VOL 25 / ISSUE 10 / 16 MARCH 2023 / £4.49 Should you be worried about investing in this sector? Banking crisis Top strategies whether you’re saving for a house or retirement USING A LIFETIME ISA

As an asset class that can diversify risk, deliver income and broaden return potential, real estate is unique. Which is why we offer a range of strategies to harness its power.

From directly owning real estate assets to investing in property companies, our real estate investment trusts seek to capture opportunity across UK commercial real estate and the dynamic European logistics sector.

From residential to retail, industrial to warehousing, see how abrdn real estate investment trusts aim to build more possibility into your portfolio.

Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested.

Request a brochure: 0808 500 4000 invtrusts.co.uk/realestate

Issued by abrdn Investments Limited, registered in Scotland (SC108419) at 10 Queen’s Terrace, Aberdeen, AB10 1XL, authorised and regulated in the UK by the Financial Conduct Authority. Please quote 3021.

•

•

I faweekcanbealongtimeinpolitics,in asfinancialmarketsitcanmakeinvestorsfeel upsidethoughtheirwholeworldhasbeenturned down. lineForyears,analystshaveconsistentlypeddledthe thathigher–oratleastrising–interestrates arepositiveforbanksbecauseitmeanstheycan generateabiggermarginontheirlending. hasInstead,lastweek’scollapseofSiliconValleyBank effectshownthatrisinginterestrateshaveanegative impactonthevalueofbonds,whichinturncan abank’sliquidity,especiallyifitsdepositsdon’tmatchitsloans. declineInvestorshavepanicked,leadingtoasharp bankinginsharepricesaroundtheworld,withoneoftheworsthitsectors.Whilemarkets 14inEuropehadstartedtocalmdownasofTuesday March,thereremaintwounansweredquestions will–aremorebanksgoingtogetintotroubleand theSVBincidentpromptcentralbankstobe knowlessaggressivewithinterestratehikes?Wedon’t theanswertotheformer,butthelatterlooksplausible.

WHATHAPPENEDTOSVB? SVBwasaspecialistlenderwithafocuson endtechnologyandventurecapitalcompanies.Atthe oflastyear,thebankhadassetsincludingloans ofaround$210billionandcustomerdepositsof around$175billion. difficulty,TherearetworeasonswhySVBgotintobothofwhichcentreonthemismatch hadbetweenitsassetsanditsdeposits.First,thebank fewerdepositsthanloans,sotofinancesomeofitsinvestmentsithadtoborrowmoneyat hadprogressivelyhigherrates,justasNorthernRock whichtoborrowfromtheUKinterbankmarket, proveditsundoing.Second,thebankwas takinginshort-termdepositsandinvestingthem

inlong-termassetslikeloanstocompaniesandUS governmentbonds. theDuetothepopularityofventure-capitalinvesting almostbank’sdepositsexplodedfrom$60billionto $200billioninashortspaceoftime,and USitdecidedtoinvestalargechunkofthismoneyin However,governmentbondswhenyieldswereverylow. lastyear’ssharpriseininterestrates everydrovedownthevalueofthebondsheldbySVBand Whenotherbank.customersstartedaskingSVBfortheir ofmoneybacklastweek,thebankhadtosellsome cashitslong-termbondholdingsatalosstoraisethe tomeetthewithdrawals.Oncethemarket gotwindSVBmightbeintroubletherewasafullshareblown‘run’onthebank,leadingtoacollapseinits price. andCalifornianstateregulatorstookoverthebank FederaltheUSTreasury,theFederalReserveandthe DepositInsuranceCorporationstepped itsintoguaranteeallofSVB’sdepositsandprotect customers.

COULDMOREBANKSBEINTROUBLE? theirAswellasguaranteeingSVB’sdepositorsthat introducedmoneywassafe,inare-runofmeasures inthegreatfinancialcrisisof2008USregulatorsagreedtoletbanksusetheFederal Reserve’s‘discountwindow’toborrowcheaplyto financecustomerwithdrawalsiftheyneededto. sinceDespitetheimprovementinbanks’capitalratios ability2008,investorsstillhaveconcernsoverthe ofsomeUSspecialistandregionallenderstomeetcustomerwithdrawalssosharesof FirstRepublicBank(FRC:NYSE)andWestern Alliance(WAL:NYSE)

Shares in the likes of Barclays, HSBC and Lloyds have slumped as investors worry about a new banking sector crisis

We explain what’s happened, what might come next and the knock-on impact for interest rates

Chancellor’sbigrevealwas theovershadowedbyadeepeningcrisisin bankingsectorwhichrockedmarkets

Panicinthebankingindustry fromovershadowedanybigmarketimpact theBudgeton15Marcheveniftheabolitionofthelifetimeallowanceon pensioncontributionswasagenuinerabbitoutof thehatforinvestors. Previouslythelifetimeallowance,whichis themaximumyoucanbuildupinapensionpot thanwithoutpayingextratax,stoodatalittlemore apparently£1million.Themotivationforthechangeis thefact80%ofNHSdoctorsretireearlyduetopensiontaxcharges. Themaximumyoucanpayintoapensioneach yeartax-freewillincreaseby50%from£40,000to if£60,000.Toputthechangesintosomeperspective, years,youweretoputaway£60,000peryearfor47 youwould’vehaveachievedasavingspot of£2.82million(withoutfactoringininterestor investmentgrowth). ChancellorJeremyHuntthrewalifelinetothose alreadyinretirementbyincreasingtheMoney

payPurchaseAnnualAllowance,howmuchyoucan moneyintoapensiononceyou’vestartedtaking allowancesoutofit,from£4,000to£10,000.Yearly of£20,000foradultISAsand£9,000forJuniorISAswereleftunchanged. ForecastsfromtheOfficeforBudget ResponsibilitysuggesttheUKwillavoidatechnical thisrecessionalthoughtheeconomywillstillshrink yearandprojectionsformedium-termgrowthhavefallen.Anextensionoftheenergyprice guaranteefrom1Aprilcouldprovideaboostto inconsumer-facingbusinesses,socouldanincrease freechildcarehoursbutthatdoesn’tbeginuntilApril2024.PubsgroupsincludingJDWetherspoon(JDW) abouncedofftheirlowsasthechancellorunveiled ‘Brexitpubsguarantee’whichmeansdutyon draughtproductsinpubswouldbeupto11p belowthedutyinsupermarketsfrom1August–a differentialwhichwillbemaintainedinthefuture. salveTherewereacoupleofannouncementsto anywoundsfromaloomingincreaseinthe Everyheadlinecorporationtaxratefrom19%to25%. poundspendonITequipment,plantor machinerycanbedeductedinfullandimmediately fromtaxableprofitforthenextthreeyears,witha plantomakethispermanentassoonaspossible. theNewsthatnuclearenergywillqualifyfor sameinvestmentincentivesasrenewableenergycouldbegoodnewsforRolls-Royce(RR.)whichisworkingonsmallmodularreactors–a technologywhichcouldenablefasterandcheaper developmentofnuclearcapacity. eachHuntpledgedtoliftthebudgettorepairpotholes opportunitiesyearby40%to£700million.Thatcreates forcompanieswhichspendtimefixingthenation’shighwaysincludingCostainwhosesharepricemovedhigheronthenews.[TS/SG]

There was plenty of good news for investors in the Budget

Discover the most important bits about new pension allowances and other changes to personal finance and tax matters

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Weexplainwhathappensifa aBPR-qualifyingcompanymovesto differentmarketoristakenoverI nvestingincertainAIMstockstoobtain theinheritancetaxreliefisapopularstrategy,yet Givenrulescanbecomplicated.thattwoofAIM’sbiggeststocksarepoisedtoleavethejuniormarket–Emis (EMIS:AIM)inatakeoverandBreedon(BREE:AIM)whichwantstomovetoLondon’sMainMarket–investorsmightbeaskinghowtherulesworkifyou switchintoadifferentqualifyingAIMstock.THEKEYRULES taxYourestatewon’thavetopaythe40%inheritance AIMchargeuponyourdeathforanyinvestmentsin stocksthatqualifyforbusinesspropertyrelief, alsoknownasBPR,andheldforatleasttwoyears. youIfaBPR-qualifyingAIMcompanyistakenover, canpassportthetimeaccruedinthestockfor heldIHTreliefqualification.Forexample,let’ssayyou ‘time’EMISforsixmonths.ToretaintheIHTrelief beforebuiltup,youwouldneedtoselltheshares reinvestthetakeoverbecomesunconditional.You theproceedsinanotherBPR-qualifying willAIMcompanyandafterafurther18monthsyou investmentshavebuiltupatotaloftwoyearsinqualifying andqualifyforIHTreliefonthatpartofyourportfolio.WHATIFIBOUGHTSHARESINTHESAMESTOCK ATDIFFERENTTIMES?

