Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

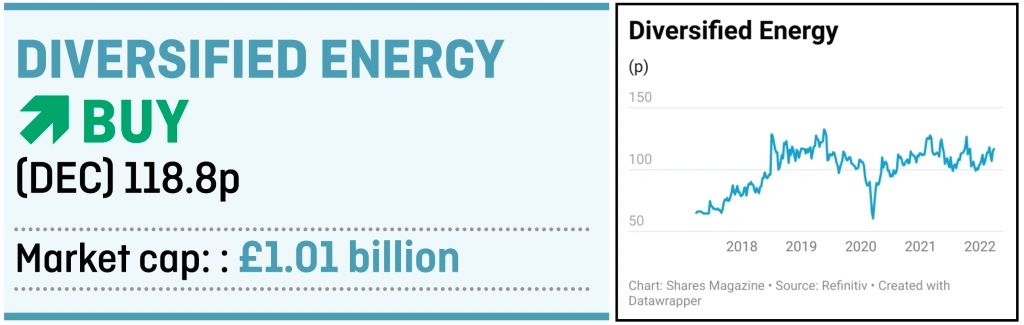

magazineBeat inflation with Diversified Energy’s big dividends

A Western world looking to wean itself off Russian energy is increasingly looking to the US and that is great news for FTSE 250 US natural gas producer Diversified Energy (DEC) as it should provide a strong driver for domestic energy prices.

Shares in the company trade at a mere six times 2022 consensus forecast earnings and offer an inflation-busting dividend yield of 11.2%.

