Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEbiquity’s profit margin sacrifice

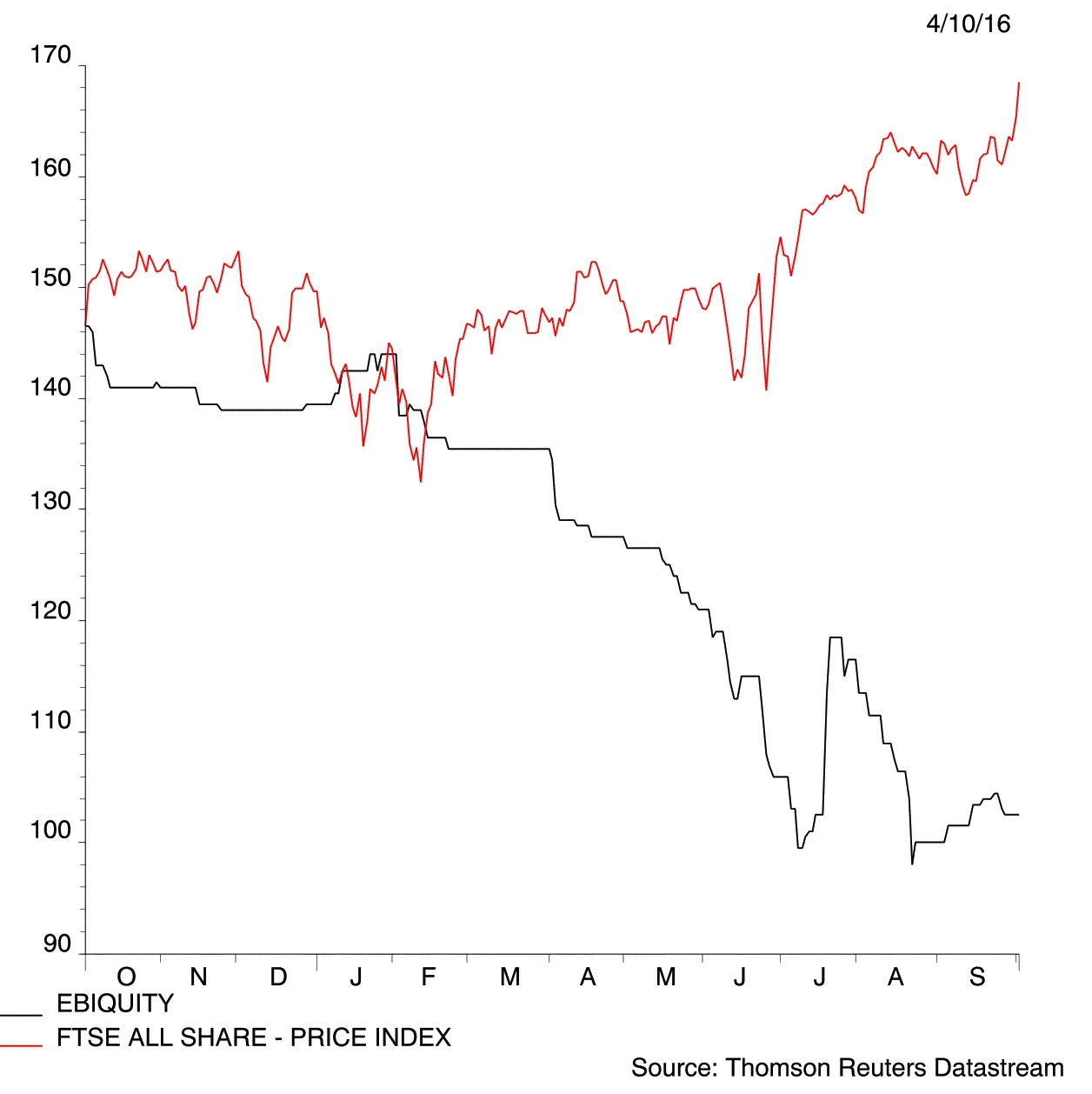

Marketing analytics business Ebiquity (EBQ:AIM) is sacrificing short-term margin performance as it invests for future growth. Earnings are forecast to decline near-term, perhaps explaining why the shares are trading close to a two-year low of 102.5p.

Contrarian investors may wish to consider taking a position now while the shares are depressed. The best time to buy something is when others are fearful, which makes Ebiquity look interesting at present.

The benefits of the company’s investment plan may take time to be realised, but Numis analyst Paul Richards says the plan will leave the group ‘well-positioned to deliver double-digit earnings per share growth’ in the future.

The bulk of the investment is going towards Ebiquity’s Media Value Measurement and Marketing Performance Optimisation divisions. They help companies understand the effectiveness of their marketing and advertising and to make promotions have greater impact in the future.

In the peak year of the investment programme (2018), margins are expected to be around the 12-13% mark versus the current level of 17%.

We like companies that invest for the future and believe the short-term hit to earnings is already reflected in the stock rating. It trades on a mere 10.4 times 2017 forecast earnings. Buy at 102.5p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.