value (NAV) of $2.885 per share – something that may entice value investors.

The fund is managed by Vietnam Holding Asset Management and benefits from an experienced team whose local presence represents a competitive advantage.

The manager’s value investment approach has proved highly successful, supported by an active engagement programme with an emphasis on ESG (environmental, social and corporate governance) issues.

In fact, Vietnam Holding’s NAV per share is up 29.26% year-to-date versus 15.88% for the VNAS Index. Over the past five years it has grown 166.88% versus 50.87% for the Vietnam All Share (VNAS) Index.

The fund’s portfolio is biased towards growing mid cap companies and focused on three key themes: domestic consumption, urbanisation and agri-business. ‘Vietnam has reached a level of income per capita where it is more than just about survival,’ says Jean-Christophe Ganz, chairman of the fund’s management company.

‘Vietnam is entering the age of consumption. Two thirds of the population still live in rural areas, but there’s a huge investment effort to provide accommodation, water, schools and education to the population as people migrate to the cities,’ he says.

‘Agri-business used to be 26% of the portfolio, but we realised investments that had reached their maturity stage and we divested them at a premium,’ adds Ganz. ‘We keep companies for a relatively long time if we can and we rebalance.

‘If the valuation becomes really high or an investment has reached maturity, then we will divest. There’s a big dividend culture in Vietnam in general,’ explains Ganz, citing demand for payouts from the retail investors that drive the market, and saying that most companies pay high dividends.

Key holdings include Traphaco, an industry leader in traditional herbal medication and a potential bid target for an overseas pharma company in time. It also has positions in Thien Long, a pens and stationery distributor and strong portfolio performer, as well as Nafoods, which exports fruit puree and juice concentrate to more than 50 countries.

Further selections

Other ways to gain Vietnamese exposure include VinaCapital Vietnam Opportunity (VOF) and Dragon Capital’s Vietnam Enterprise Investments (VEIL), launched over 20 years ago as the first-ever Vietnamese closed-ended fund.

In July 2016, the latter moved from the Irish Stock Exchange to London’s Main Market in a bid to boost liquidity, attract greater investor interest and narrow its discount to NAV, currently 12.7%.

Vietnam Enterprise Investments offers an exposure to the likes of dairy products play Vinamilk, IT and telecommunications leader FPT Corp and also VEAM, a state-own enterprise with stakes in automobile and motorcycle makers via joint ventures with Honda, Toyota and Ford.

Broader exposure

If you aren’t comfortable with having one fund with sole exposure to a single overseas country, an alternative route would be to invest in a broader Asian-themed fund.

For example, BlackRock Frontiers Investment Trust (BRFI) has 6.6% of its holdings in Vietnamese stocks. Baillie Gifford’s Pacific Horizon Investment Trust (PHI) has 4.6% of its portfolio in the country, the fifth largest geographic position after India, Taiwan, Korea and Hong Kong/China.

Don’t presume all Asian-style investment funds will have Vietnam in their portfolio, despite the country’s obvious attractions. For example, Henderson Far East Income (HEFL) has no exposure to the country. ‘We’re not in Vietnam, though the long-term story is a pretty compelling one’, says fund manager Mike Kerley.

He believes the market has already done very well and, with an income mandate in mind, claims dividend yields in Vietnam tend to be derived from riskier sectors including banks. His frontier market preference is Pakistan, currently undergoing an infrastructure boom. ‘It is Vietnam fifteen years ago,’ he claims. ‘The market there is half the multiple of Vietnam and the index yields over 5%.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.