Let’ssayyouinvestedinEMISontwoseparate occasions,1,000sharesboughtthreeyearsago six(whichwe’llcallParcelA)and250sharesbought Youmonthsago(ParcelB). proceedsselltheEMISsharesandreinvestthefull intoanotherBPR-qualifyingstock.Thisiswhereyouwillneedtohavekeptaccurate recordsofalltransactions. ParcelAhadbeenheldforthreeyearssoalready

Two of AIM’s biggest stocks could soon leave the junior market

qualifiesforIHTrelief.Youworkouttheamount receivedfromsellingthose1,000sharesand whereveryoureinvest(itcanbeinmorethanone BPR-qualifyingstock)thatnewinvestmentwillalso qualifyforIHTrelief. youParcelBhadonlybeenheldforsixmonthsso needtoworkoutthevalueofthe250sharessoldand,whereveryoureinvest,thosenew ofBPR-qualifyingsharesboughtwiththeproceeds beforeParcelBmustbeheldforafurther18months thatpartofyourportfolioqualifiesforIHTrelief. youOnceyou’vehitthetwo-yearqualifyingperiod, cansellthesharesandhavethreeyearstouse inthatcashasyouwish.Butyoumustbereinvested periodqualifyingAIMstocksbeforethethree-year endstoretaintheIHTreliefstatus. replacement‘Iftheinvestordieswhenstillincash,before stockshavebeenpurchased,thecash ChriswouldbeintheestateandsubjecttoIHT,’notes BoxallfromFundamentalAssetManagement,aspecialistinAIM/IHT.‘InvestinginAIMforIHT atplanningpurposesreallydemandsfullinvestment alltimes.’

ByDanielCoatsworthEditorIf you’re holding EMIS and Breedon to qualify for IHT relief, you need to think about your next steps now

Find out which companies in the FTSE 100 have the highest dividend yields

How popular tech fund Allianz

Trust is tackling risk after losing 7% to benchmark

The investment world likes to complicate everything. Our Managed Fund likes to keep it really simple. It’s made up of equities, bonds and cash, and we think to generate great returns, that’s all you need. The result is a balanced portfolio with low turnover and low fees. Beautifully straightforward, it’s been answering questions since 1987.

Please remember that changing stock market conditions and currency exchange rates will affect the value of the investment in the fund and any income from it. Investors may not get back the amount invested.

Find out more by watching our film at bailliegifford.com

The biggest US bank collapse in a decade has rocked investor confidence

If a week can be a long time in politics, in financial markets it can make investors feel as though their whole world has been turned upside down.

For years, analysts have consistently peddled the line that higher – or at least rising – interest rates are positive for banks because it means they can generate a bigger margin on their lending.

Instead, last week’s collapse of Silicon Valley Bank has shown that rising interest rates have a negative effect on the value of bonds, which in turn can impact a bank’s liquidity, especially if its deposits don’t match its loans.

Investors have panicked, leading to a sharp decline in share prices around the world, with banking one of the worst hit sectors. While markets in Europe had started to calm down as of Tuesday 14 March, there remain two unanswered questions – are more banks going to get into trouble and will the SVB incident prompt central banks to be less aggressive with interest rate hikes? We don’t know the answer to the former, but the latter looks plausible.

SVB was a specialist lender with a focus on technology and venture capital companies. At the end of last year, the bank had assets including loans of around $210 billion and customer deposits of around $175 billion.

There are two reasons why SVB got into difficulty, both of which centre on the mismatch between its assets and its deposits. First, the bank had fewer deposits than loans, so to finance some of its investments it had to borrow money at progressively higher rates, just as Northern Rock had to borrow from the UK interbank market, which proved its undoing. Second, the bank was taking in short-term deposits and investing them

By Ian Conway Companies Editor

By Ian Conway Companies Editor

in long-term assets like loans to companies and US government bonds.

Due to the popularity of venture-capital investing the bank’s deposits exploded from $60 billion to almost $200 billion in a short space of time, and it decided to invest a large chunk of this money in US government bonds when yields were very low. However, last year’s sharp rise in interest rates drove down the value of the bonds held by SVB and every other bank.

When customers started asking SVB for their money back last week, the bank had to sell some of its long-term bond holdings at a loss to raise the cash to meet the withdrawals. Once the market got wind SVB might be in trouble there was a fullblown ‘run’ on the bank, leading to a collapse in its share price.

Californian state regulators took over the bank and the US Treasury, the Federal Reserve and the Federal Deposit Insurance Corporation stepped in to guarantee all of SVB’s deposits and protect its customers.

As well as guaranteeing SVB’s depositors that their money was safe, in a re-run of measures introduced in the great financial crisis of 2008 US regulators agreed to let banks use the Federal Reserve’s ‘discount window’ to borrow cheaply to finance customer withdrawals if they needed to.

Despite the improvement in banks’ capital ratios since 2008, investors still have concerns over the ability of some US specialist and regional lenders to meet customer withdrawals so shares of First Republic Bank (FRC:NYSE) and Western Alliance (WAL:NYSE) slumped after the SVB debacle.

In the UK, shares of the big high-street banks Barclays (BARC), HSBC (HSBA), Lloyds (LLOY) and

NatWest (NWG) have also been under pressure and by the evening of 13 March the FTSE 350 bank index had lost close to 10% of its value in a week.

Shares of smaller, less heavily capitalised firms such as Bank of Georgia (BGEO), TBC Bank (TBCG) and Virgin Money (VMUK), which rely on the stability of their deposit base, also fell on the stock market although there is no indication that any of them have any operational difficulties.

Ratings agency Moody’s believes the decline in bond values is temporary and most European banks have enough liquidity to meet any potential liability, allowing them to hold their bonds to maturity.

HSBC paid £1 to rescue the UK arm of SVB and protect its depositors. The company said the acquisition would strengthen its commercial banking arm and enhance its ability to serve ‘innovative and fast-growing firms’, including in the technology and life-science sectors.

The Bank of England said the deal would ensure ‘the continuity of banking services, minimising disruption to the UK technology sector and supporting confidence in the financial system’.

It also stressed no other UK banks were materially affected by the failure of SVB and the wider UK banking system was ‘safe, sound and well capitalised’.

The immediate effect of the turmoil at SVB is likely to be that banks and other financial firms tighten

‘Assuming the economic impact is relatively contained, we do not see a clear read-across (from SVB), particularly for the larger US and European banks, for several reasons.

Large banks are subject to more comprehensive and thorough regulation. For instance, in Europe, banks are limited in how much rate

mismatching they can take on their held-to-maturity bond portfolios, due to Basel 4 regulations. This means that they will not face the same steep negative equity position that SVB found itself in with its deeply underwater securities book.

Hence, the average European bank has losses of just ~5% of

tangible equity, compared to the 124% that SVB showed as of year-end.

‘Further, European and large US banks must deduct unrealised losses on securities accounted at fair value (i.e., marked to market on a quarterly basis, in contrast to held-to-maturity) from their regulatory capital.’

their lending criteria making it harder for fledgling companies, which are notorious for burning through cash before they generate a profit, to borrow money.

Another effect is investors are likely to want to put a bigger discount on assets held in venture capital funds and potentially on private assets in general to compensate them for what they perceive to be increased risk. That doesn’t bode well for investment trusts invested in private markets.

As well as prompting a sell-off in bank stocks around the world, the collapse of SVB has spurred frantic buying of government bonds as investors look to reduce their risk exposure in favour of ‘safe’ assets.

That in turn has led to a steep decline in bond yields and in market expectations for interest rate rises by the Federal Reserve and the Bank of England over the next couple of months.

Whereas traders were worrying last week that Fed chair Jerome Powell was ready to raise interest rates faster than they had anticipated, this week all bets seem to be off.

Instead of a 50 basis-point hike, economists at

investment bank Goldman Sachs now expect the Fed to leave interest rates unchanged on the next rate decision day (22 March) despite the bank’s primary aim being to rein in inflation, not alleviate strains in the financial sector.

While SVB may well have been an outlier, with investors worried about possible contagion due to unrealised bond losses on banks’ balance sheets and potentially a broader financial crisis, many observers are arguing the Fed should take its time to assess the impact of the bank’s collapse and allow sentiment to recover.

