Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLifetime ISA: top investment strategies for your first home or retirement

Putting aside some of your disposable income on a regular basis to build up a deposit on a first home and take that initial step onto the property ladder is something everyone strives for, but did you know the government will give you thousands of pounds for free to do it?

Launched in April 2017, the Lifetime ISA is one of the less well-publicised savings products, but it can get you to that deposit target much quicker than you think.

You don’t have to use it for a deposit – if you hold onto it until you are 60 you can take your money out and supplement your income or your pension.

WHAT IS THE LIFETIME ISA?

The Lifetime ISA is designed to encourage home buyers to build up a deposit for their first flat or house.

To open an account, you must be 18 or over but under 40, and you can pay in up to £4,000 per year as part of your £20,000 annual ISA limit until you are 50.

The government will add a 25% bonus to your savings, up to a maximum of £1,000 per year.

In theory, therefore, if you pay in £4,000 every year from age 18 to age 50 you could get a ‘free’ £32,000 from the government on top of your original savings of £128,000.

Once you turn 50, you can’t pay into your Lifetime ISA or earn the 25% government bonus but your account stays open and earns interest or investment returns. You can hold cash, shares, or a mixture of them, and you get all the usual ISA benefits such as no tax on income and capital gains but there are strict rules on withdrawals.

You can only withdraw money if you are:

– Buying your first home;

– Aged 60 or over;

– Terminally ill with less than 12 months to live.

If you withdraw cash or assets for any other reason, you must pay a 25% charge based on your total pot.

There are also conditions on buying your first home, such as:

– The property must cost £450,000 or less;

– You can’t buy a property until at least 12 months after you make your first payment;

– You must use a conveyancer or solicitor to act for you in the purchase – the ISA provider will pay the funds directly to them;

– You must apply for a mortgage.

If you’re buying together with someone else who also has a Lifetime ISA and it’s a first property for both of you, they can use their savings and government bonus too.

WHY SHOULD I OPEN ONE?

According to the Land Registry, which tracks all housing transactions in the UK, the average price of a house in December last year was £294,000, up 10% on the previous year, so getting on the property ladder is harder for many people.

However, it’s worth pointing out the average is made up of everything from flats, which cost an average of £233,000, to detached houses, which cost an average £463,000.

Also, the data is a mix of prices for first-time buyers and owner-occupiers who are moving home, with the average price for a first-time buyer – who the Lifetime ISA is aimed at – averaging £245,000 against an average of £345,000 for people moving from one house to another.

According to the Nationwide, which tends to be more conservative in its calculations, the average UK house now costs six and a half times the average salary compared with around three times back in the early 1990s and a long-run average of four and a half times.

For first-time buyers, the UK average is about five and a half times their salary, ranging from just over three times in Scotland and the north of England to nine times in London.

In terms of how long it would take the average first-time buyer to get together a 20% deposit, assuming they set aside 15% of their take-home pay each month, those in Scotland and the north of England could have the money ready within six years, but for those wanting to buy in London it could take over 15 years.

In London, the average price of a property was £530,000 in January, around £250,000 above the UK national average and around 18% above the upper limit for purchases using the Lifetime ISA, but that figure includes super-prime properties.

Most housing transactions each month, including in London, are for properties worth £300,000 or less, suggesting there is a liquid market for flats and smaller houses which are likely to appeal to first-time buyers.

For those who have their heart set on living in the capital, prices and deposits will be steep so it makes even more sense to start contributing to a Lifetime ISA and taking advantage of the government bonus as early as possible.

CAN YOU SHOW ME SOME EXAMPLES?

