Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe key considerations to factor in before selling a share

Following the collapse of global stock markets this year, many observers may think the ‘when to sell’ boat has been missed. Not so. History shows that investors consistently get this wrong, buying high and selling low, despite the opposite being the objective.

Many investors sit on poorly performing stocks in the hope that they will eventually recover. Others get timing hopelessly backward, selling perfectly good companies after a sharp stock market fall, fearing running up even larger losses when recovery is just over the horizon.

BABY OUT WITH THE BATHWATER

Here’s an example. In October 2016, shares in ID management and fraud prevention software company GB Group (GBG:AIM) lost a third of its value after reporting mildly disappointing growth and a slow start on an online identity verification programme for the UK government.

In response Shares said at the time that this was a heavy-handed market response to a short-term hiccough, but no doubt plenty of ordinary investors shared the market’s cold feet and sold the stock.

Big mistake. By the summer of 2017 the share price had recovered all of its previous losses and more at close on 400p. The stock was close to 600p another 15 months on, and had surged beyond 900p late last year, before the latest market shake-out took hold.

GB is not unique but serves as a lesson in keeping your emotions in check, reassessing your investment thesis, and acting accordingly when a bad spell strikes a company you have previously backed. Just because a share price has fallen sharply doesn’t necessarily mean you should ditch a company.