While the news around SVB has caused shockwaves across global stock markets, we do not see a reason to panic and sell shares.

Admittedly there is now a heightened risk of tighter regulation among banks which means investor sentiment could temporarily remain poor towards the sector. That will put pressure on banks to provide reassurance they have strong balance sheets and aren’t in trouble.

Most people hold shares in banks for generous dividends and we do not expect payouts to be cut from the UK banking stocks in the wake of the SVB crisis.

One of the reasons that the Federal Reserve could deliver fast and impactful interest rate increases over the past year is that the system could take it.

Equity markets and bond markets may have crumbled, but as long as the system was intact the Fed could continue to tighten.

The SVB saga as a standalone mutes the ability of the Federal Reserve to over-tighten from here, as there is an implied threat to the system should the Fed be seen to be overdoing it.

Risk barometers like FRA/ OIS and the cross-currency

basis have spiked, but not dramatically so. This suggests the system has had a wobble but is absolutely not under immediate threat.

The down move in the yield curve points to a material reduction in the likelihood that the Fed overdoes it on rate hikes.

We argue that what equity markets do here is not that relevant. They can come under pressure, but the really important thing to monitor is the financial system. If that were to be materially threatened, the Fed could not hike at all.

We only have to look at the global financial crisis and the pandemic as templates that showed the Fed is single-minded when the system is under threat, and that is to cut rates and ease policy, significantly.

We are not at that point, and we most likely won’t get to that point. But if the inflation data refuses to dampen in a material fashion it places pressure on the Fed to make a tough choice. The simplest choice is to stick with a 25 basis point rise and let the market calm down of its own accord in the weeks and months ahead.

Chancellor’s big reveal was overshadowed by a deepening crisis in the banking sector which rocked markets

Panic in the banking industry overshadowed any big market impact from the Budget on 15 March even if the abolition of the lifetime allowance on pension contributions was a genuine rabbit out of the hat for investors.

Previously the lifetime allowance, which is the maximum you can build up in a pension pot without paying extra tax, stood at a little more than £1 million. The motivation for the change is apparently the fact 80% of NHS doctors retire early due to pension tax charges.

The maximum you can pay into a pension each year tax-free will increase by 50% from £40,000 to £60,000. To put the changes into some perspective, if you were to put away £60,000 per year for 47 years, you would’ve have achieved a savings pot of £2.82 million (without factoring in interest or investment growth).

Chancellor Jeremy Hunt threw a lifeline to those already in retirement by increasing the Money

Purchase Annual Allowance, how much you can pay into a pension once you’ve started taking money out of it, from £4,000 to £10,000. Yearly allowances of £20,000 for adult ISAs and £9,000 for Junior ISAs were left unchanged.

Forecasts from the Office for Budget Responsibility suggest the UK will avoid a technical recession although the economy will still shrink this year and projections for medium-term growth have fallen. An extension of the energy price guarantee from 1 April could provide a boost to consumer-facing businesses, so could an increase in free childcare hours but that doesn’t begin until April 2024.

Pub groups including JD Wetherspoon (JDW) bounced off their lows as the chancellor unveiled a ‘Brexit pubs guarantee’ which means duty on draught products in pubs would be up to 11p below the duty in supermarkets from 1 August – a differential which will be maintained in the future.

There were a couple of announcements to salve any wounds from a looming increase in the headline corporation tax rate from 19% to 25%. Every pound spend on IT equipment, plant or machinery can be deducted in full and immediately from taxable profit for the next three years, with a plan to make this permanent as soon as possible.

News that nuclear energy will qualify for the same investment incentives as renewable energy could be good news for Rolls-Royce (RR.) which is working on small modular reactors – a technology which could enable faster and cheaper development of nuclear capacity.

Hunt pledged to lift the budget to repair potholes each year by 40% to £700 million. That creates opportunities for companies which spend time fixing the nation’s highways including Costain (COST) whose share price moved higher on the news. [TS/SG]

The modern world is built on technology – an ever-advancing megatrend changing our lives today and shaping our future.

As one of the largest, most experienced technology investment teams in Europe, we have deep experience in identifying trends early. With major innovations transforming industries and companies across the world, we are embracing these opportunities.

polarcapitaltechnologytrust.co.uk

London Stock Exchange Ticker: PCT

Discover more about the investment potential of technology at Capital at risk and investors may not get back the original amount invested. This advertisement should not be construed as advice for investment. Important information: This announcement constitutes a financial promotion pursuant to section 21 of the Financial Services and Markets Act 2000 and has been prepared and issued by Polar Capital LLP. Polar Capital is a limited liability partnership with registered number OC314700, authorised and regulated by the UK Financial Conduct Authority (“FCA”)

FULL-YEAR RESULTS

21 March: Kingfisher, Oxford Nanopore Technologies, Fintel, Ergomed, Alliance Pharma, Zotefoams, Kape Technologies, Tissue Regenix, Luceco, Gamma Communications, Aptitude Software, Quixant, Henry Boot, Equals, Staffline

22 March: Hostelworld, Ten Entertainment, Vistry, Fevertree Drinks, Pendragon, LSL Property Services, Anpario, MPAC, Genel Energy, Judges Scientific, Essentra, BioPharma Credit

23 March: Playtech, Portmeirion, Safestyle, Sopheon, Pollen Street

HALF-YEAR RESULTS

20 March: SCS, YouGov

23 March: Smiths Group

TRADING UPDATES

22 March: Bloomsbury Publishing

Can the posh mixers maker regain some fizz when it posts 2022 results?

After enjoying years of fizzing earnings upgrades and share price gains off the back of its 2014 stock market listing, posh mixers maker Fevertree (FEVR:AIM) has gone flat in recent times.

In January the company downgraded 2023 guidance thanks to rising costs – this negative news coming off the back of three profit warnings in 2022.

A key selling point for Fevertree and

B&Q-owner bemoaned a ‘challenging’ consumer outlook when downgrading profit guidance in November

Full year results (21 March 2023) from Kingfisher (KGF) will reveal if the DIY retailer’s sales resilience continued in the final quarter, supported by demand for energyefficiency products.

The B&Q, Screwfix and Castorama brands owner proved a lockdown winner as spending on home improvement projects surged, but the cost-of-living crisis and housing market downturn represent stiff headwinds for the company.

Kingfisher lowered its full year

its premium proposition is its glass bottles (which now account for 80% of its sales mix) but the cost of producing these is heavily tied to volatile energy prices. Supply chain issues have also impacted US sales.

When it reports 2022 results on 22 March, Fevertree needs to demonstrate it is making progress on a plan to bring on stream bottling capacity in the US to help limit logistics costs and disruption. [TS]

profit outlook with its third quarter update (24 November 2022) due to the ‘challenging’ outlook for consumer spending. [JC]

The sportswear firm is hoping for a boost from China reopening as its main rival struggles

US trainers and sportswear giant Nike (NKE:NYSE) posts third quarter numbers on 21 March with investors hoping it can match the strong second quarter update.

In the previous three-month period, earnings per share of $0.85 was comfortably ahead of the $0.64 consensus forecast and the

Investors will have much to chew over with the company's Q3 results

Third quarter results (23 March) from General Mills (GIS:NYSE) provide an opportunity to see if the cereal maker has sustained the positive momentum engendered by its ‘Accelerate’ strategy as consumers grapple with cost-ofliving pressures. The food multinational behind the Cheerios, Nature Valley and Haagen-Dazs brands recently raised guidance for the financial year to May 2023, citing resilient consumer demand

company also raised its outlook, as management flagged progress clearing a chunky inventory pile that arose in large part due to supply chain disruptions.

Key areas of focus for the third quarter will be the impact of China reopening on its sales and whether it has been able to capitalise on the recent travails of its rival Adidas (ADS:ETR) which boss Bjørn Gulden, who took over at the start of 2023, is hoping to turn around. [TS]

17 March: Lithium

Americas, Ballard, Orla Mining, Janux Therapeutics

20 March: Cathay

Financial, Foot Locker

21 March: Nike

22 March: Tencent, GameStop

23 March: Accenture, General Mills, Cintas, Carnival

17 March: Vonovia

23 March: Hamburger Hafen

and the growth opportunities afforded by its brand portfolio, notably dog and cat food brand Blue Buffalo. [JC]

71% of us wish we were more patient in at least one aspect of our lives. But patience isn’t just a virtue – it has real-world value, too.1

As an investment trust that’s been trusted for generations, we understand a few things about patience.