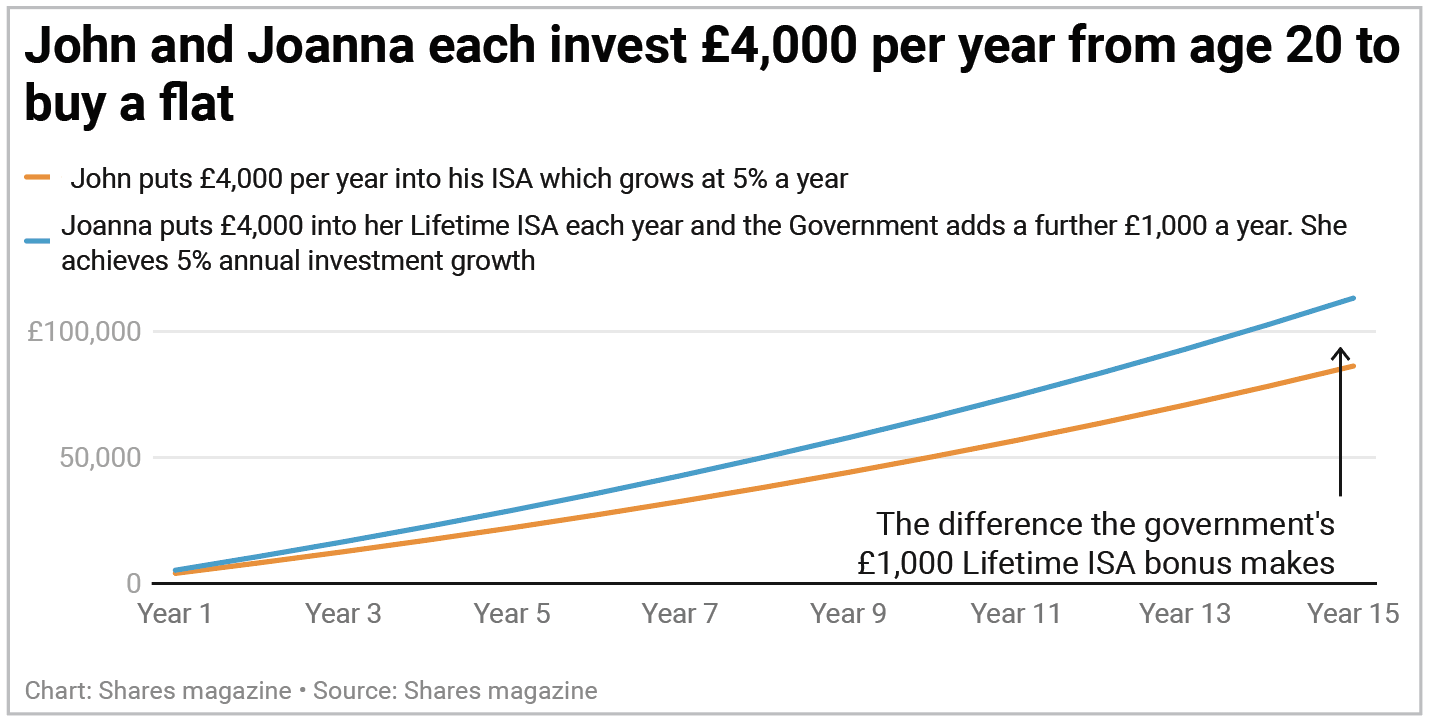

Let’s use the hypothetical example of siblings John and Joanna, who are both 35, and have both been saving £4,000 a year for the last 15 years to put down a deposit on a house.

John has paid £4,000 a year into his ISA, which has grown at 5% per year, while Joanna has paid £4,000 a year into her Lifetime ISA and collected an extra £1,000 free each year, while her capital also grows at 5%.

For illustrative purposes, our calculation assume the Lifetime ISA has been available for 15 years even though it was only launched in 2017.

As the table shows, thanks to the 25% government bonus, Joanna’s savings have compounded at a higher rate than John’s, giving her a deposit of more than £113,000 after 15 years against John’s £86,000.

The difference is much more than the £15,000 extra ‘free’ money which Joanna received and demonstrates why starting early and choosing a Lifetime ISA over a standard ISA makes sense for those saving up for their first home.

WHAT IF I DON’T WANT TO BUY A HOUSE?

One of the great misconceptions about Lifetime ISA’s is they are ‘use it or lose it’ product, like life insurance, and if you don’t buy a house then you are somehow missing out.

Lifetime ISAs are perfect for someone who doesn’t have a lot of disposable income but who wants to save for retirement and is happy to tie their money up for the long term.

You don’t have to start at 18 but you still get the 25% government bonus on whatever you pay in up to £4,000.