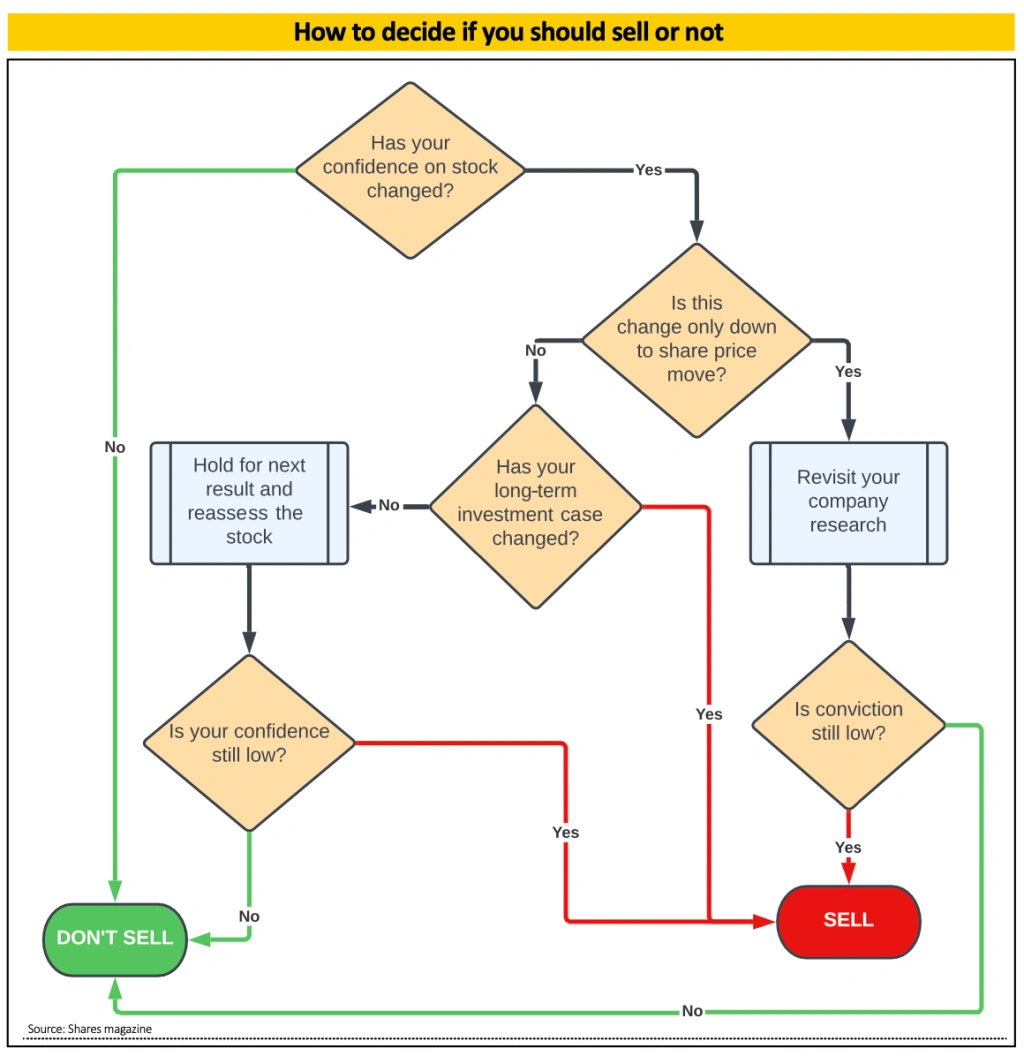

What investors should do is ask yourself some tough questions, such as has the fundamental investment thesis changed, are you simply reacting to a share price fall, and is it worth monitoring the stock a little longer to see if your continued confidence is justified? All easy to say, harder to do, but to make this process easier for readers, we have provided a simple decision flow chart (see graphic below).

MARKETS GO UP AND DOWN, GET USED TO IT

Put simply, market falls are a harsh reality of buying shares, and if the possibility that you may not get back all that you have invested scares you, equity markets are probably not for you. But for millions of investors, the potential to grow their real-terms wealth over many years makes the risks worthwhile.

That the MSCI World Index has lost 21.4% this year shows the widespread nature of the current stock markets shake out, even if some popular indices have done better.

The FTSE 100, for example, is down just 5% or so. But it does mean that many ordinary investors who hold individual shares now know what it feels like to buy a share that drops sharply in price if they didn’t before.

Today’s challenges are not the same as previous downturns, and stocks that bounced back quickly in the past might not this time, and vice versa.

Storied investor Warren Buffett says his ideal holding period for an investment is ‘forever’. Yet few investors are as skilled and confident as Buffett, whose ‘forever’ strategy relies on only buying high-quality businesses capable of withstanding periodic trading challenges and have the capacity to adapt to a changing business environment.

Think about how Greggs (GRG), for example, has emerged from being a high street baker to today’s hot and cold snacks on-the-go operator.

A decade ago, many investors may have wondered if Greggs might go the way of Percy Ingles as competition intensified and consumer behaviour changed. Go back a decade and Greggs shares were a quarter of today’s £18.57, and that’s having halved this year. Dividends over the decade bolster value creation further still.

Many people are looking for easy answers to difficult questions, and there are plenty willing to try to provide them. For example, equities experts at Barclays (BARC) say keeping emotions out of your investment decisions helps.

Barclays also advises fixing a price at which you automatically sell a share and identifying overvalued stocks and avoiding them in the first place. Taking a cold and clinical approach to investment decisions is, we believe, sound advice as is, in principle, not buying overvalued stocks, even if this is highly subjective.

For example, in November 2021 investors thought £340 was a fair price to pay for Microsoft (MSFT:NASDAQ) shares. Today, the market thinks $250 is closer to the right figure, despite its long-run growth opportunity being barely dented by current events. What has changed is the attitude of investors who are reacting to what may well be relatively short-term factors, such as spiralling inflation.

Forcing yourself to sell winners at a fixed price is more controversial still, we would argue. ‘It’s never wrong to bank a profit’, some say, yet that ensures that followers of this investment maxim are prepared to miss out on the compounded benefits of growth earned over decades.

COMPOUNDED GROWTH RETURNS OVER YEARS

Take health, safety and environmental electronics firm Halma (HLMA). It has earned a premium rating thanks to years of consistent, high-quality growth, yet with a price to earnings multiple typically in the 30s, many fund managers and ordinary investors have refused to buy the shares.

In June 2022 it reported its 19th consecutive year of record profit, and while 2022 has been a tough year for the stock, like so many others (down 34% year-to-date), the value and wealth creation for long-term holders has been astonishing, with a 20-year total return of more than 3,200% at its recent peak, and still above 2,000% at the current lower price, according to FE Analytics.

Shares believes that investors benefit most, not by being told by experts or recent share price performance, that they should sell a share. But by being armed with a framework within which they can draw their own conclusions.

There’s a reason why deciding when to sell a stock is widely seen as one of the most difficult decisions investors face. We hope that by providing readers with a simple framework, they will find future decisions, if not easy, less difficult to make.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Feature

Great Ideas

News

- Profit warnings galore as companies struggle with higher costs and lower demand

- Find out why consumer health group Haleon’s debut fell flat

- Investors are rushing to exit funds as small cap specialists really suffer

- Wealth preserver Ruffer warns bear market is ‘only mid grizzle’

- Fevertree’s earnings forecasts slashed by nearly 50% after problems get worse