Our research shows that investors who remained invested through the ups and downs could have built up a Patience Pot worth as much as £192k over 30 years.2

So if you want to make the most of your investments, it could pay to choose an investment trust that truly understands the value of patience.

Find out why now is the right time to start profiting from patience with Alliance Trust. alliancetrust.co.uk/patience

With SVB’s collapse leading to market volatility this ETF offers exposure to the prized precious metal

With concerns about systemic risk in the banking sector, gold’s qualities as a safe haven are once again coming to the fore and we’ve found an excellent way to play the precious metal.

Gold typically performs well during periods of low growth and sticky inflation and when investors are feeling nervous. Arguably all three of these factors are present and correct right now.

Even aside from the collapse of banking group SVB, the crash seen at several crypto-linked institutions and the ongoing volatility in this part of the market has blown out of the water any claims for bitcoin as an alternative store of value to gold.

One of the things which has held gold back recently has been rising interest rates and the implications for gold’s attractiveness relative to assets like cash and bonds which, after all, offer something gold doesn’t: an accompanying income stream.

($/oz)

2,000

1,500

1,000

Price: £10.46

Net assets: £1.29 billion

20142016201820202022

Chart: Shares magazine • Source: Refinitiv

However, the collapse of SVB has led to a reduction in rate expectations, at least for the time being, and this should be supportive to gold.

A step back for the dollar, which tends to have an inverse relationship to the metal, is also helpful. On the flipside if rates are higher for longer and if the dollar strengthens these could help dull gold’s shine

as a defensive asset – something investors should bear in mind.

Investing in gold miners, while it comes with operational risk, also allows you to typically secure income from dividends and enjoy outsized gains if they can deliver growth.

A diversified fund of gold producers protects you from the risk of being caught out by the failings of individual companies and iShares Gold Producers (SPGP) is a low-cost way of achieving this kind of exposure.

The exchange-traded fund has an ongoing charge of 0.55% and has delivered a five-year annualised total return of 9% versus 6.6% from BlackRock Gold & General (B5ZNJ89), the big actively managed gold mining fund which has a much higher ongoing charge of 1.16%.

Dividends are automatically reinvested into the ETF which tracks the S&P Commodity Producers Gold index, a basket of companies engaged in exploration and production of gold. Its largest holding is Barrick Gold (GOLD:NYSE), a $30 billion miner headquartered in Canada which has assets across the globe, including in the Americas, Africa and Asia.

It has a stake in Franco-Nevada (FNV:NYSE) which receives royalties on revenue from various third-party mines. It also invests in Newmont (NEM:NYSE), the world’s largest gold miner by output, and which last month made a $17 billion takeover bid for Australian rival Newcrest (NCM:ASX). [TS]

Trulyglobalandaward-winning,therangeissupported byexpertportfoliomanagers,regionalresearchteamsand on-the-groundprofessionalswithlocalconnections.

With400investmentprofessionalsacrosstheglobe,webelieve thisgivesusstrongerinsightsacrossthemarketsinwhichweinvest. Thisiskeyinhelpingeachtrustidentifylocaltrendsandinvestwith theconvictionneededtogeneratelong-termoutperformance.

Fidelity’srangeofinvestmenttrusts:

•FidelityAsianValuesPLC

•FidelityChinaSpecialSituationsPLC

•FidelityEmergingMarketsLimited

•FidelityEuropeanTrustPLC

•FidelityJapanTrustPLC

•FidelitySpecialValuesPLC

Thevalueofinvestmentscangodownaswellasupandyoumay notgetbacktheamountyouinvested.Overseasinvestmentsare subjecttocurrencyfluctuations.Thesharesintheinvestmenttrusts arelistedontheLondonStockExchangeandtheirpriceisaffected bysupplyanddemand.

Theinvestmenttrustscangainadditionalexposuretothemarket, knownasgearing,potentiallyincreasingvolatility.Investmentsin emergingmarketscanmorevolatilethatothermoredeveloped markets.Taxtreatmentdependsonindividualcircumstancesand alltaxrulesmaychangeinthefuture.

Tofindoutmore,scantheQRcode,goto fidelity.co.uk/itsorspeaktoyouradviser.

Thelatestannualreports,keyinformationdocument(KID)andfactsheetscanbeobtainedfromourwebsiteat www.fidelity.co.uk/its orbycalling0800414110.Thefullprospectusmayalsobeobtained fromFidelity.TheAlternativeInvestmentFundManager(AIFM)ofFidelityInvestmentTrustsisFILInvestmentServices(UK)Limited.IssuedbyFinancialAdministrationServicesLimited,authorisedand regulatedbytheFinancialConductAuthority.Fidelity,FidelityInternational,theFidelityInternationallogoandFsymbolaretrademarksofFILLimited.Investmentprofessionalsincludebothanalystsand associates.Source:FidelityInternational,30September2022.Dataisunaudited.UKM1222/380938/SSO/1223

The engineering support services group is a self-help story with significant rerating potential

As volatility returns, one way to protect your portfolio is to tap into returns that aren’t reliant on the global economy or the direction of markets.

We think Babcock International (BAB) is a good option as it undergoes an internally-driven, multi-year turnaround.

The engineering support services play has had a difficult time. However, Shares believes a rebound from October 2022 lows has further to run as Babcock benefits from self-help and a step-up in defence spending over the coming decade.

The FTSE 250 constituent is at the start of a major recovery after several turbulent years, having been hit hard by additional costs during the pandemic. A specialist in managing complex assets and infrastructure in safety and mission-critical environments, Babcock swung from a £1.81 billion loss to pre-tax profit of £182.3 million in the year to March 2022.

This was the first year of its turnaround under CEO David Lockwood and chief financial officer David Mellors, who together successfully turned round defence outfit Cobham before its £4 billion sale to US private equity firm Advent in 2020.

Following the conclusion of a disposals programme designed to refocus Babcock on its core capabilities as a critical defence supplier to the UK and international partners whilst strengthening the balance sheet, defence now accounts for roughly two thirds of group revenue, and contract wins are coming through.

The backdrop for defence and security equipment and services providers has visibly improved due to Russia’s invasion of Ukraine and tensions between the west and China. This environment is favourable for Babcock, the

Price: 328.8p

Market cap: £1.66 billion

second largest supplier to the UK Ministry of Defence with a leading position in the UK maritime defence sector.

The company owns and operates complex marine engineering infrastructure in the UK and undertakes 100% of the in-service support and deep maintenance for the UK’s nuclear powered submarines fleet, as well as for a high proportion of UK surface warships.

Cost savings are coming through and margins are set to recover, driving positive free cash generation in the year to March 2024.

Based on Shore Capital’s 2024 and 2025 earnings estimates of 38.5p and 43.6p, Babcock trades on single digit prospective price-to-earnings ratios of 8.5 and 7.5, a discount to peers such as BAE Systems (BA.) and Qinetiq (QQ.) on double digit earnings multiples. This suggesting a rerating is overdue, while an imminent return to the dividend list offers an additional catalyst. [JC]

Asset Value Investors (AVI) has been finding compelling opportunities in Japan for over three decades. Despite a year filled with challenges and volatility, Japanese equities fared relatively well.

Many investors may be surprised to hear of Japan’s resilience during what was a difficult year for global equity markets. After all, Japan has suffered from stagnant growth and an ageing population for a prolonged period of time. However, Japan has a relatively stable economy and the attitude towards corporate governance has improved significantly since the onset of ‘Abenomics’. Japan is now the world’s second largest activist market. Activist events have risen 110%* over five years, as pressure from shareholders continued to intensify. This was accompanied by a surge in corporate buybacks as cash was returned to investors.

Excess cash is one of the things that the investment team at Asset Value Investors (AVI) look for in Japan. AVI’s portfolio of 20-25 stocks are all companies that have been thoroughly examined by the investment team to find value, quality, and an event to realise the upside. Key to the strategy is to build relationships with company management, actively working together to improve shareholder value. While AVI can launch public campaigns, it aims to work behind closed doors with management to find mu-

tually beneficial solutions. The depth of the investment team provides AVI the resources to undertake detailed and targeted research.

In 2022, our engagement was mostly behind the scenes. Over 120 meetings were held with 26 portfolio companies and 24 detailed letters or presentations were sent to these companies. This engagement is well supported by the broader changes in the attitudes of Japanese management as they are encouraged by the Japanese Corporate Governance Code to better allocate capital. The result is long term sustainable improvements in returns for investors.