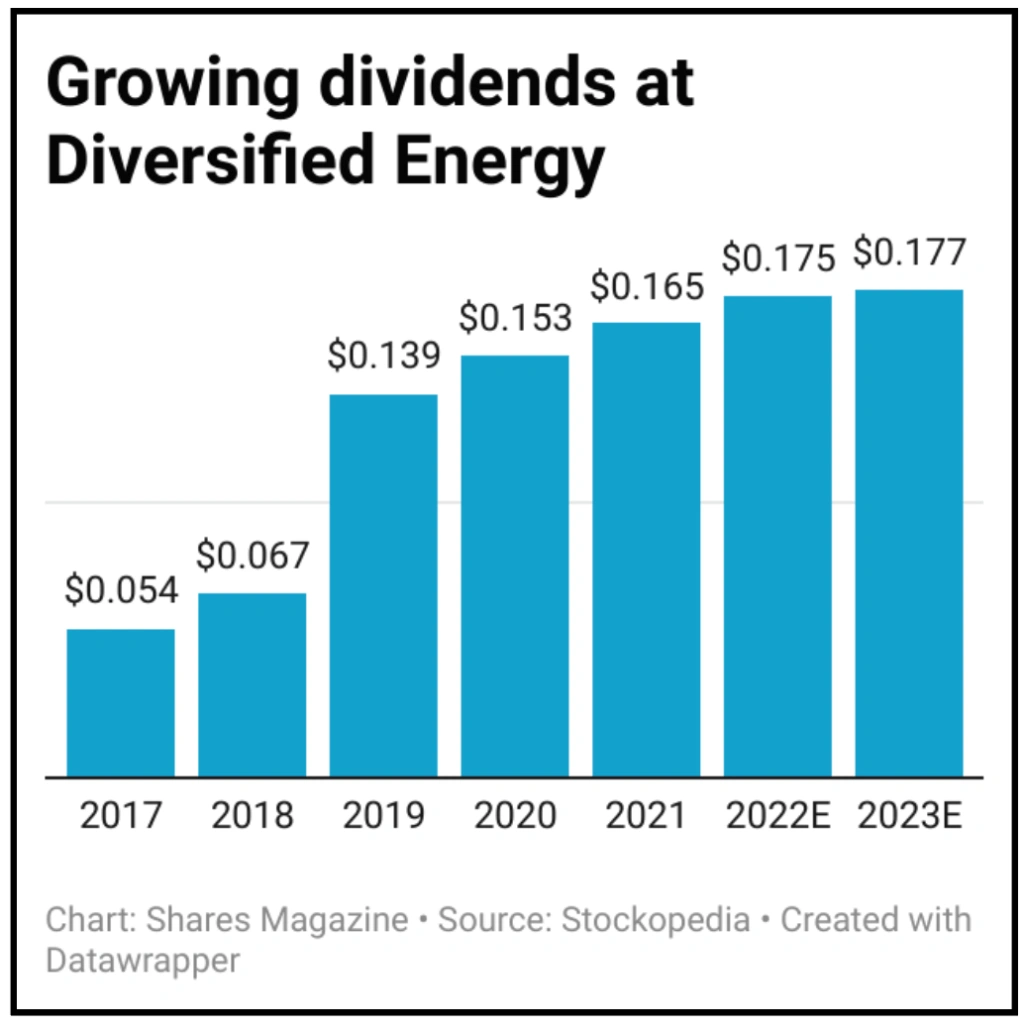

Diversified Energy has grown the dividend, which investors should be aware is declared and paid in dollars, from a maiden annual payment of 5.44 cents in 2017 to 16.5 cents in 2021.

Its strategy is built on acquiring conventional natural gas assets, spanning from the Appalachian region to Louisiana, Texas, Oklahoma and Arkansas.

Diversified Energy aims to buy fields with long lives where production is declining slowly. This helps to generate a predictable stream of cash flow which can underpin the dividend.

In 2021 the company produced a record 119,000 barrels of oil equivalent per day and kept operating costs low at $6.73 per barrel of oil equivalent.

The company has been adept at using debt and other avenues for financing to fund its expansion and thereby avoid issuing new shares and diluting shareholders. However, this brings some complexity to the story which may explain the discounted equity valuation.

For example, the company uses securitisation – packaging up its assets and selling them as securities with a coupon payment. The company recently completed its latest such transaction, raising $365 million, and CEO Rusty Hutson Jr explained to Shares that it represents a ‘low cost of capital for us in a rising interest rate environment’ at a coupon of less than 5%.

Net debt stood at a little more than $1 billion as at the end of 2021, or around 2.1 times earnings. This is in line with the firm’s targeted range and according to US broker Tennyson it has liquidity of up to $400 million to put towards future acquisitions and is looking at options to boost this to as much as $700 million.

Hutson Jr says he would be extremely disappointed not to match last year’s deal flow of four acquisitions at a net cost of around $700 million.

The company secured additional firepower for deals through a November 2020 agreement struck with specialist asset management firm Oaktree Capital which committed to a $1 billion outlay to be matched by Diversified Energy and Hutson Jr says the ‘model is sustainable for a long period of time’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Make the most of your ISA allowance: three stocks to buy now

- Recession fears: How to protect and grow your wealth if the economy weakens

- How bond fund managers analyse investments and assess risk

- How important are commodities in the Brazilian economy and market?

- Emerging markets: Views from the experts

Great Ideas

- ConvaTec has turned a corner and offers growth and re-rating potential

- AG Barr fizzes to profit ahead of pre-Covid levels

- SDI’s £7.7 million deal to immediately boost earnings

- Homeserve shares surge higher on bid approach

- Value specialist Temple Bar is well placed for inflation and rising rates

- Beat inflation with Diversified Energy’s big dividends

- Strong demand drives gains in logistics, residential and development

- Our faith in the managers is undiminished despite a slow first half

Investment Trusts

News

- What a harsh EU clampdown means for Apple, Google and other big tech firms

- Why Pendragon might be the next auto retail takeover target

- US Treasury yields surge as Fed toughens stance on mounting inflation

- Mark Barnett makes a comeback with new Tellworth equity income fund

- Terry Smith uses Fundsmith investor meeting to criticise Unilever top brass