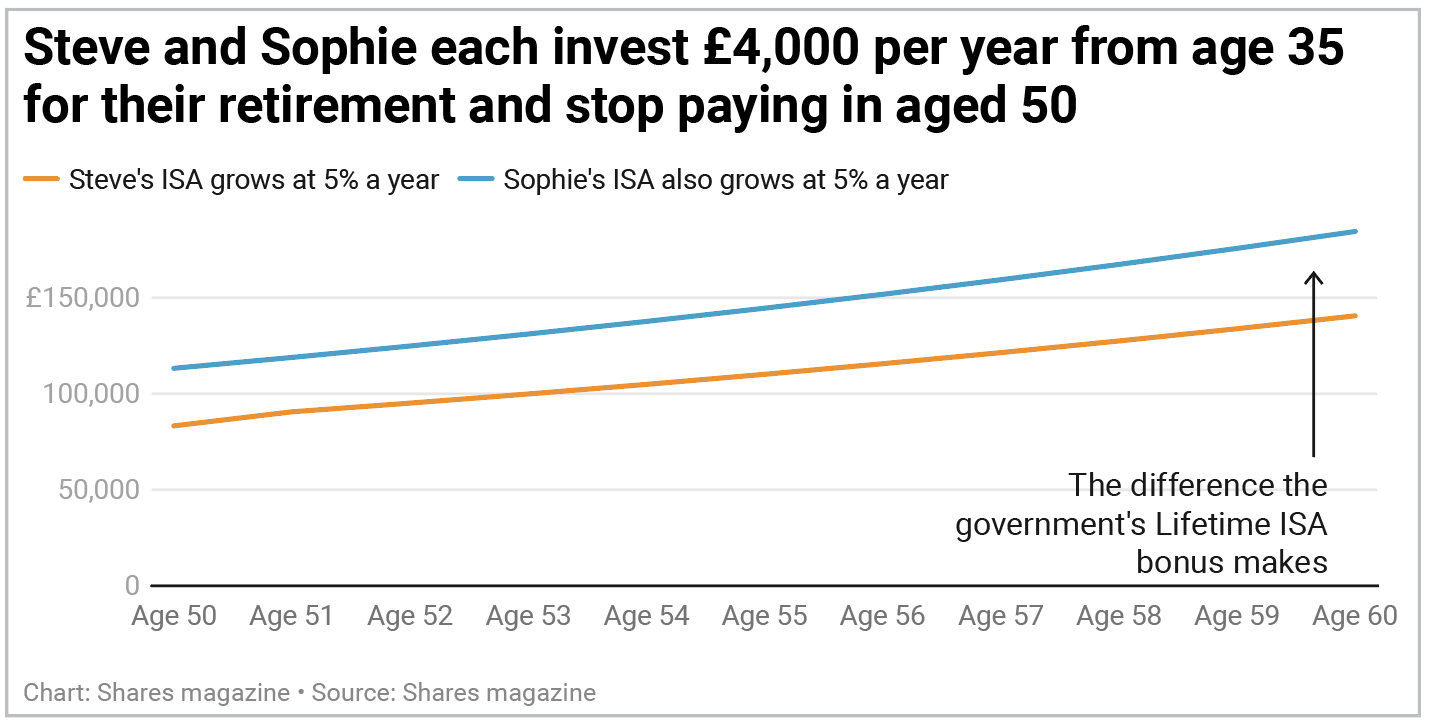

For this example, we’ve taken cousins Sophie and Steve, who are both 50 and have been paying £4,000 into their savings every year for the last 15 years. For illustrative purposes we have assumed the Lifetime ISA has been around for more than a decade and the pair opened their accounts before they turned 40.

Steve has paid his £4,000 into a stocks and shares ISA which has grown at 5% per year, while Sophie has paid her £4,000 per year into a Lifetime ISA which has also grown at 5% per year.

As in the previous example, after 15 years Steve has a pot of £86,000 and Sophie has a pot of £113,000 thanks to her government bonus.

Steve’s savings have grown to an impressive £140,000 by the time he is 60, but Sophie has done even better with her savings just topping £184,000. This is thanks to the fact she contributed to her Lifetime ISA for 15 years early in the process and received that bump of £1,000 per year.

The usual vehicle for retirement savings is a pension which comes with its own tax benefits attached and a much higher annual contribution limit of £40,000 or 100% of your qualifying earnings, whichever is lower.

For basic rate taxpayers the 25% upfront tax relief is akin to the Lifetime ISA government bonus payment, though additional and higher rate taxpayers can claim more relief on top for pension contributions through their tax return.

Even if a Lifetime ISA does not contain your main retirement pot it could be a useful ringfenced option for money you might want to use for a holiday of a lifetime when you retire, for example. Or for someone worried about breaching the lifetime allowance for pension contributions a Lifetime ISA could be a useful alternative for their retirement savings.

WHAT SHOULD YOU INVEST IN?

It is worth splitting this into three parts based on your investment horizon which will determine how much risk you can afford to take on.