As anyone who has invested in Japan will know, change takes time. Discovering

overlooked and under researched investment opportunities requires a long-term approach. A long-term time horizon aligns AVI with the interests of the management to work together on creating shareholder value.

The companies AVI invests in have cash on their balance sheets and attractive business models with either stable earnings or structural growth trends to ensure corporate value is growing.

In 2018, AVI launched the now c. £149m* AVI Japan Opportunity Trust (AJOT). The strategy’s first four years bears witness to the success of this approach, with a strong NAV total return and outperformance of its Japan small-cap benchmark. AVI’s aim is to be a constructive,

stable partner and to bring our expertise – garnered over three decades of investing in Japan. We are optimistic about the macro environment in Japan. The weak Yen makes Japan highly cost-competitive, both for tourism and manufacturing. Our portfolio includes a variety of sectors, with strong exposure to the domestic Japanese economy. Inflation has returned after a 40-year absence and with wage growth and increased spending, we expect to see better allocation of capital and improved productivity, which would support returns for investors. AVI is well positioned to capture this long-term opportunity with a unique investment approach and established track record.

More pension schemes are expected to bring forward their defined benefit de-risking plans

Gain to Date: 13%

We highlighted the attraction of annuities and lifetime mortgages specialist Just Group (JUST) on 1 December 2022 based on its underappreciated transformation to positive cash generation and predictable cash flows.

With the bulk annuities market predicted to complete more than £600 billion worth of deals over the next decade according to consultant Lane Clark & Peacock, Just Group is well positioned to capture more of the market.

Pleasingly, the shares have moved up nicely, reflecting momentum in the business and stronger than expected trading.

In early March the company delivered knock-out fiscal 2022 numbers with adjusted operating profit up 41% to £336 million which was way ahead of analysts’ expectations.

Higher interest rates have improved pension scheme funding levels ‘materially’, and strong deal momentum in the back half of 2022 has continued into 2023 with the firm signing its largest transaction to date at £513 million this month.

Strong trading drove organic capital generation of £134 million which Jefferies estimates was three times the consensus expectation and allowed the firm to increase the full year dividend by 15% to 1.73p per share.

The company reiterated confidence in achieving its 15% target growth in operating profits per annum on average over the next three years.

Analysts at JPMorgan Cazenove suggested the firm’s £6 billion defined benefit pension pipeline meant there was ‘upside risk’ to the chief executive’s forecast.

While the shares have got off to a great start since we highlighted them as attractive, there is arguably more upside to go.

Analysts have increased their 2023 earnings estimates by around 10% since the beginning of the year which should continue to be supportive.

The shares trade on a lowly four times 2023 forecast earnings per share and well below net tangible assets of 170p per share which looks too stingy. We remain positive. [MG]

We explain what happens if a BPR-qualifying company moves to a different market or is taken over

Investing in certain AIM stocks to obtain inheritance tax relief is a popular strategy, yet the rules can be complicated. Given that two of AIM’s biggest stocks are poised to leave the junior market – Emis (EMIS:AIM) in a takeover and Breedon (BREE:AIM) which wants to move to London’s Main Market –investors might be asking how the rules work if you switch into a different qualifying AIM stock.

Your estate won’t have to pay the 40% inheritance tax charge upon your death for any investments in AIM stocks that qualify for business property relief, also known as BPR, and held for at least two years.

If a BPR-qualifying AIM company is taken over, you can passport the time accrued in the stock for IHT relief qualification. For example, let’s say you held EMIS for six months. To retain the IHT relief ‘time’ built up, you would need to sell the shares before the takeover becomes unconditional. You reinvest the proceeds in another BPR-qualifying AIM company and after a further 18 months you will have built up a total of two years in qualifying investments and qualify for IHT relief on that part of your portfolio.

Let’s say you invested in EMIS on two separate occasions, 1,000 shares bought three years ago (which we’ll call Parcel A) and 250 shares bought six months ago (Parcel B).

You sell the EMIS shares and reinvest the full proceeds into another BPR-qualifying stock. This is where you will need to have kept accurate records of all transactions.

Parcel A had been held for three years so already

qualifies for IHT relief. You work out the amount received from selling those 1,000 shares and wherever you reinvest (it can be in more than one BPR-qualifying stock) that new investment will also qualify for IHT relief.

Parcel B had only been held for six months so you need to work out the value of the 250 shares sold and, wherever you reinvest, those new BPR-qualifying shares bought with the proceeds of Parcel B must be held for a further 18 months before that part of your portfolio qualifies for IHT relief.

Once you’ve hit the two-year qualifying period, you can sell the shares and have three years to use that cash as you wish. But you must be reinvested in qualifying AIM stocks before the three-year period ends to retain the IHT relief status.

‘If the investor dies when still in cash, before replacement stocks have been purchased, the cash would be in the estate and subject to IHT,’ notes Chris Boxall from Fundamental Asset Management, a specialist in AIM/IHT. ‘Investing in AIM for IHT planning purposes really demands full investment at all times.’

By Daniel Coatsworth Editor

By Daniel Coatsworth Editor

UK investment trusts are trading at the widest discount seen since the financial crisis, according to recent research from Numis. The share price of the average investment trust was trading 13% below its net asset value in 2022, which suggests that there is value to be found in this well-established and diverse part of the UK investment industry. It could, therefore, be a good time for investors to be considering investment trusts as a buying opportunity.

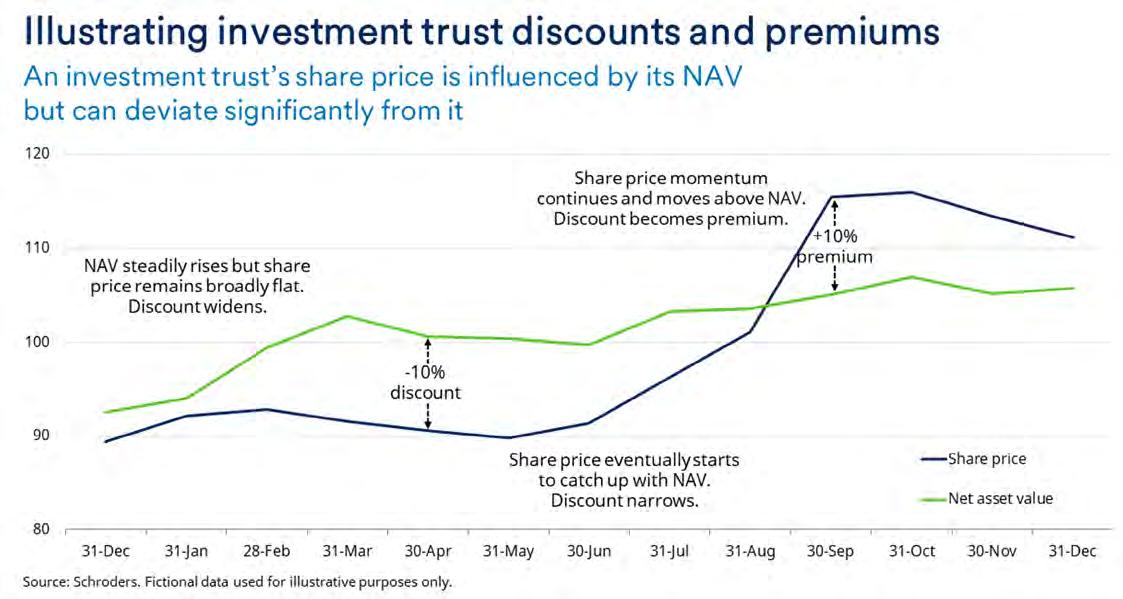

Investment trusts are stock market listed companies, so their shares are subject to the forces of demand and supply. A stock market works by setting a price at which demand (the quantity of shares that investors want to buy) and supply (the quantity of shares that investors want to sell) are in equilibrium. As demand and supply change over time, you should expect a share price to move to maintain the balance between these two forces. This is the same for all quoted companies, but with investment trusts there is an additional measure of actual value, against which the share price can be compared. This is known as ‘net asset value’ (NAV for short), and it is essentially the value of all the assets held in that investment trust’s portfolio at a given point in time expressed on a per share basis. Most investment trusts release their

NAV every day, but some – particularly those that invest in less liquid or private assets – release their NAVs less frequently.

The presence of a NAV calculation means that investors get a regular look at the actual value of that investment trust which they can then compare to the prevailing share price to get a sense of how cheap or expensive it is. This is a key differentiator between investment trusts and other ‘open-ended’ investment vehicles such as OEICs, ICVCs and unit trusts, where the value at which investors can buy or sell units is determined explicitly by NAV, and supply and demand are instead balanced by changing the number of units in issue on a daily basis.

When the share price of an investment trust is trading below its NAV, it is said to be trading at a

discount. Conversely, if the investment trust’s share price is above its NAV, it is said to be trading at a premium. The chart and table above and on the right should help to illustrate this with a simple example, showing how the share price and NAV of an investment trust interact over time. Put simply, an investment trust’s share price will be influenced by its NAV but over time, it can deviate significantly from it in both directions.

Broadly speaking, if an investment trust is trading on a discount, it reflects slightly lower demand than supply. This can happen for a number of reasons, such as uncertainty about the outlook for the asset class the trust is invested in, or a lack of interest or liquidity in a particular market or investment theme. By contrast, an investment trust on a premium tends to reflect high demand as a result of elevated investor enthusiasm for a particular characteristic. Sometimes, however, discounts and premiums can arise simply because stock markets are not always totally efficient.

For investment trusts that release NAV data less frequently, a discount or premium may represent the market trying to estimate the change in the value of its assets since the NAV was last released. So, it is always important to try to understand why an investment trust share price has deviated from its NAV before making an investment decision. Nevertheless, a discount does effectively mean that investors have the potential opportunity to buy an asset for less than it is estimated to be worth. It’s bargain hunting time!

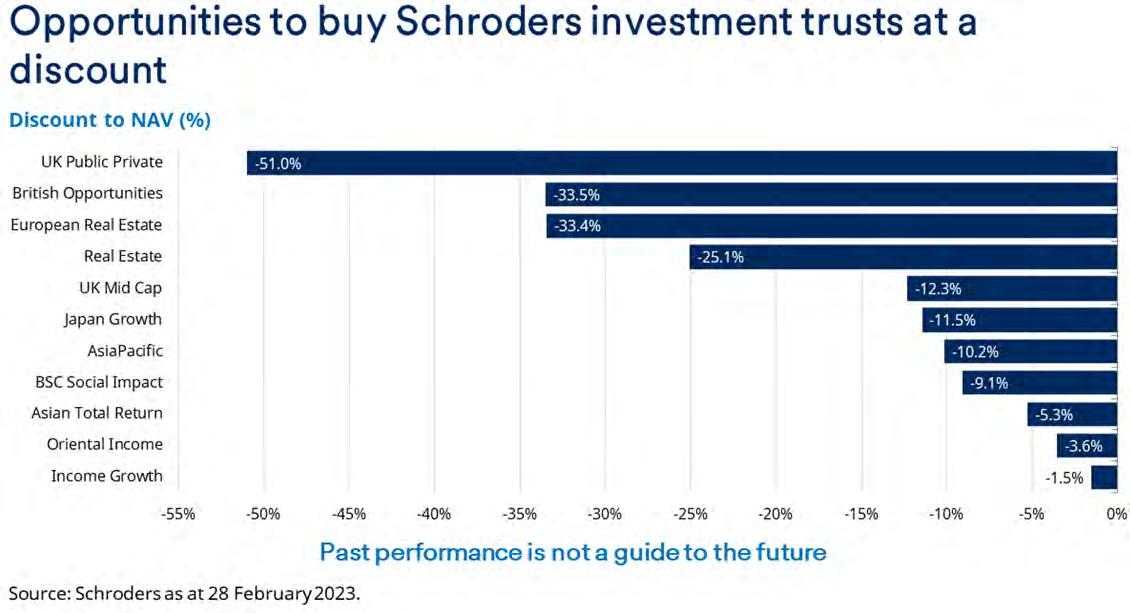

As the chart on the previous page illustrates, all Schroders investment trusts are currently available to buy at a share price below NAV. Discounts (as at 28 February 2023) range from -1.5% on Schroder Income Growth Fund plc, through to -51.0% for Schroder UK Public Private Trust plc

The fact that UK investment trusts have been trading at their widest discount for fifteen years suggests there are currently bargains to be found if investors look carefully. Due diligence is, as always, vital, and investors should do their research before committing to an investment.

We are confident in the investment proposition of each of Schroders investment trusts and would encourage investors to find out more to understand the individual attractions of the Schroders range. The long-term chart at the beginning of this article suggests that the broad level of discount currently seen on UK investment trusts won’t remain this wide forever. Happy shopping!

Find out more about Schroders Investment Trusts

This is a marketing communication.

Past performance is not a guide to future performance and may not be repeated.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

Any reference to sectors/countries/stocks/ securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy.

Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy.

For help in understanding any terms used, please visit address www.schroders.com/en/insights/ invest-iq/investiq/education-hub/glossary/

We recommend you seek financial advice from an Independent Adviser before making an investment decision. If you don’t already have an Adviser, you can find one at www.unbiased.co.uk or www.vouchedfor.co.uk

Before investing in an Investment Trust, refer to the prospectus, the latest Key Information Document (KID) and Key Features Document (KFD) at www.schroders.co.uk/investor or on request.

Issued in March 2023 by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registration No 4191730 England. Authorised and regulated by the Financial Conduct Authority

The emergence of PrimaryBid and REX means institutions aren’t the only investors being offered stock potentially at a discount

This year has brought some tentative optimism from investors linked to easing inflation and Chinese reopening. Corporate confidence is gradually recovering after the invasion of Ukraine brought fundraisings to a halt, with businesses beginning to tap the market for growth capital again.

In this article, we outline why the year ahead should see a rebound in equity fundraisings and explain how retail investors can get involved, often at attractive share price discounts.

2020 and 2021 were bumper years for fundraisings on the London Stock Exchange; 2020 because the onset of the pandemic and lockdowns meant companies needed cash to shore-up balance sheets, 2021 as companies sought fresh funds to capitalise on an anticipated post-Covid recovery that was derailed by inflation and the Ukraine conflict.

After a subdued 2022, investment bankers are sharpening their pencils for an uptick in fundraisings this year. And given higher interest rates, companies are looking to raise equity rather than borrow to fund growth.

Oliver Brown is manager of IFSL RC Brown UK Primary Opportunities (B905T77), a multicap fund that seeks to buy quality, typically dividend-paying companies when they raise

money through placings or initial public offerings (IPOs). He recalls there were no big IPOs in 2022 and the last quarter was ‘as quiet as it has probably ever been in my career’.

Yet he sees ‘more positivity on the outlook’ this year and believes there are ‘plenty of good companies out there that will be seeking fresh capital in order to expand’, with a smaller contingent wanting to protect and repair balance sheets. ‘I would expect fundraising to grow throughout the year,’ he adds.

‘I think it will be back to a more normal year, over the £20 billion mark,’ he explains.

RC Brown UK Primary Opportunities has invested in placings this year by US natural gas producer Diversified Energy (DEC), which raised £134.9 million at 105p, a 5.2% discount to the prevailing market price and 3i Infrastructure (3IN), the investment trust which raked in £100 million at 330p, a 3.4% discount.

The fund has also supported quarried materials group SigmaRoc (SRC:AIM), which raised £30 million at 54p, a 1.8% premium to the 53p market price, which it will use to acquire quarries and fund organic growth and carbon footprint reduction projects. Oliver Brown believes it is significant that SigmaRoc raised £30 million in equity and £10 million in debt for acquisitions.

‘Because the cost of debt has gone up, issuing equity is now more attractive than it was. More than ever, investors are very hot on how much debt a company has,’ says Brown. ‘We tend to buy into companies at the stage when they are raising money, so the fact that debt is reasonably more expensive and equity has become reasonably more attractive, and investors are less prepared to tolerate as much debt in businesses, means you are going to see equity raises.’

Public markets were created to allow everyone to invest in companies they believe in, but retail investors have been missing out on valuable share offers for decades as the technology wasn’t available to enable retail inclusion at scale. Increasingly however, retail investors are being offered a chance to buy shares when companies raise money through IPOs or at a discount through share placings.

This level playing field has long been desired by smaller investors, who now have a regulatory tailwind at their back following the UK Government’s Secondary Capital Raising Review (July 2022), which recommended that companies should give due consideration to including their retail shareholders in all capital raises as fully as possible.

Fundraising platform PrimaryBid enables individuals to invest in IPOs, placings and other deals, while the similar REX platform owned by broker Peel Hunt allows retail investors to participate in IPOs and fundraisings conducted as

accelerated book-builds. REX is set to become a standalone business branded ‘RetailBook’ in the second half of this year.