Five years or less until you want to buy a house

In this situation, your best option is to keep your Lifetime ISA in cash. If you invest the money in the market and are caught out by short-term volatility you could end being without the full amount you need to lay down a deposit and your dream of a first home could be dashed. The Moneybox Lifetime ISA has a rate of 3.5% with a 12-month 0.75% bonus.

Five to 10 years until you want to buy a house

Having between five years and a decade before you want to purchase your first home gives you scope to take on a little more risk with the aim of making your money work a bit harder.

You could consider a multi-asset fund whose inherent diversification should help even out ups and downs in the market, and two solid investment trusts with a sensible approach to risk.

Offering global exposure to stocks, the investment manager of Securities Trust of Scotland (STS), Troy Asset Management has a cautious approach which might suit someone using a Lifetime ISA to buy a house within five to 10 years’ time.

Steered by James Harries and Tomasz Boniek, Securities Trust of Scotland is an investment trust with a portfolio of what the managers consider to be solid and reliable businesses which do not require lots of money to grow and therefore have a steady stream of cash which they can return to shareholders.

Among the 33 holdings are British American Tobacco (BATS), soft drinks and snacks firm PepsiCo (PEP:NASDAQ) and consumer goods firm Unilever (ULVR). It trades at a discount to net asset value of 2.1% and has an ongoing charge of 0.93%.

Another investment trust to consider is UK-focused City of London (CTY) which has an explicit income focus. Again, there is a bias towards being conservative with investors’ money. The trust targets income and capital growth from high-quality large companies with strong balance sheets. It holds defence firm BAE Systems (BA.) and publishing firm RELX (REL), among others. It trades at a slight premium to net asset value, offers a 4.7% yield and has a low ongoing charge of 0.37%.

When it comes to multi-asset funds Royal London Sustainable World Trust C Acc (B882H24) has one of the best records over the last five years and offers an ethical focus for those for whom that is an important consideration.

As at the end of January 83% of its assets were in stocks and shares with 15% in bonds and the remainder in cash. This version of the fund automatically reinvests dividends for you. The ongoing charge is 0.77%.

10 years or more until you access the cash

If you have a decade or more before you need to access the cash, either because you’re already on the property ladder and are going to use the Lifetime ISA as a retirement vehicle or you’re young and have started very early with the aim of purchasing a property down the line, then you can afford take on more risk.

You have quite a lot of flexibility in terms of potential investments. We would suggest Fidelity Global Special Situations W Acc (B8HT715), Jupiter Asian Income (BZ2YMT7) and Henderson Smaller Companies (HSL) as good starting points.

Managed by Jamie Harvey and Jeremy Podger, Fidelity Global Special Situations focuses on three distinct categories of company.

Those undergoing corporate change through restructuring, M&A or spinning off businesses; those with the ability to deliver higher-than-expected earnings growth; and unique businesses with a dominant market position, robust growth, cash flow and pricing power.

This approach has helped deliver annualised returns of 12% over the last decade. The ongoing charge is 0.92%. Holdings include Alphabet (GOOGL:NASDAQ), JPMorgan Chase (JPM:NYSE) and UnitedHealth (UNH:NYSE).

Managed by the experienced Jason Pidcock, Jupiter Asian Income is unusual in having no exposure to China, where growth has slowed, and geopolitical concerns have started to mount. A healthy weighting in Australian stocks means it is less exposed to emerging market risks than peers.

Over five years it has generated annualised returns of 8.7%. Holdings include Woodside Energy (WDS:ASX), Samsung Electronics (005930:KRX) and Singapore Telecommuncations (Z74:SGX). The ongoing charge is 1.01%.

A good small cap stock picker can often outperform the wider markets given their greater growth potential (which comes with an extra helping of risk), so Henderson Smaller Companies makes sense for someone with time on their side to invest.

Included in the portfolio are environmentally focused investment manager Impax Asset Management (IPX:AIM) and gaming firm Team17 (TM17:AIM). The ongoing charge is 0.42% and the trust trades at a 10% discount to net asset value. The 10-year annualised return is 10.1%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Investing in AIM shares for inheritance tax relief? Don’t get caught out by these issues

- Are Harbour Energy and its rivals bluffing about leaving the North Sea behind?

- Why investing in your 60s doesn't mean the end of investing for capital growth

- Lifetime ISA: top investment strategies for your first home or retirement

- How investors can take part in company fundraisings as they dial up again