A share placing is when new shares are issued to institutional investors, or small groups of investors for capital. This increases the amount of shares in issue and dilutes existing shareholders by spreading a company’s profit over a larger number of shares, which decreases earnings per share. Usually new or ‘primary’ shares are only offered to institutions, which differentiates a placing to a rights issue.

The latter involves the issue of rights to existing shareholders that entitles them to buy additional shares in proportion to their existing holdings, within a fixed period and at a specified price. If a holder takes up their entitlement in full, they will own the same percentage of the company as they held previously.

Rights issues can be an effective way for companies to raise new money for acquisitions or to strengthen balance sheets and this fundraising method is often employed at times of crisis. Lloyds Banking (LLOY) used a rights issue to raise £13.5 billion in the wake of the global financial crisis

in 2009, for example, while the pandemic saw International Consolidated Airlines (IAG) and Rolls-Royce (RR.) announce multi-billion-pound rights issues to shore-up their balance sheets after the aviation sector was effectively grounded.

Rights issues aren’t always welcomed by shareholders, as their discounted price tends to pull down the market price of a stock. But many companies would argue that’s the price to pay to allow their business to grow – and that the longerterm benefits will more than compensate for the short-term pain.

An open offer gives existing shareholders the

right to buy new shares in a company at a discount to the market price. You might also hear an open offer referred to as an entitlement issue. For example, if you owned 500 shares in a company, and an open offer is announced giving you the right to buy one share for every five you own, you could buy up to 100 new shares in total. Open offers and rights issues are similar, but one key difference is that with an open offer, you can’t sell your rights in the market.

The key benefit of taking part in placings and other fundraisings is that you are typically able to buy shares at a discount to the prevailing price, and you don’t pay stamp duty. Rarely is a placing done at a premium because then the investors could just buy the shares more cheaply in the market.

On PrimaryBid, retail investors have had an average discount of just under 10% across more than 170 deals since 2020, while in the year the platform completed its most deals – 2021 with 91 fundraisings – the average discount was still attractive at 9.1%.

James Deal, head of UK and co-founder of PrimaryBid, says shareholders deserve to have the opportunity to participate in public company fundraisings, especially when they are dilutive or at a price discount.

‘Rewarding investors for their long-standing support is obvious and part of pre-emption. So too is broadening the register with new investors of the same type, i.e. retail interests. With technology, we can facilitate such inclusion for issuers with ease.’

Dilution through placings, rights issues and open offers affects the value of retail investors’ holdings depending on the number of additional shares issued in the fundraising and the number of shares held by retail investors. Increasing the number of shares in issue means both earnings

and dividends per share are stretched more thinly.

Here’s an example using a hypothetical logistics firm, ‘Cheetah FastFreight’, which has a market capitalisation of £50 million with five million shares in issue. Let’s say it has allocated £1 million to pay out in dividends or 20p a share

Aaqib Mirza, CTO of Peel Hunt who will become part of the RetailBook leadership, says that discounts through REX can vary, but the point to take away is ‘retail investors are being treated the same as institutions, so it is a level playing field’. Traditionally, institutions were the beneficiaries of these fundraising discounts, but now everyone is being treated the same.

‘We had a deal a week or two ago where the actual transaction was done at a premium to the close, so it is deal specific,’ he explains. Since launch in 2015 more than 50 deals have completed on the REX platform, generating demand of more than £450 million from retail investors.

Participating in a fundraising also means you are investing in the growth of the business unless it is a company in distress. On the flipside, if you don’t subscribe to the new shares being offered in a placing or open offer or take up your rights, your

out of earnings of £2 million or 40p per share. If it issued one million new shares the dividend per share would reduce to 16.7p and the EPS would be 33.3p. In other words, if retail investors don’t participate in the placing, their share of earnings and dividends goes down materially.

overall holding in the company will be diluted and you will suffer a decline in voting rights.

Also keep in mind that most of these placings happen after the stock market is closed for the day, so any retail investor without cash in their ISA or SIPP cannot sell an existing position in a different stock to raise money to fund their share placing application.

If you are not paying attention to messages from your investment platform provider, or studying the stock market announcements like a hawk, you might miss the placing opportunity. Investors typically have a short period – often just an hour –to apply for shares in the placing.

By James Crux Funds and Investment Trusts Editor

There was little doubt about the part of its latest results which Harbour Energy (HBR) wanted the market to focus on.

Whereas companies often look to flatter their headline profit numbers, the opposite seemed to be true when Harbour, previously known as Premier Oil, reported full-year results on 9 March. Pre-tax profit of $2.46 billion had effectively been wiped out by the energy profits levy with just $8 million left over.

Scratch below the surface and pleas of poverty do not stand up. The company generated free cash flow of $2.1 billion from which it was able to pay off more than half of its net debt and return $553 million to shareholders.

Harbour made what looked like a calculated accounting decision to book the impact of the energy profits levy all the way out to 2028 in its 2022 results.

The company, which has made it clear it will reduce headcount in the UK and could prioritise investments elsewhere, is not the only operator to decry the impact of the energy profits levy which effectively creates a headline tax rate of 75%.

Another major independent producer in the North Sea, Enquest (ENQ) is on record as saying it has deferred drilling on the Kraken field thanks to the windfall tax which it says will have an impact on its ‘capital allocation strategy and UK production growth ambitions’. AIM-quoted Serica Energy (SQZ:AIM) has made it clear it is looking elsewhere

for opportunities, even though it still believes in the ‘importance’ of UK oil and gas.

Their concerns matter as these independents will have to play a central role if the UK’s remaining reserves of oil and gas are going to be exploited, with the big oil companies having already exited large parts of the North Sea.

When the levy was first announced in May 2022 Shore Capital analyst Craig Howie observed: ‘The chancellor has actually handled it reasonably sensibly and pragmatically – particularly through implementation of a significant investment allowance.’

The problem is an 80% investment allowance was effectively reduced to 29% on everything except ‘decarbonisation expenditure’ six months later and the period over which the tax applies was extended by two-and-a-bit years.

It is the constant tinkering with the tax set-up in the UK which is arguably the biggest problem for North Sea producers and the one most likely to drive investment elsewhere. Developing an oil or natural gas field is a multi-year commitment and you need to have certainty to be able to budget and plan effectively.

More than once over the years this author has heard oil executives compare the UK’s fiscal set-up and its instability unfavourably with locations you would think would be much more fraught with political risk. Food for thought.

By Tom Sieber Deputy Editor

There tend to be many features that most good companies have in common, but there are myriad characteristics and features to analyse that will be unique to each and every business. By undertaking a detailed analysis of the 50 or 60 companies we have on our radar (a portfolio of ~40 positions and a watch list of 10-20 names), we try to ascertain whether a business is a good business and if so, whether now is the right time to be invested or not.

In 1984, on a late-night flight from Paris to London, a chance encounter between Jane Birkin, the actress, singer and model, and Jean-Louis Dumas, the CEO of Hermes, resulted in a moment of inspiration that created the Birkin Bag. Nearly 40 years later, The Birkin is well established as Hermes’ most iconic and desirable handbag. Demand for these bags significantly exceeds their carefully managed supply and even secondhand prices can be stratospheric. The Birkin is a wonderful example of the power of human desire for beautifully made, scarce items and it is this longstanding desire that drives powerful, resilient economics for a company like Hermes.

The history and heritage of the brand is a crucial driver of desirability for any branded goods company. The history of Hermes goes back a long time before the iconic Birkin was dreamt up. In 1837, Thierry Hermes opened his first workshop in Paris, specialising in harnesses. Made-to-measure saddles followed, with the establishment of a broader leather goods offering during the interwar period. Today, Hermes has grown into a global company employing nearly 20,000 people and generating revenues of over €11bn.1 The power of the business today stems from the history and heritage of the brand.

You can’t create heritage, you can’t invent a history, but brand desirability is inextricably linked to the past. This gives companies like

• Hermes carefully manages the volume of products it manufactures, tightly controls the distribution chain, and ensures that demand growth exceeds supply growth year-after-year. This helps drive brand desirability and pricing power.

• High gross margins enable Hermes to invest heavily behind the brand whilst also generating high levels of profitability. Meanwhile, long-term wealth creation and the growth of aspirational, middle-class consumers in emerging markets continues to drive growth.

• We take a long-term view when judging the merits of a particular company and this aligns with family owners who tend to care about the long-term wealth creation that comes from their stake in the company, rather than being concerned with short term profitability.

Hermes a huge competitive advantage and creates a powerful moat around their business. Hermes is a great example of a company with a carefully protected brand heritage – this drives attractive and durable economics for shareholders. We have owned Hermes since 2014 and continue to see attraction in the long-term investment case, the key pillars of which are laid out below.

Desirability, brand heritage, and limited supply drive attractive gross margin dynamics… Heritage and history are extremely important elements of brand desirability. However, brands can lose their desirability over time. Hermes has consistently invested in its brand and has maintained exceptional manufacturing quality, with every Hermes bag handmade, and hand stitched in an artisanal workshop.

Another risk to a brand comes from the supply side. A desirable, aspirational brand loses its appeal the minute that supply exceeds demand –humans desire things that they can’t have! Hermes carefully manages the volume of products which they manufacture, tightly controls the distribution chain, and ensures that demand growth exceeds supply growth year-after-year. Waiting lists are the norm for their most desirable products. This has helped drive brand desirability and, with it, Hermes’ ability to charge prices significantly ahead of the cost of the raw materials used to make a particular product.

These factors – amongst many others – contribute to high (~70%) gross margins for Hermes.1 These exceptional gross margins are a key element of the overall strong economics delivered by the company.

High gross margins enable Hermes to invest heavily behind the brand whilst also generating high levels of

High gross margins mean that for every unit of revenue that Hermes receives, they simply generate more profit and cash than a lower gross margin company would. This is extremely important and acts as a significant competitive advantage. It provides Hermes with the firepower they need to consistently invest in the brand and to grow the business. They spend less than you might imagine on Advertising & Promotion (circa. 5% of sales versus some peers at 10% of sales), but that is the beauty of operating such a well-known brand with such a long history behind it.1 The strong presence of flagship stores helps build their brand presence as well as acting as a core sales channel; most of their operating costs are focused

on investments behind their retail stores.

With 70% gross margins, Hermes is able to invest around 30% of sales in operating costs (advertising, costs associated with the stores etc) whilst still generating extremely healthy operating margins of around 40%.1

Low capital intensity and working capital needs combine with high margins to drive an attractive return on invested capital…

Though Hermes is a vertically integrated business, it is operating in an industry where capital intensity is not high. This factor combines powerfully with the high margin structure to ensure that Hermes generates a very attractive return on invested capital. In 2022, Hermes generated €4.7bn of operating income, and with a 29% tax rate, this resulted in net operating profit after tax of around €3.3bn.1 From my calculation, its average invested capital for 2022 was around €5.1bn, meaning Hermes is currently generating a return on invested capital of around 65%.2 This is exceptional when compared to the wider market. There are not many companies in Europe that can match this kind of economic performance.

Long term wealth creation and the growth of aspirational, middle-class consumers in emerging markets continues to drive significant growth… For any potential investment, growth in revenues and earnings are not necessarily attractive or desirable. It all depends on how much capital is required to fund that growth and what return on capital the company is able to generate. As I have shown above, Hermes is able to generate very attractive returns on capital. Therefore, this is a company that we want to grow – we love it when they are able to deploy capital for further growth. Growth is a significant part of the attraction for us with a business like this.

In 2012, Hermes generated €3,484m in sales, by 2022, revenues have expanded to €11,602m.1 Clearly, part of this strong growth (12.8% compound annual growth rate) is related to the strong desirability that Hermes has and their success in expanding to new customer groups in new regions.3 However, an important reason for why we like Hermes simply relates to the industry in which they operate. The luxury goods industry has experienced significant growth over the past 20 years, driven by powerful structural themes, whilst Hermes has managed to consistently outgrow the sector; from 1999-2019, the sector has grown at a 7-8% CAGR, whilst Hermes has grown at an 11% CAGR.4

Global wealth creation is the most powerful sector driver. Over the past 20 years, global wealth has grown by 7% per annum and this is set to continue. The wealthy are getting wealthier, and the growth of the middle classes in China, India and other regions is helping to support global wealth creation. This is a major growth driver for the sector.5

A final point worth discussing is the fact that Hermes is a family-controlled company. Different investors view family ownership in different ways. As a general rule, we like to invest alongside families that have been longstanding owners of a business. We take a long-term view when judging the merits of a particular company and this aligns with family owners who tend to care

about the long-term wealth creation that comes from their stake in the company, rather than being concerned with short term profitability. Thus, family control allows the management team to think and act in a long-term way without being worried about whether they might be judged on shorter term metrics. This fosters the perfect environment for maintaining the power of a heritage brand; the long-term health of the brand should trump concerns over short-term profitability every time. With Hermes, we truly believe this to be the case and the family ownership plays a significant role in this.

Recently, the family behind Hermes have committed to maintaining their controlling stake in the until 2041 at the earliest. We see this as very good news.6

1Source: https://assets-finance.hermes.com/s3fs-public/node/pdf_file/2023-02/1676618361/slides-fy2022-va-vdef.pdf

2Source: Henderson EuroTrust, 2023

3Source: https://finance.hermes.com/en/publications#

4Source: Citi Research – The Power of a 183-year-old icon, 26 June 2020

5Source: Credit Suisse – EMEA Luxury Goods: Entering a new dawn – 50 key questions for luxury investors, 8 November 2022

6Source: https://www.voguebusiness.com/companies/hermes-family-signals-plan-to-retain-majoritystake-until-at-least-2041#:~:text=The%20family%20members%20own%2054,through%20the%20 holding%20company%20H51

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Unless otherwise stated all data is sourced from Janus Henderson Investors.

We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Janus Henderson, Knowledge Shared, Knowledge Labs are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

GC-0123-121490 01-31-24 TL

Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. This is a marketing communication. Please refer to the AIFMD Disclosure document and Annual Report of the AIF before making any final investment decisions.

• If a Company's portfolio is concentrated towards a particular country or geographical region, the investment carries greater risk than a portfolio diversified across more countries.

• Some of the investments in this portfolio are in smaller companies shares. They may be more difficult to buy and sell and their share price may fluctuate more than that of larger companies.

• This Company is suitable to be used as one component in several in a diversified investment portfolio. Investors should consider carefully the proportion of their portfolio invested into this Company.

• Active management techniques that have worked well in normal market conditions could prove ineffective or detrimental at other times.

• The Company could lose money if a counterparty with which it trades becomes unwilling or unable to meet its obligations to the Company.

• Shares can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

• The return on your investment is directly related to the prevailing market price of the Company's shares, which will trade at a varying discount (or premium) relative to the value of the underlying assets of the Company. As a result losses (or gains) may be higher or lower than those of the Company's assets.

• The Company may use gearing as part of its investment strategy. If the Company utilises its ability to gear, the profits and losses incured by the Company can be greater than those of a Company that does not use gearing.

References made to individual securities should not constitute or form part of any offer or solicitation to issue, sell, subscribe, or purchase the security. Janus Henderson Investors, one of its affiliated advisors, or its employees, may have a position mentioned in the securities mentioned in the report.

Not for onward distribution. Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. This is a marketing communication. Please refer to the AIFMD Disclosure document and Annual Report of the AIF before making any final investment decisions. Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued in the UK by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

The story of Tesla (TSLA:NASDAQ) continues to astonish investors, both fans and sceptics. In the early part of 2023, the share price had all but doubled (from the start of the year to 15 Feb), followed by sharp falls from that $214.24 peak a month ago. As it stands, the stock is about 57% up year-to date at $169.98.

It’s a far cry from its pariah status of 2022 when shares in the electric cars-to-energy lost nearly 70% of their value.

The question is, what next?

A key part of Tesla’s share price advance this year has been its price cuts. In January, the company lowered the prices of two of its most popular vehicles, the Model Y and Model 3, across US and European markets by up to 20%. The company cut prices again at the start of March.

‘Our focus on continuous product improvement through original engineering and manufacturing processes have further optimised our ability to make the best product for an industry-leading cost,’ is what Tesla said in a statement at the time.

‘As we exit what has been a turbulent year of supply chain disruptions, we have observed a normalisation of some of the cost inflation, giving us the confidence to pass these through to our customers.’

As is so often the case with Tesla, investors have found themselves split over EV (electric vehicle) prices.

‘How do bulls like Dan Ives or Gary Black justify improving margins when the company is cutting selling prices and inventory is up?’ asked Markets.com analyst Neil Wilson rhetorically. Dan Ives is an analyst at US broker Wedbush. Gary Black is a Future Fund managing partner and co-founder. Both are long-run champions of Tesla shares.